Short-Term U.S. Treasury Spreads

Short-Term U.S. Treasury Spreads

Mind the Gap?

Hello and welcome to another issue of 🕵 The Seeker 🕵

"The first thing I heard when I got in the business, was bulls make money, bears make money, and pigs get slaughtered. I'm here to tell you I was a pig. And I strongly believe the only way to long-term success is through strict discipline and risk management." - Stanley Druckenmiller

1) Big moves drawing attention from the last three trading days.

The main event on Friday included industry clarification related to the Inflation Reduction Act, which propelled the solar components of the renewable energy group to rise. The primary beneficiary of this development was FSLR 0.00%↑ , which closed up 26% at the top of its daily range. With such heightened attention, there was also a significant increase in short interest, as many expect this stock to re-connect with its primary trend line. The upcoming week will be crucial to monitor First Solar’s action.

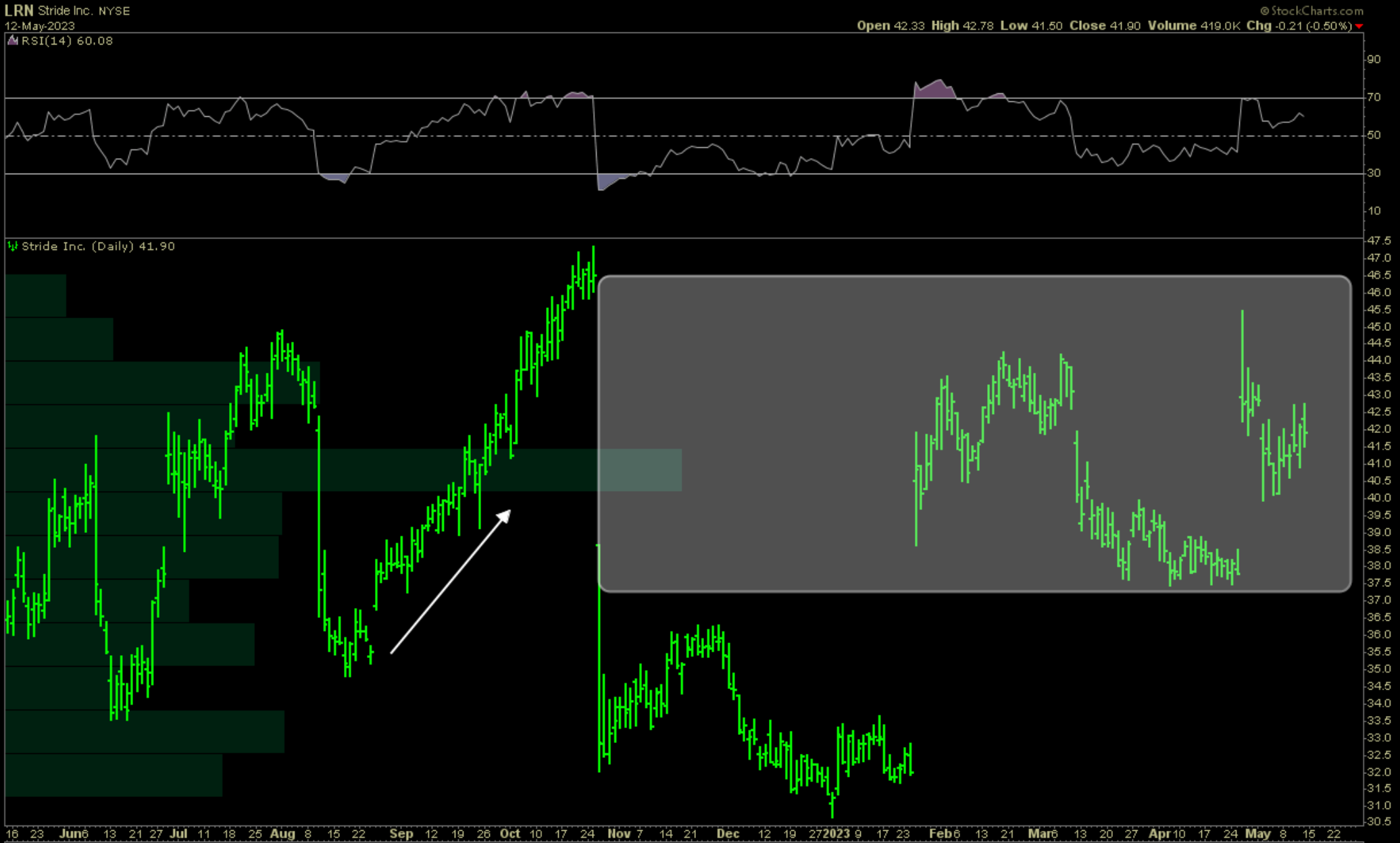

