The Revenge of Breadth

Hello and welcome to another issue of 🕵 The Seeker 🕵

"Don't confuse brains with a bull market" - Humphrey B. Neill.

1) Big moves and/or interesting developments from the last three trading days.

With the summer more and more upon us in the northern hemisphere, it’s only fitting that Live Nation is starting to flex it’s muscles. In the face of controversies, not unsimilar to other large moat companies, LYV 0.00%↑ produced a positive earnings surprise that impressed an analyst corps already infatuated with the company’s potential.

Here is the current chart examining Live Nation’s possible untangling from a heavy VWAP (base).

Another stock making the case for an interesting reversal is Chargepoint Holdings. After breaking through $10 in December, the stock looked well on it’s way to closing the price gap to $5. Though it’s still trades below it’s long-term moving average (not shown), it’s recently rejected a break below and held above it’s 2022 all-time low. What’s makes the price even more compelling, is that CHPT 0.00%↑ has been trading into the upper band of it’s negative trajectory for a significant length of time trying to break out, so it’s recent reversal wasn’t completely unlikely. Now with the price coming back down to test the 50-day m.a., there could be interesting risk-reward looking for positive mean reversion.

From the small-cap international space, one name with awe inspiring action is CI&T inc. This Brazilian software house recently witnessed what appears to be a total capitulation by sellers potentially forced exiting at all costs. What looks to have unfolded thereafter is a major ownership shift with large flows and heavy trading volumes the last several weeks. We think CINT 0.00%↑

could likely trade in sympathy with ARKK, so we’ll be watching this space as long risk-on sentiment remains in control.

Looking at SSTK 0.00%↑ price optimism now seems like it could be finding a more reasonable level. Though Shutterstock continues to issue significant stock reimbursement to employees, it’s returning value in the form of dividends, growing the business thru acquisitions, and in it’s most recent quarter saw good year-over-year fcf growth. Add to this that there has recently been significant pain for traders holding this stock. This reviewer thinks it could be ripe here for a positive correction.

…but let’s be honest with ourselves, often times it’s just easier to relate to blue chips. I’d be dishonest if told you I knew everything was ok at ZScaler the first week of May and was loading up on cheap call options. No, the truth it fact was it falling further off the radar, steeped in a parabolical decent. So at this moment reviewing Adobe, I imagine there are many others out there saying the same thing and breathing a sigh of relief peering over this chart. Even though ADBE 0.00%↑ itself sold off hard on merger news in 2022, it’s back returning to it’s August 2022 high in a much more convincing way (i.e. volume), and at this point it’s made a 62% retracement from it’s breakout zone prior to it’s ath.

