Volatility Cluster Coming In May?

Volatility Cluster Coming In May?

SPX Testing Important Levels...Again

Hello and welcome to another issue of 🕵 The Seeker 🕵

“Inflation is when you pay fifteen dollars for the ten-dollar haircut you used to get for five dollars when you had hair.” - Sam Ewing

1) Big moves drawing attention from the last three trading days.

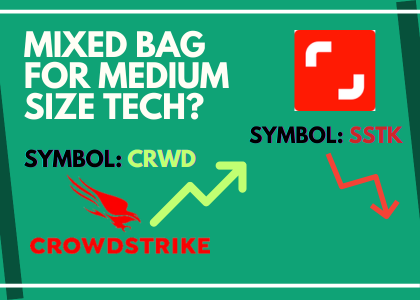

Crowdstrike, which was battered down over the last two weeks, has made a strong charge up CRWD 0.00%↑ on Friday. It broke through its 8-day resistance. Crowdstrike is scheduled to report earnings on May 31st.

Similarly, the selling in Cloudfare has been harsh. With longer-term moving averages that are beginning to flatten out, combined with weekly MACD that is pushing into positive territory NET 0.00%↑ , there is some possibility for better risk/reward on the long side than has existed. NET recently beat Q1 estimates.

Similar to above, in the aftermath of the market selloff related to Silicon Valley Bank, GameStop shocked the market gapping higher on positive earnings news. Since then, GME 0.00%↑ has closed that gap, but now shows signs of life again and is peaking above its 8-day moving average.

Conversely, remaining weak was Shutterstock. This company had been deemed an AI leader at the end of January. Since then, SSTK 0.00%↑ has been popular for sellers, without hearing so much as a whimper from bulls, not even during Friday's stock rally.