Across sectors, in the Consumer Discretionary sector, one stock standing out was Stride. After gapping up on positive earnings, it took an entirely different course compared to its counterpart CHGG 0.00%↑ . As a company prone to dislocations, LRN 0.00%↑ has a recent history of closing gaps. Once again, it’s reversing up and firmly re-establishing the gap space from last autumn for further price discovery between buyers and sellers.

Cadence Design Systems also caught our attention this week. Often a leading bellwether with seemingly predictive powers for the markets, it topped out on April 7th and continues to trend weakly. Of particular concern are the pockets of varying volume weighting beneath the current CDNS 0.00%↑ price level.

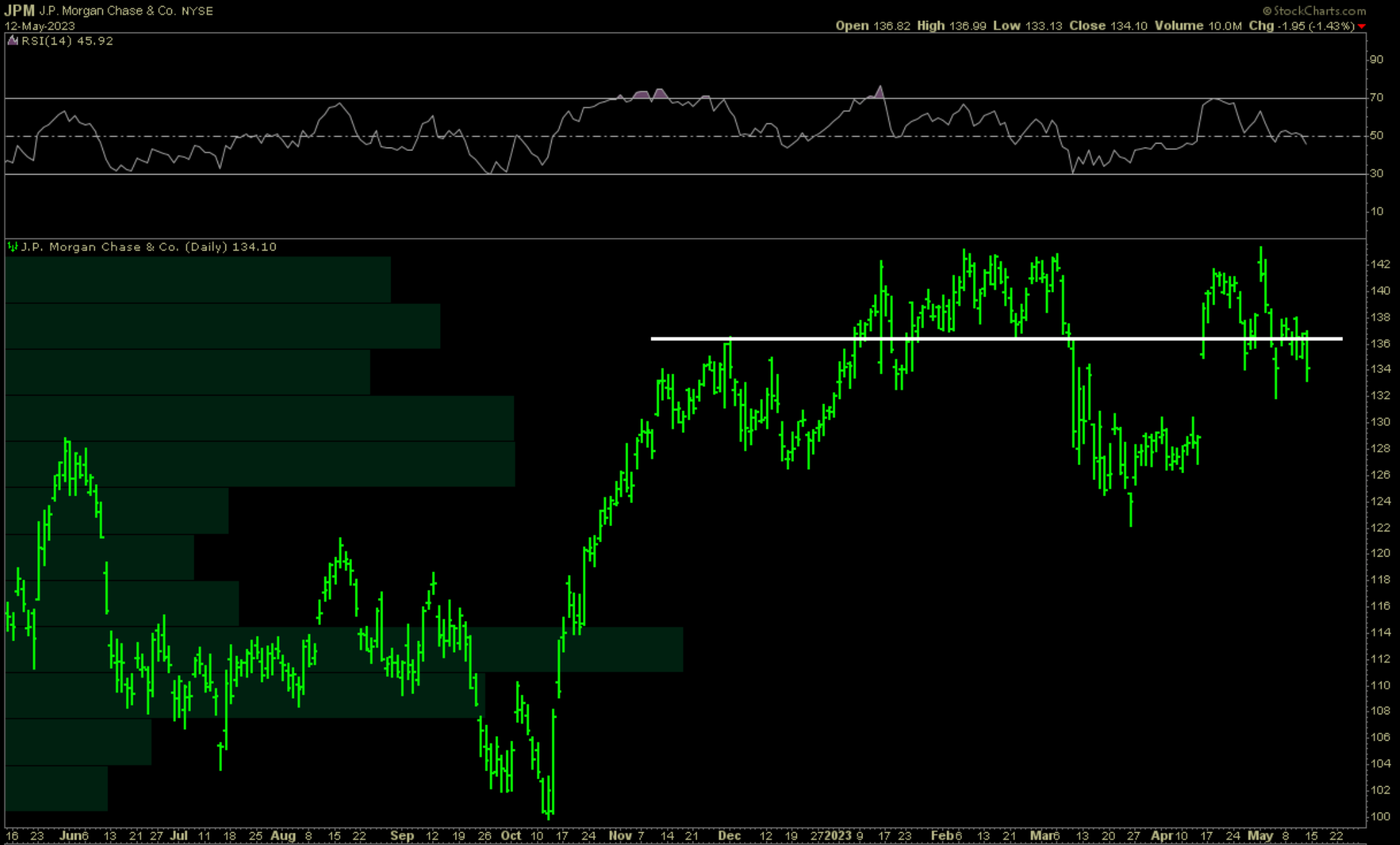

Another bellwether worth watching is JP Morgan Chase. Despite the ongoing noise surrounding banks in the U.S., it's worth noting the poor relative strength of JPM 0.00%↑ as well, with the RSI dipping below 50, despite the initial Q1 earnings positive response.