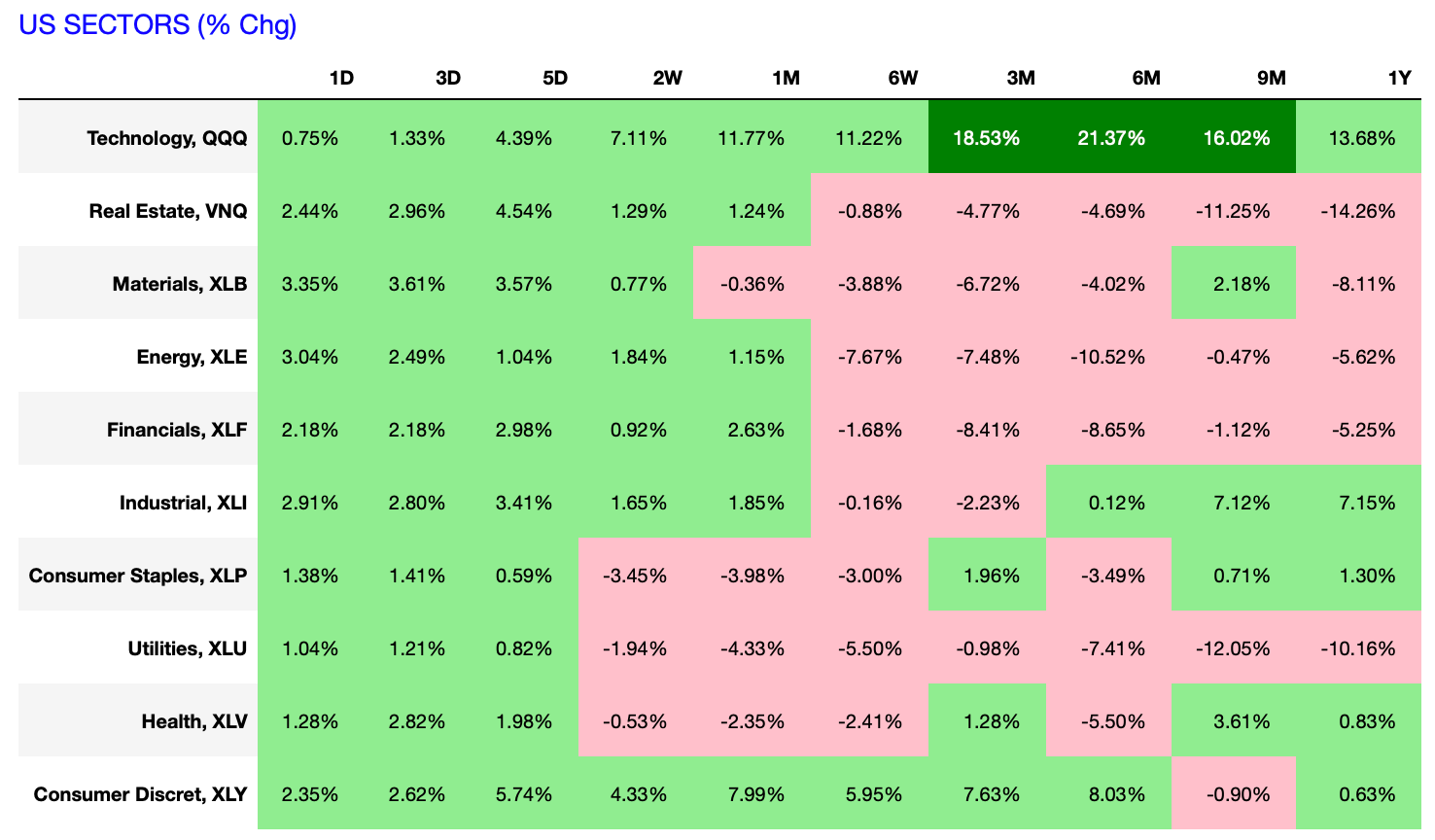

2) Sector Performance

This week the turn of the month occurred, and especially going into the weekend, new investment capital was being deployed by fund managers into stocks. Friday was green across all sectors, with especially beaten down cyclical sectors outperforming.

Looking at where things stand, if tides are turning for the common stock, there is still a lot of catch-up potential for cyclicals / equal-weight indices. Defensives could however be poised to maintain weakness.

Digging further down into industry results, optimism is apparent in the media sector. One interesting name is Zoominfo Technologies ZI 0.00%↑. It looks cheap (maybe a bad thing!) and is pulling out of it’s decline with pent up divergent energy.

Another chart jumping out on this author’s screen is General Motor’s. Auto’s have been improving lately, and frankly like airlines, will likely always be captivating to investors’ dollars. Last week we featured Lithia Motors and hinted that now might be the time to look harder at this space. Likewise in the Discord, the QF-screeners have recently signaled Tesla for a move. Like the salmon of Capistrano, it now looks like time for GM 0.00%↑ to make a pass through it’s trading range, especially IF breadth is to improve through the summer.

Returning home to the semiconductor space, it was a short choppy week. Monday the SMH 0.00%↑ gapped higher in anticipation of FOMO from late buyers. It then sold off further, but however finding support at the top of it’s recent major gap higher, and was relatively unchanged going into the weekend.

One name that’s been uncommonly quite, but still going about it’s business is On Semiconductor. ON 0.00%↑ has a significant presence in the making of chips to the auto industry.

