RSI 86

Hello and welcome to another issue of 🕵 The Seeker 🕵

"If you want to be a great investor, you have to be a learning machine." - Mohnish Pabrai

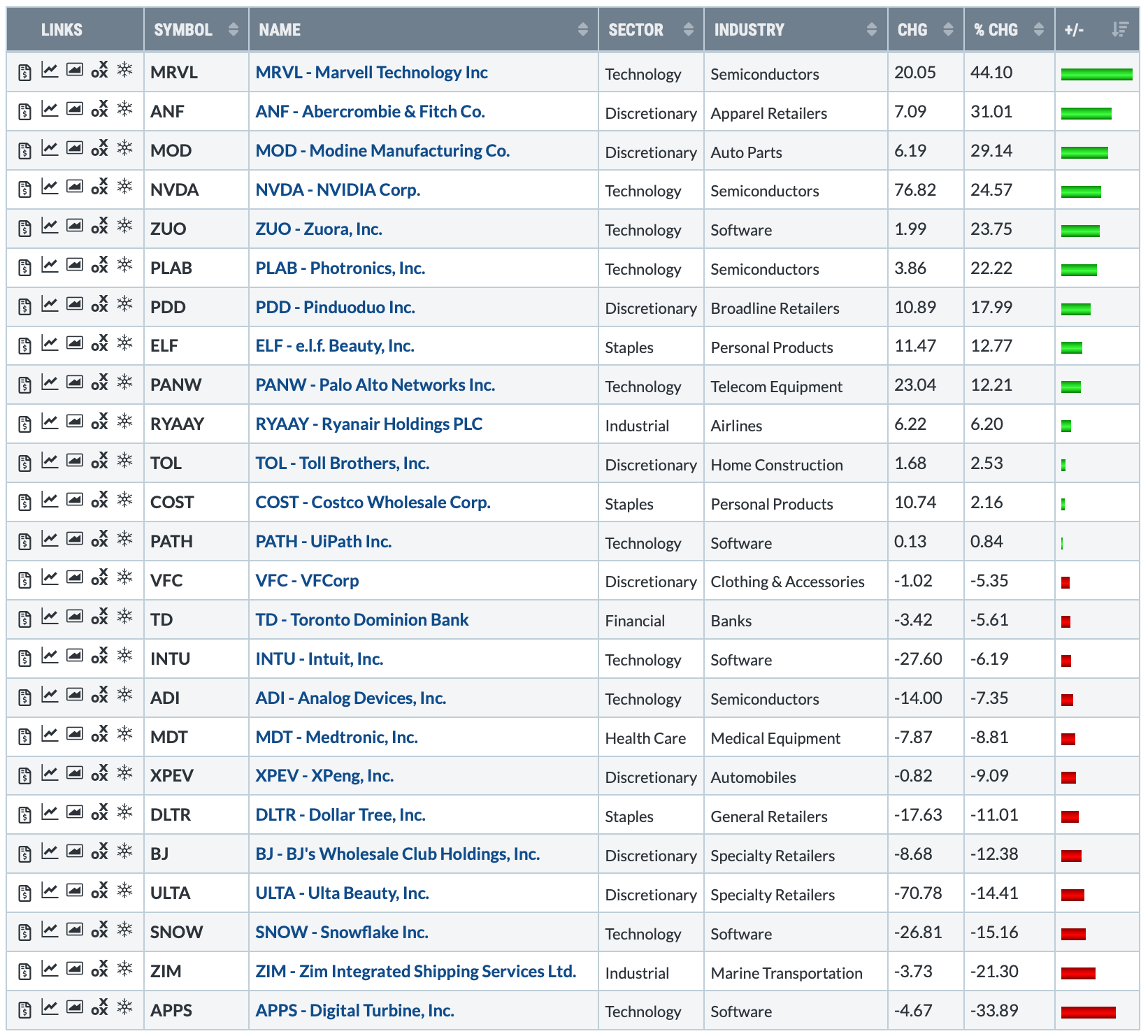

Big moves drawing attention from the last three trading days.

Photronics had a highly successful week, benefiting from favorable industry trends in the semiconductor sector and achieving a record quarter. The company reported earnings per share (EPS) of $0.54, a notable increase from the previous quarter's $0.43. Moreover, their guidance for the upcoming quarter shows positive improvement when compared to estimates. On the technical side, the PLAB 0.00%↑ weekly chart demonstrated strength by rejecting a head and shoulders pattern, ultimately breaking out to the upside.