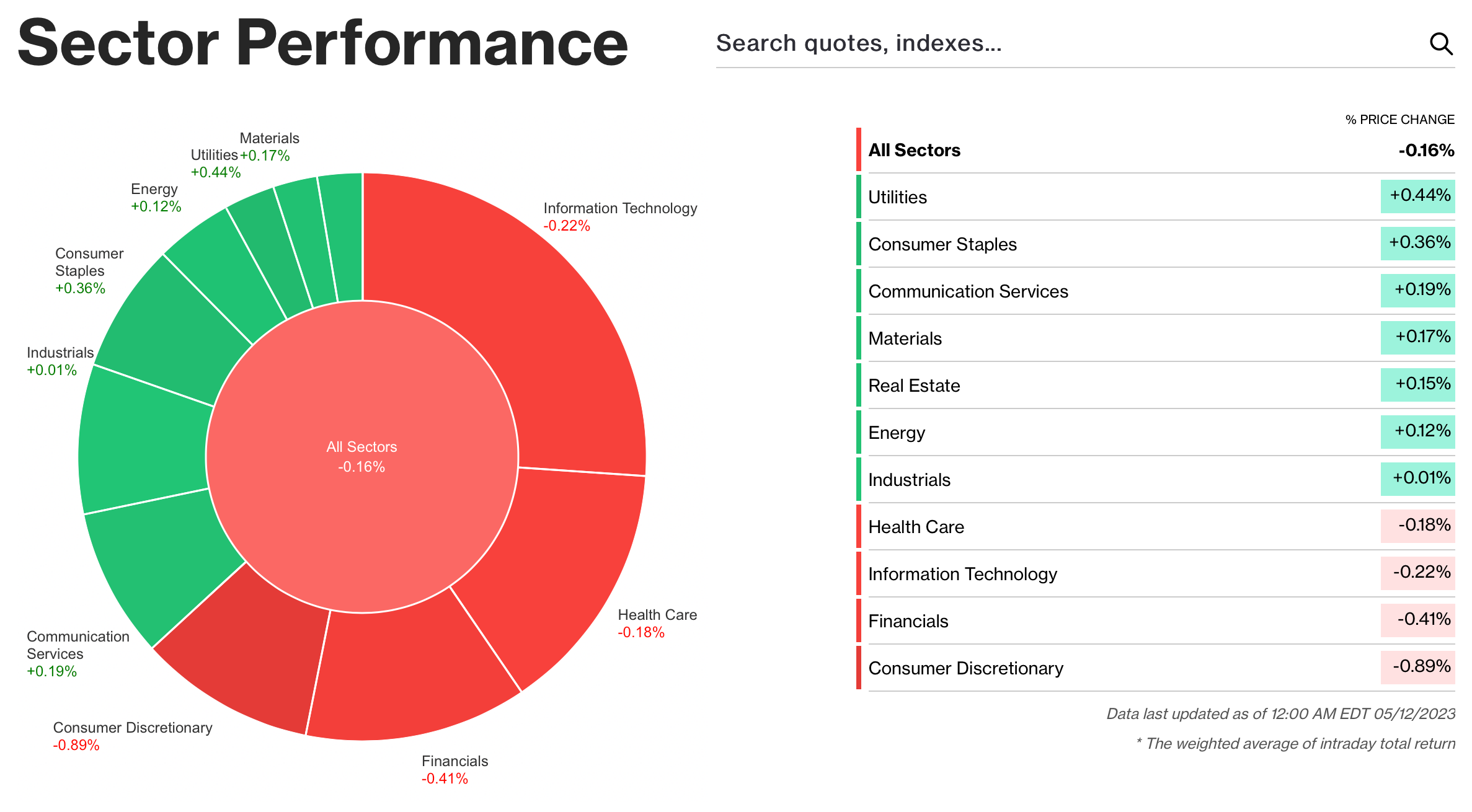

2) Sector Performance

Friday was generally a red day, with Utilities, Consumer Staples, Communication Services, Materials, and Energy leading the market in declines.