3) Earnings reports from this last week:

Weekly major price reactions from significant companies of interest.

4) The week ahead

From Barrons:

The Calendar

Next week will be relatively quiet before major inflation data and a Federal Reserve decision the following week. There are still several earnings and economic data releases to look forward to.

Earnings will include results from Gitlab on Monday, Ciena and J.M. Smucker on Tuesday, and Brown-Forman, Campbell Soup, and GameStop on Wednesday. DocuSignand Vail Resorts report on Thursday, then NIO goes on Friday.

The economic data highlights of the week will be the Census Bureau’sdurable goods report for April on Monday and the Institute for Supply Management’s services purchasing managers’ index for May on Tuesday.

The Reserve Bank of Australia will announce a monetary-policy decision on Tuesday. Futures markets are pricing in roughly one-in-three odds of a 12th-straight interest-rate increase.

--Nicholas Jasinski

5) Macro conditions

Weekly risk signals are based on intermediate and long-term market trends, as well as the flow of money into or away from asset classes. Not included are potential fundamental or gamma implied volatility tail risks.

Note: top traders themselves have a hit rate approaching the 50% lower bound. Controlling risk on losing positions and letting winners prosper is for many the difference in creating a successful track record over time.

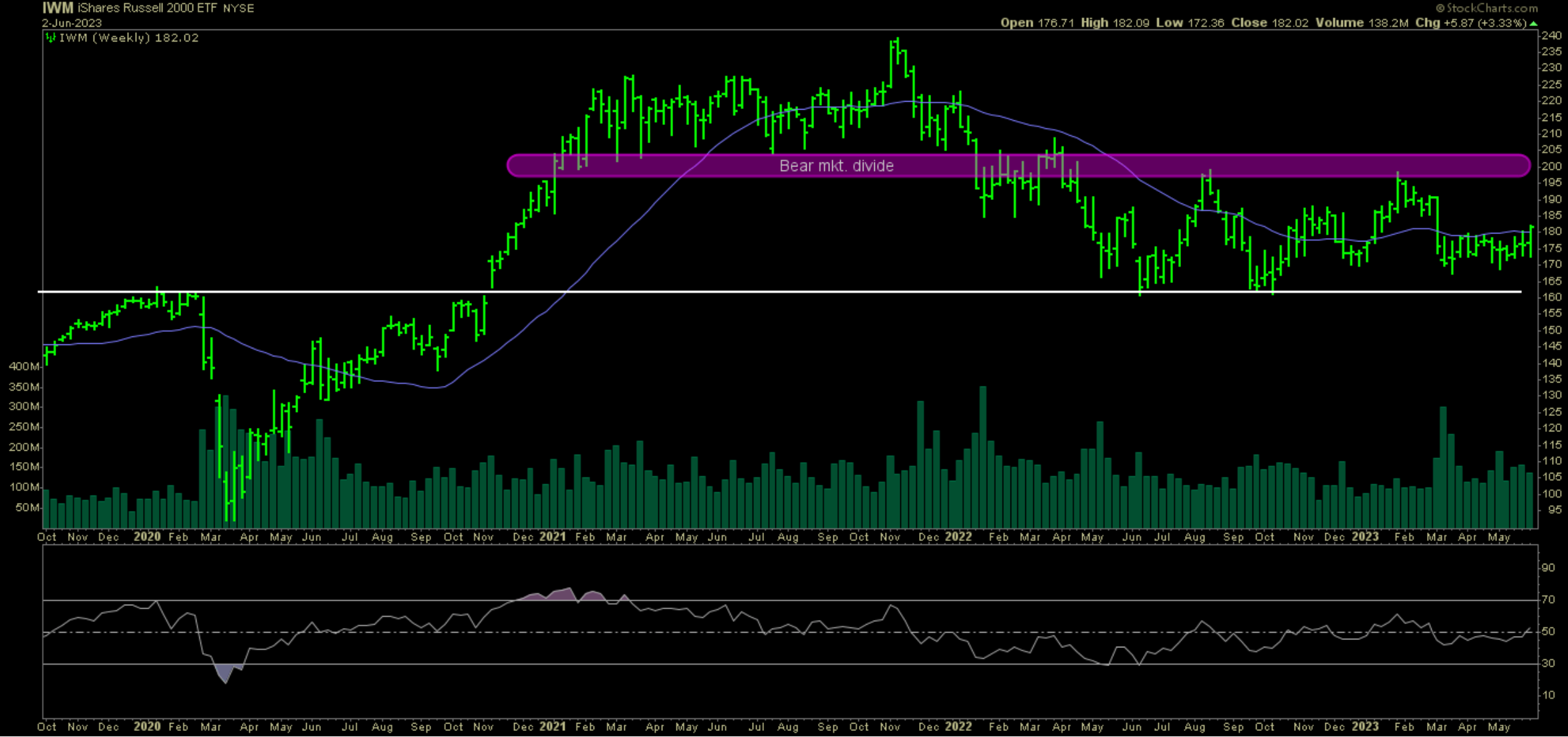

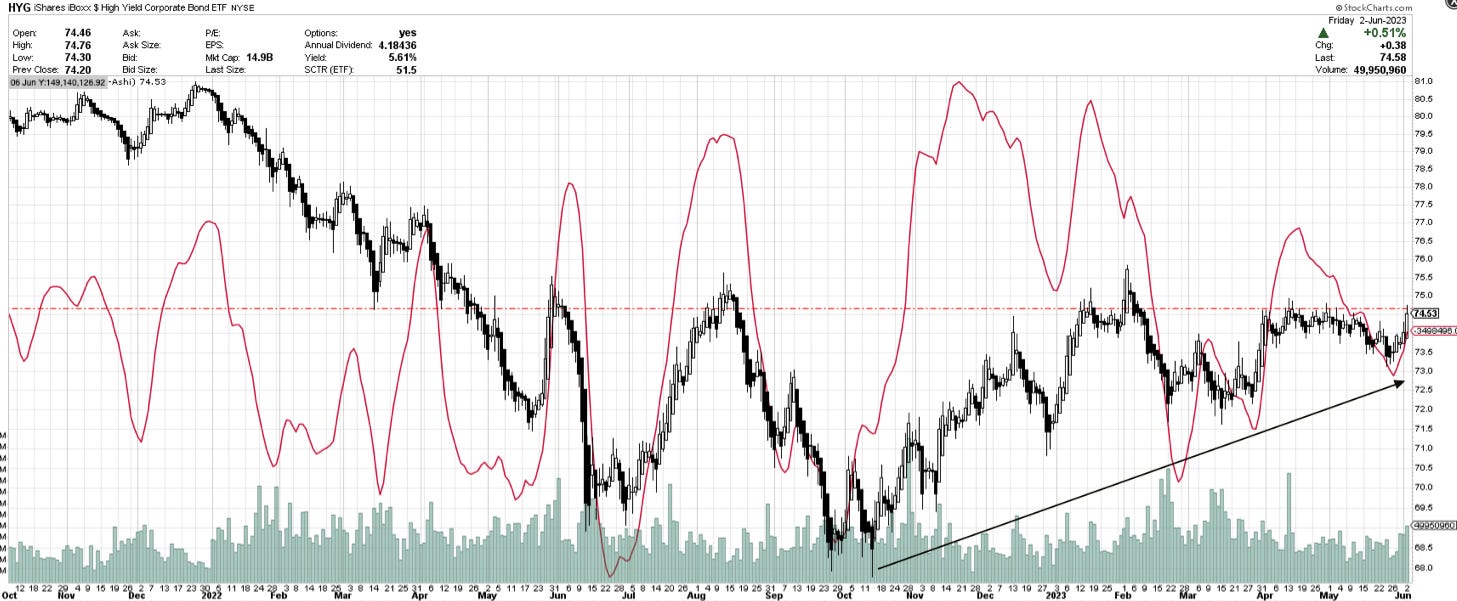

Another eventful week was laid to rest having a significant impact on macro conditions. We saw the debt ceiling resolved and a rotation away from the insurance of event pricing of short-term government debt. This resulted in broad-based rotation into stocks. The Russell 2000 as well as HYG, the etf for high yielding corporate coupons, turned positive this week . As further demonstrated below (both charted below), these moves comes from nearly flat bases, a.k.a. equilibrium between buyers and sellers. For that reason, before a true trend is demonstrated by further price action, a significant amount of volatility should be expected.