This week, encouraging signs were also developing at Lithia Motors. After experiencing some selling pressure around earnings, buyers have now returned, pushing the company's share price higher. Previously, the stock price was constrained by overhead resistance, but is now showning signs LAD 0.00%↑ of meaningfully breaking through that barrier.

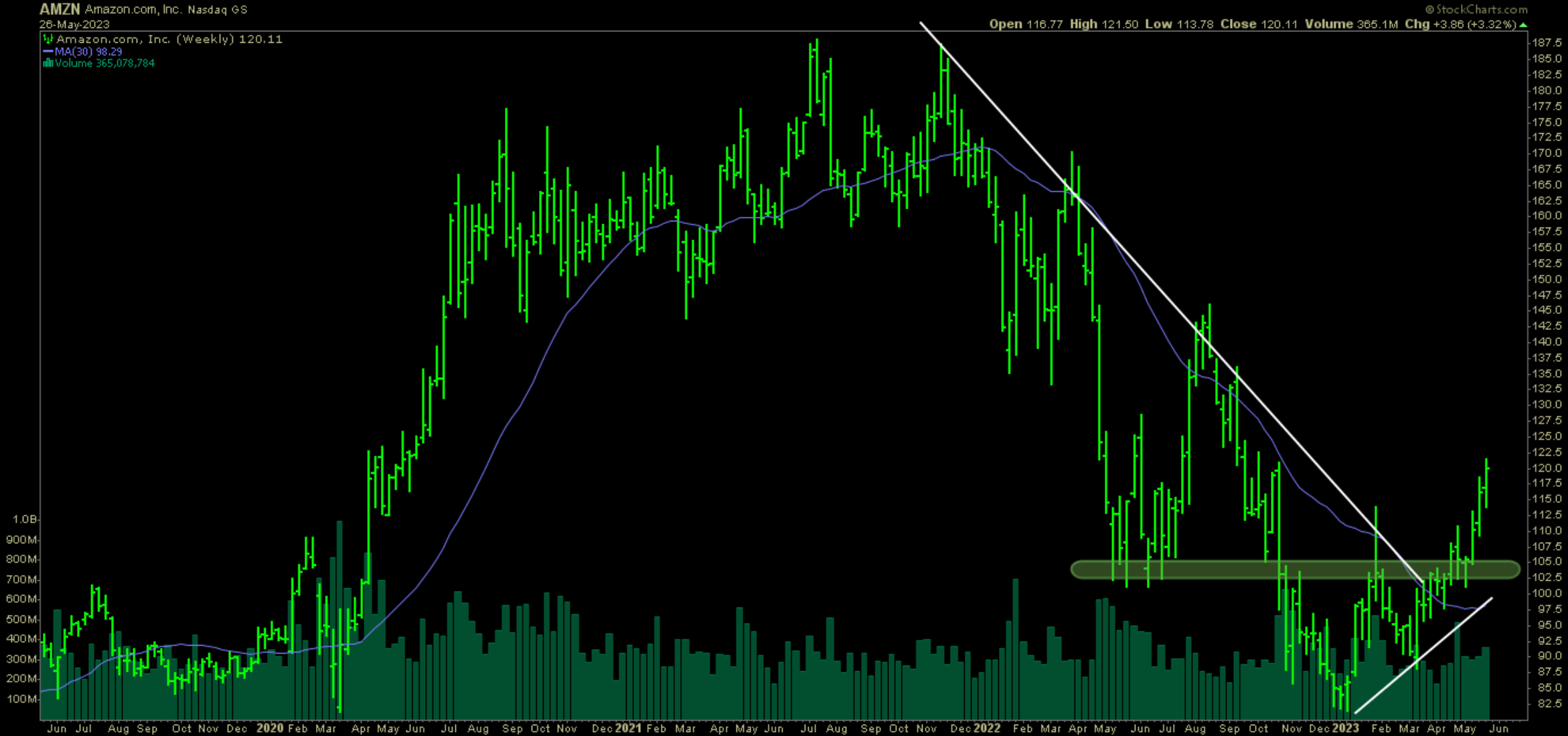

Another company worth keeping an eye on this week is Amazon. Despite the banking turmoil that unfolded in March, AMZN 0.00%↑ managed to break through its steep downward trend and surpass its May 2022 low, as shown on the weekly chart. Since then, Amazon has demonstrated resilience, continuing to thrive even in the face of increased competition for AWS (Amazon Web Services) and a potentially weakening American consumer market. These developments provide food for thought for contrarian investors seeking opportunities within the consumer discretionary sector.