The only notably positive sector for the week was Communication Services, which gained 2.37%.

Not surprisingly much of this outperformance came from the generals in internet, and more specifically $GOOGL leading the way. However, it's equally intriguing to note that Transportation Services remains particularly strong, with $GXO as its standout performer.

Turning our attention to semiconductors, the $SMH index was slightly lower but remained relatively unchanged zooming out. Positive sentiment was maintained, with oscillator data staying above 100.

3) Earnings reports from this following week:

Names of significance from the top and bottom of the earnings results.

4) The week ahead

From Barrons:

The Calendar

First-quarter earnings season continues next week with retailers making up a larger share of the reports. Economic releases will include retail sales and housing-market data.

Home Depot reports earnings on Tuesday, followed by a busy Wednesday: Cisco Systems, Take-Two Interactive Software, Target, and TJX Cos. all report. Walmart, Alibaba Group Holding, Applied Materials, and Ross Stores publish their results on Thursday, then Deere closes the week on Friday.

The economic-data highlight of the week will be the Census Bureau'sretail sales data for April on Tuesday. Consumer spending is forecast to rise 0.7% from a month earlier, versus a decline of 0.6% in March.

Other data will include the Conference Board's leading economic index for April on Thursday, and several indicators of the U.S. housing market: The National Association of Home Builders' housing market index for May on Tuesday, the Census Bureau's new residential construction data for April on Wednesday, and the National Association of Realtors'existing-home sales for April on Thursday.