Note: the consensus by Wall Street is that credit spreads will signal when the party is over. Right now we draw attention to lower oscillator lows since the June selloff, but also HYG 0.00%↑ lower highs and the possibility of a broader resolution soon with directional impact on markets.

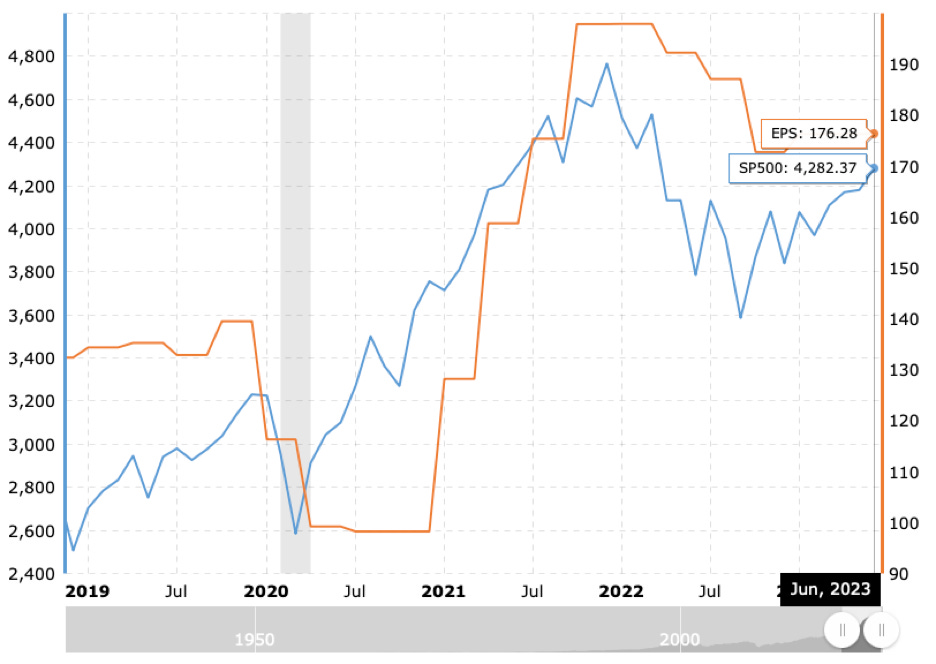

Another interesting subject as we exit results season for the first quarter 2023, we notice earnings for the S&P500 to be bucking the downtrend from 2022 likely fueling the market’s recent rally.

6) Opportunities Internationally

Continuing with the theme of globetrotting to destinations that are in the news. Going just a bit further north, let’s have a look at Sweden and see if we can understand more.