Following the appearance of "for sale" signs at PacWest Bancorp, one noteworthy potential buyer has emerged in the form of Scion Asset Management, led by Michael Burry, who has taken up a new ownership stake. As a result, short interest in the company has declined from its peak. However, when the firm recently announced new asset sales, the market response was tepid. Despite this, PACW 0.00%↑ has shown resilience by rejecting its downward trend, even as the banking industry as a whole is preparing to navigate storm clouds from further projections of the Federal Reserve increasing lending rates.

Sector Performance

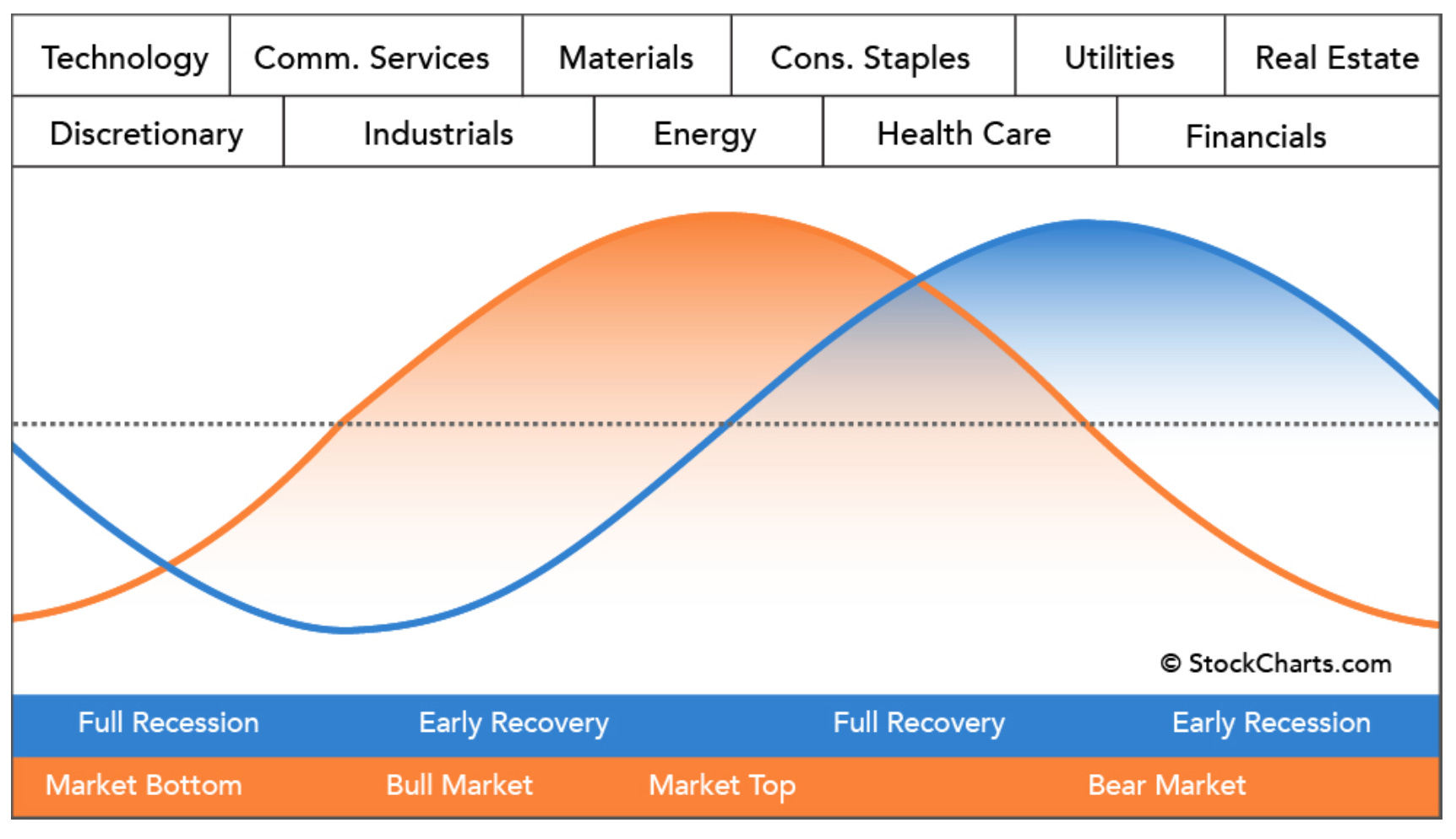

Friday saw NYSE and Nasdaq pushing on full stream ahead into the holiday weekend. XLK, XLY and XLC provided leadership, marking common bull market trends.