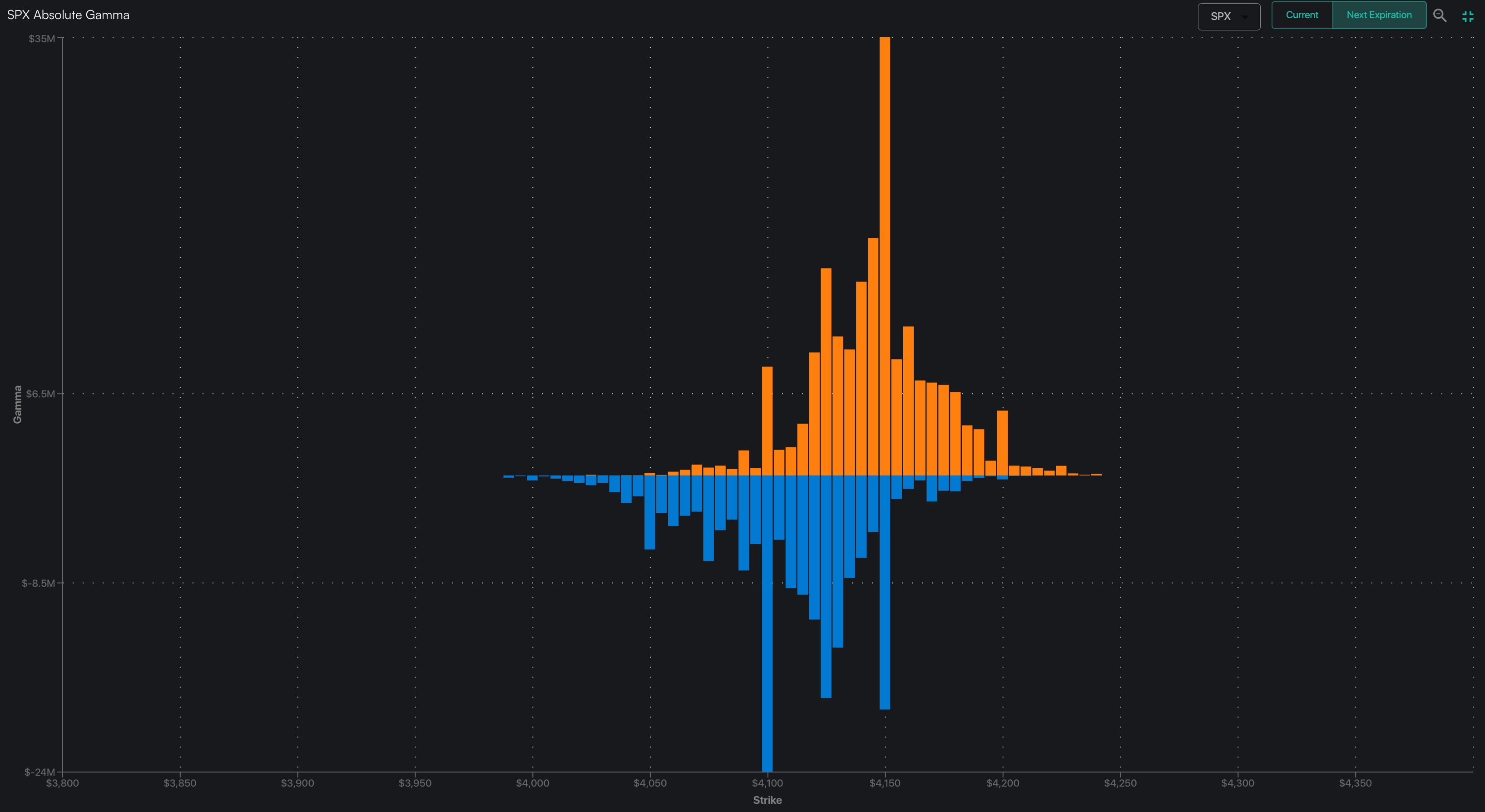

Options market positioning for monthly expiration on May 19th.

5) Macro conditions

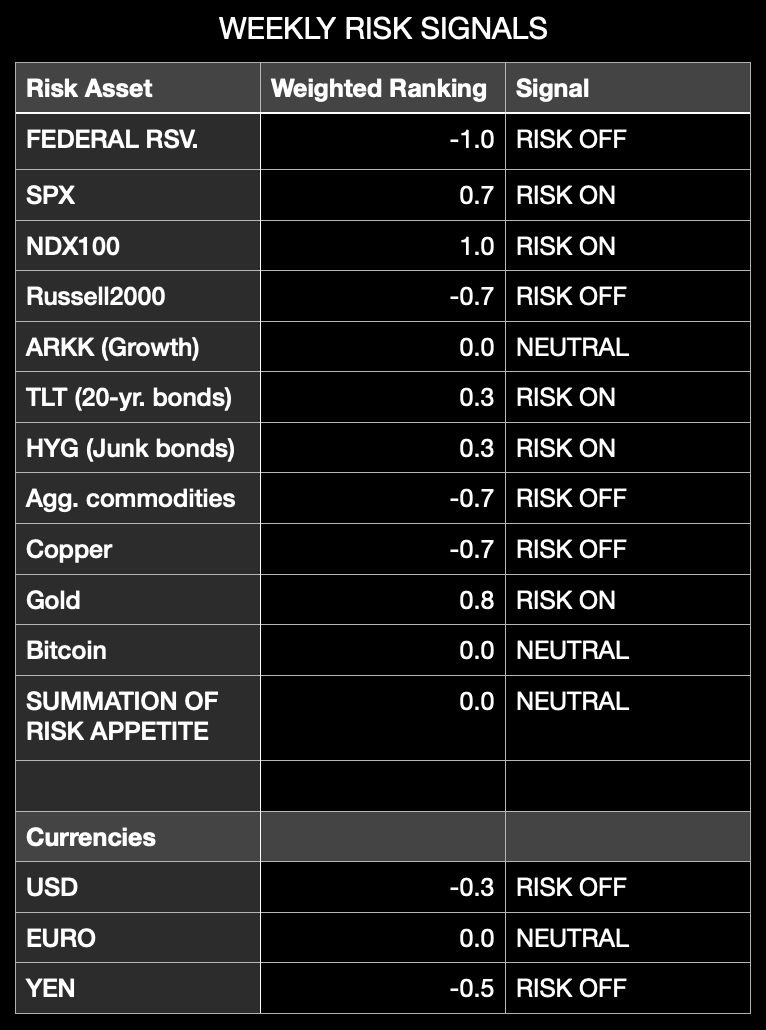

Weekly risk signals are based on intermediate and long-term trend in markets, as well as money flows into or away from asset classes. Not included are potential fundamental or gamma implied volatility tail risks.

Note: top traders themselves have a hit rate approaching the 50% lower bound. Controlling risk on losing positions and letting winners prosper is for many the difference in creating a successful track record over time.

Last week, we highlighted the USD in this segment. $UUP did, in fact, strengthen significantly, moving up 1.59% for the week. This caused ripples in the Euro and Yen markets. One can speculate on the reasons for changes in dollar liquidity. It should not be ruled out that markets could return to an environment driven by macro factors, as experienced through much of 2022.