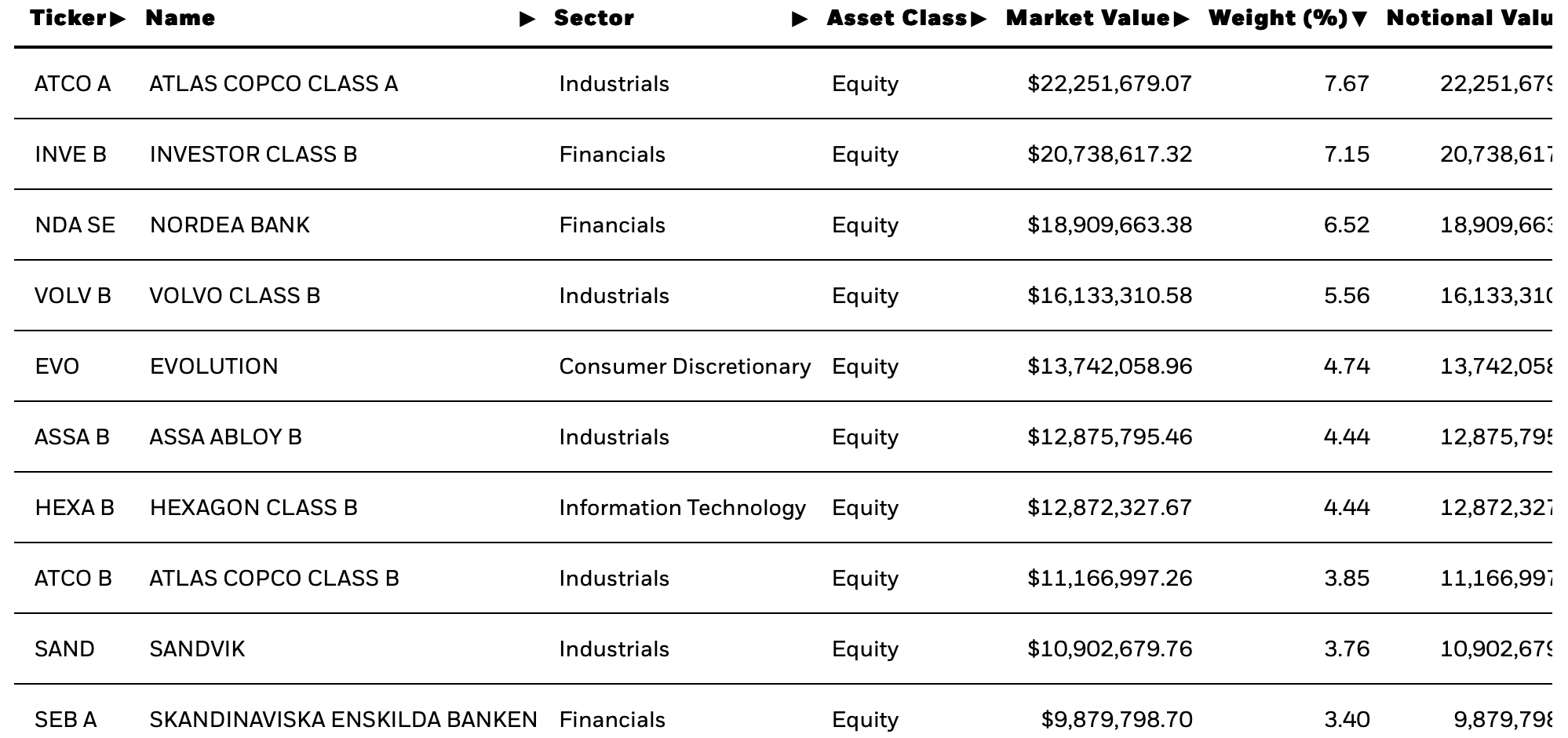

For economists, Sweden has been high on their watchlists the last several months because of the economy’s cyclical nature. Here is a look at the top holdings of iShare’s Swedish index trading on the NYSE under the ticker EWD 0.00%↑. Historically Sweden has been/is an advanced broad industrial producer, including mining. Combine this as being the north’s IT-bellweather country (Spotify, NOTE, etc), it’s understandable there is significant exposure to European growth and the interest rate cycle.

Other high quality monopolistic companies include AB SKF (a maker of ball-bearings and seals), Alfa Laval (energy and marine industries), as well as Systemair AB in building ventilation with distribution across the nordics. (Add’l international household names include; H&M, Ericsson, Telia and Saab.

However, what concerns economists the most is Sweden’s high private sector debt, and housing market. Low rates over significant time has lead to easy money in real-estate. One common theme, as the population has aged, is the lack of reinvestment in in cyclical private assets and the flow of this capital to real-estate markets with shorter cash-return cycles.

At the time of writing the most leverage real-estate developer facing re-writing of it’s debt is SBB Norden AB. Here is the recent price action, including Friday’s 50%+ significant short squeeze related to a soft landing theme.