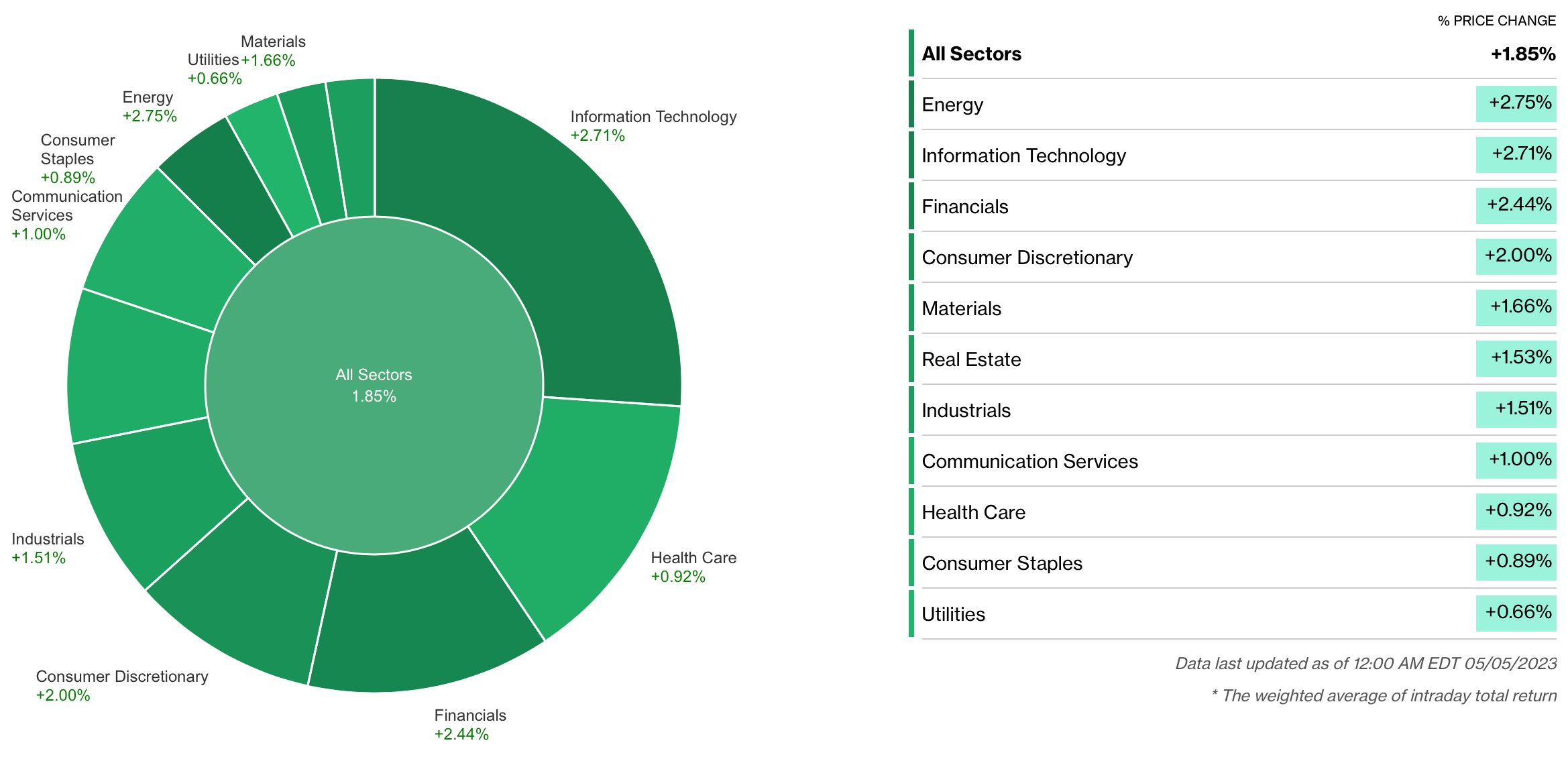

2) Sector Performance

Friday was a positive day for markets with all sectors in the green.

For the week, the top sectors were Technology, Utilities, and Staples. Of note on an industry level, Brewers from the Staples category were making a 52-week high relative to S&P500, and Gold Miners were continuing their strength from the October lows.

Here is the weekly chart of Ambev SA, a Brazilian brewer, which looks very constructive. Quietly, Brazil has been staging a comeback following political unrest and industry tailwinds. ABEV 0.00%↑ could be poised to join its peers in outperforming.

…and not to be forgotten, semiconductors on the week still did not show their hand. We had reports this week from NXPI 0.00%↑ as well as AMD 0.00%↑, and QCOM 0.00%↑ , giving equal and opposite reactions. In total, as measured by the VanEck Semiconductor ETF SMH 0.00%↑ , semis were up +0.61% on the week.

Following the latest earnings, analysts maintain a very favorable outlook (Buy >3) with positive revisions. (Note the diverging 2nd/3rd derivative with real-world fundamentals).

3) Earnings reports from this last week:

Weekly major price reactions from significant companies of interest.

4) The week ahead

From Barrons:

The Calendar

It will be another busy week of earnings, with Devon Energy, KKR, McKesson, PayPal, and Tyson Foods reporting on Monday.

Tuesday brings results from Airbnb, Air Products & Chemicals, Apollo Global Management, Duke Energy, Electronic Arts, Occidental Petroleum, and TransDigm Group.

Brookfield Asset Management, Roblox, Toyota Motor, and Trade Desk are on the schedule for Wednesday.

And Thursday, we'll hear from Honda Motor, JD.com, PerkinElmer, and Tapestry.

The economic highlight of the week comes on Wednesday, when the Bureau of Labor Statistics releases the consumer price index for April. Economists forecast a 5% year-over-year increase, matching the March data. The core CPI, which excludes volatile food and energy prices, is expected to rise 5.4%, two-tenths of a percentage point less than previously. Both indexes are well below their peaks from last year but also much higher than the Federal Reserve’s 2% target.

On Thursday, the Bank of England is scheduled to announce its next monetary-policy decision. The central bank is widely expected to raise its bank rate by a quarter of a percentage point, to 4.5%. The United Kingdom’s CPI rose 10.1% in March from the year prior, making it the only Western European country with a double-digit rate of inflation.

Also Thursday, the Department of Labor reports initial jobless claims for the week ending on May 6. Claims averaged 239,250 in April, returning to historical averages after a prolonged period of being below trend, signaling a loosening of a very tight labor market.

And the BLS releases the producer price index for April. The consensus call is for the PPI to increase 2.4% and the core PPI to rise 3.3%. This compares with gains of 2.7% and 3.4%, respectively, in March. The PPI and core PPI are at their lowest levels in about two years.