When looking at indexes like VVIX or the newly created VIX for options with less than 1-day to expiration, and also considering the graphical relationship of the spread between 1-year vs. 1-month US Treasury bonds, a dramatic dislocation has/is occurring.

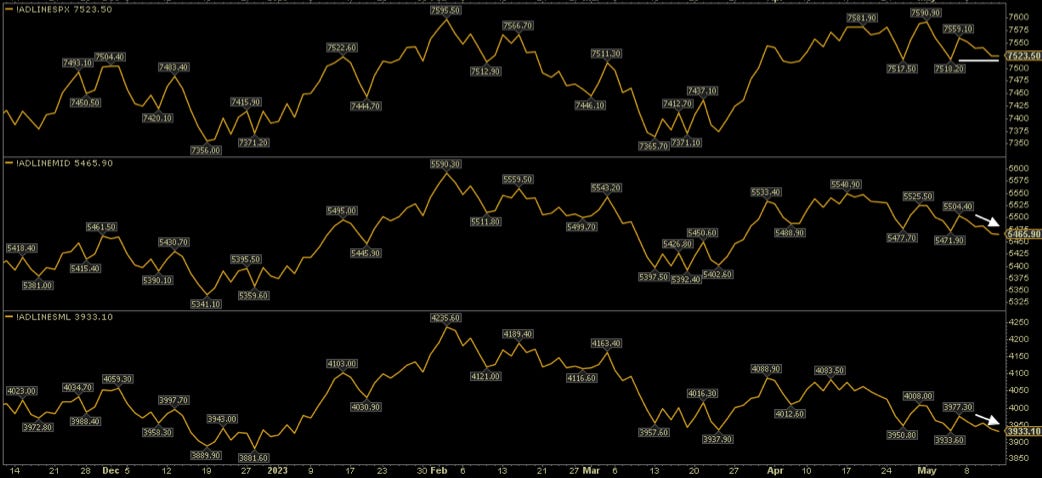

However, what does Mr. Market think? Judging by market capitalization, mid- and small-cap stocks are already being re-rated more severely than their large-cap (growth) counterparts. This chart of advancers vs. decliners from the NYSE highlights this divergence.

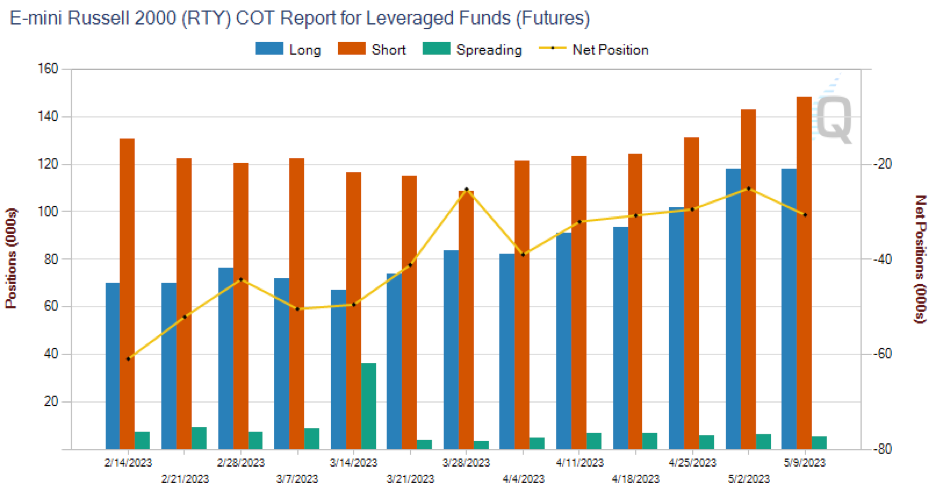

This has not gone unnoticed by hedgers either. Weekly data from the COT shows net short positioning building by funds in the contract for Russell 2000.

Are these leading indicators for further risk-off or is re-pricing well underway for America’s most economically sensitive companies?

😎 Cheers! 😎

Disclaimer: Please note that the information provided in this article is for general informational purposes only and does not constitute financial, legal, or professional advice. The information provided should not be relied upon as a substitute for financial, legal, or professional advice. Before making any decision, it is important to consider all relevant information and consult with a professional who can provide personalized advice based on your specific circumstances. The author and publisher of this article cannot be held liable for any actions taken based on the information provided. This is not a recommendation to buy or sell any specific securities or financial instruments.