In and when advent of bankruptcy and elimination of the equity’s value is reality, the pain will likely be felt in other companies and parts of the market.

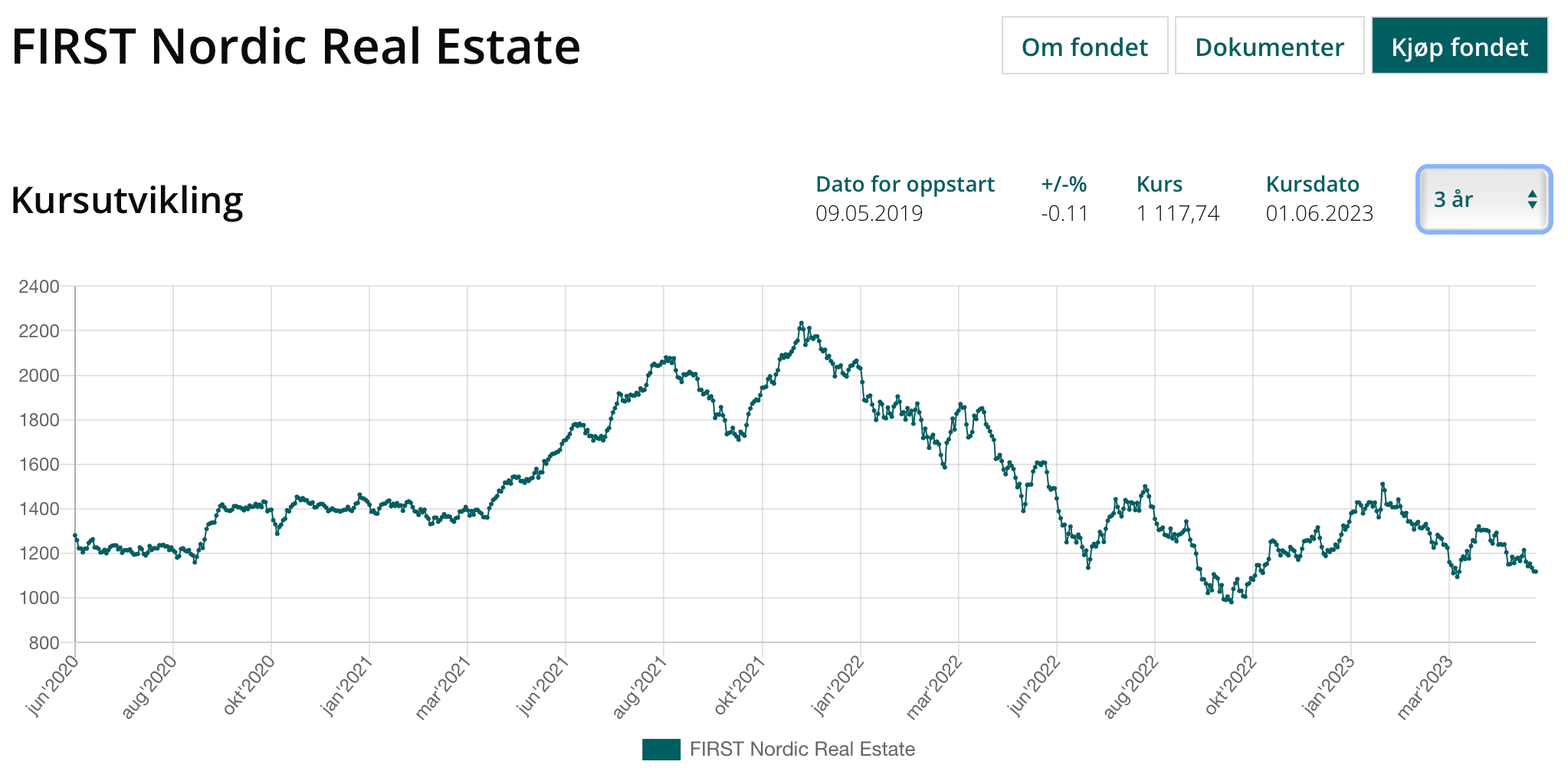

However, as can be seen looking at First’s Nordic Fund heavily invested in lower risk Swedish real-estate, prices are now comparable to the Covid low’s, already pricing in major underperformance from the sector.