Finally on Friday, the University of Michigan releases its consumer sentiment index for May. Economists forecast a dour 62.6 reading, about one point lower than in April. Consumers’ year-ahead inflation expectations surprisingly jumped by a percentage point in April to 4.6%.

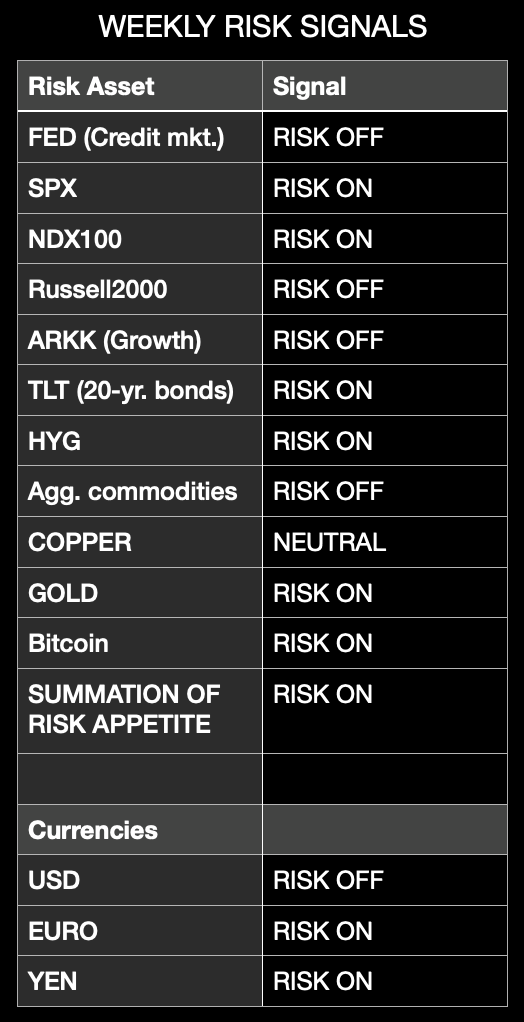

5) Macro conditions

Weekly risk signals are based on intermediate and long-term market trends, as well as the flow of money into or away from asset classes. Not included are potential fundamental or gamma implied volatility tail risks.

Note: top traders themselves have a hit rate approaching the 50% lower bound. Controlling risk on losing positions and letting winners prosper is for many the difference in creating a successful track record over time.

As shown, US markets $SPX, $QQQ 0.00%↑currently generally favor risk assets. A very weak USD is providing a tailwind, particularly for high-yield, large-cap Nasdaq issues, and even Bitcoin. Of specific concern is the Fed's heavy-handed impact on cyclical investments.