If one is so inclined to take a chance now might be the time. The outlook for cyclicals is looking better. After a long period of maintenance last winter for one of Sweden’s largest atomic reactors, combined with mild temperatures, lower natural gas prices, and good conditions for wind renewable producers, inflation from energy for this industrial producer is easing.

In addition, rates are tight (positive real economy) in the North Sea, as recently reported by Solstad Offshore. One beneficiary could be Viking Supply, trading in Stockholm.

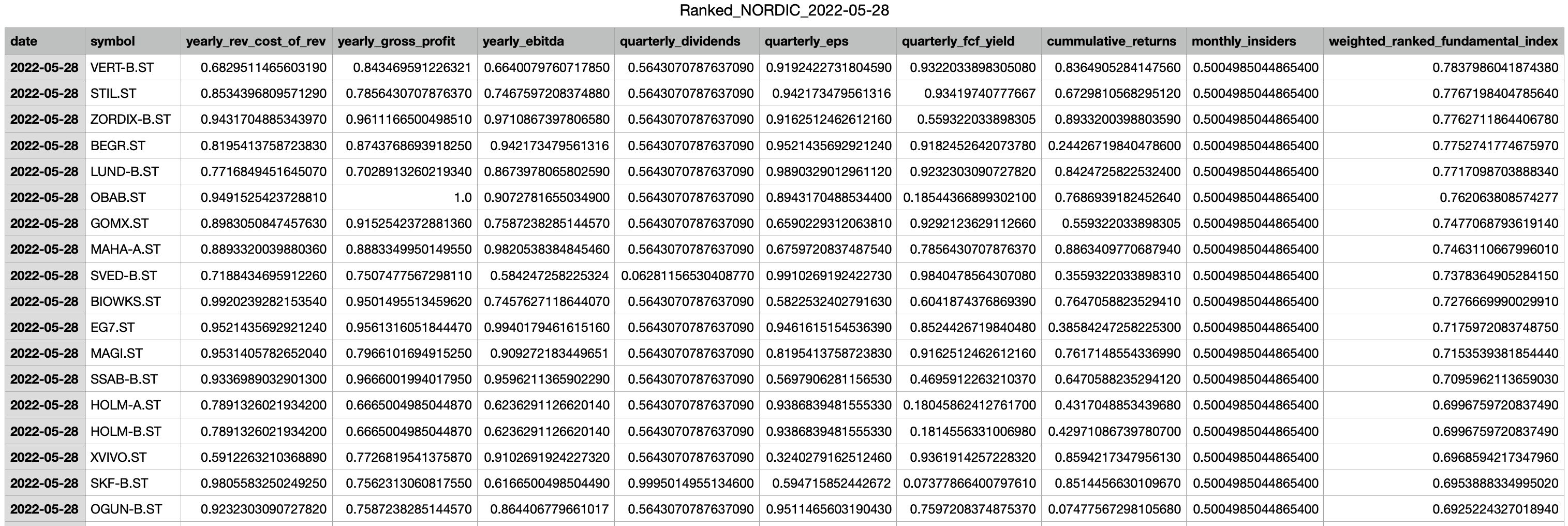

Applying a value filter, here are other name’s looking reasonably priced:

😎 Cheers! 😎

Disclaimer: Please note that the information provided in this article is for general informational purposes only and does not constitute financial, legal, or professional advice. The information provided should not be relied upon as a substitute for financial, legal, or professional advice. Before making any decision, it is important to consider all relevant information and consult with a professional who can provide personalized advice based on your specific circumstances. The author and publisher of this article cannot be held liable for any actions taken based on the information provided. This is not a recommendation to buy or sell any specific securities or financial instruments.