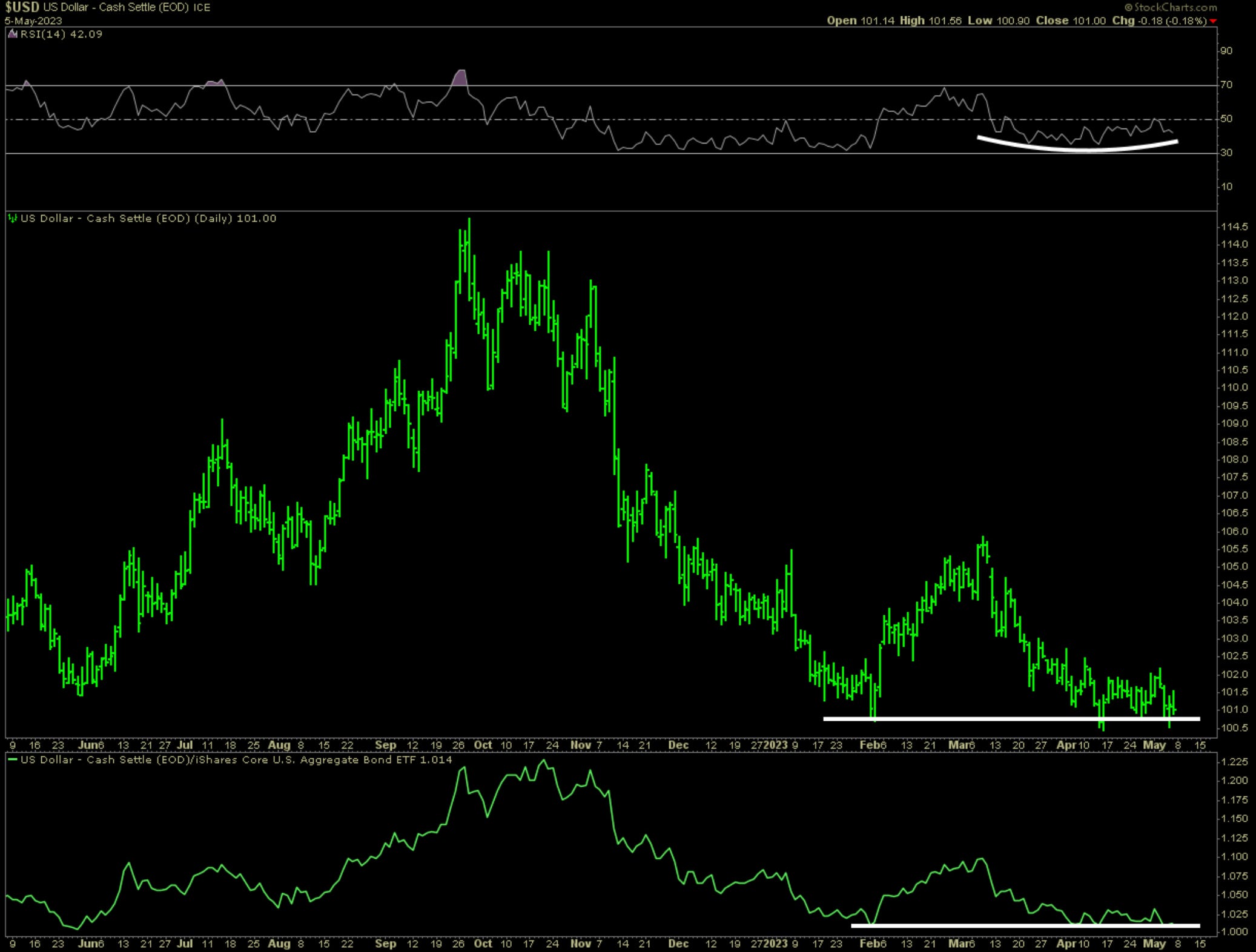

Let's zoom in on the daily chart of the USD:

Unfortunately for USD bulls, no bullish reversal from a double bottom appears to be forming, as price teeters at it’s lowest levels for the year, including relative to a basket of bonds.

However, this must be watched more closely now due to Friday’s strong jobs report. A common trend witnessed again & again are delayed reactions to these events, and this time could be no different. Off-sides traders may have been able to cause a smoke screen drawing attention of stocks, while the run for cover might take place here.

6) Opportunities Internationally

This section The Seeker will specifically strive to build-out in the period ahead and research some interesting gems from all regions. At this immediate instance a couple of names and themes deserve attention.

Emerging markets and $EEM have been relatively strong. Returning to Brazil, we are potentially witnessing the breakout from a significant consolidating range for Stone Co. $STNE 0.00%↑

In other sectors, domestically we’ve seen strong renewable utilities such as BEP 0.00%↑ Brookfield Renewable Corp. Relating this strength to other markets, we could be seeing the makings of a significant turn-around in Scatec solar, where Equinor as of March 16th increased their ownership interest to 16%, primarily caused by rumors of favorable changes at the top of management.

…and a bonus chart. Should one be additionally more inclined for a contrarian take. A reduction in recession fears and rebound in inflation could add significant rally fuel to oil producers, especially those with even weaker international currencies and earnings streams in dollar.

😎 Cheers! 😎

Disclaimer: Please note that the information provided in this article is for general informational purposes only and does not constitute financial, legal, or professional advice. The information provided should not be relied upon as a substitute for financial, legal, or professional advice. Before making any decision, it is important to consider all relevant information and consult with a professional who can provide personalized advice based on your specific circumstances. The author and publisher of this article cannot be held liable for any actions taken based on the information provided. This is not a recommendation to buy or sell any specific securities or financial instruments.