However, when looking at the broader picture for the week, the outlook was less optimistic. Only the Tech, Communication Services, and Consumer Discretionary sectors, including companies like Amazon, managed to show positive performance by finishing in the green.

Other offensive sectors like Financials, Materials and Energy didn’t garner the same interest from investors, likely following normal market cycle playbook.

A stock pickers market?

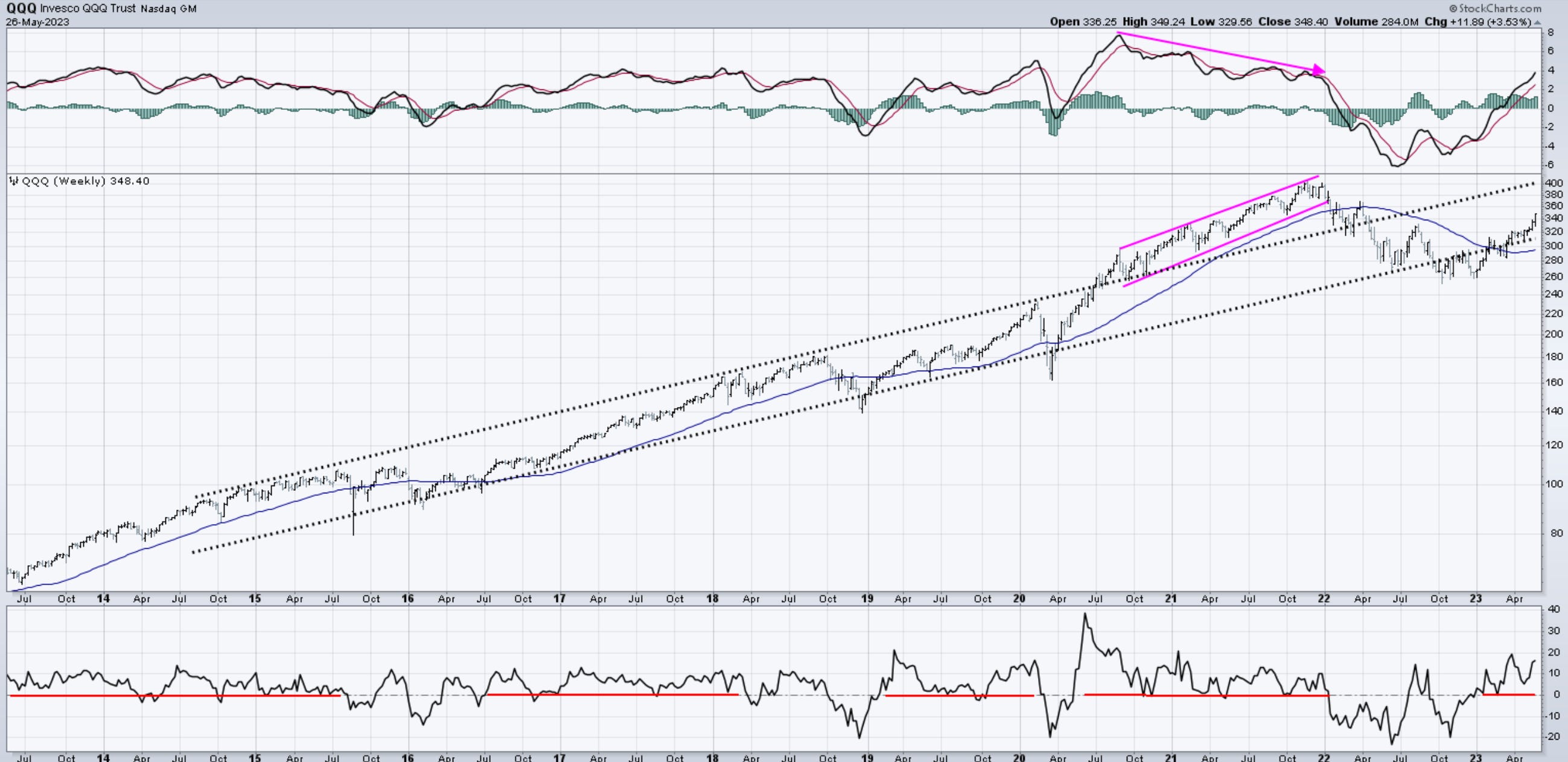

Tech stocks have continued to outperform, as evidenced by the performance of QQQ 0.00%↑ , the popular investment choice for the Nasdaq100. QQQ is now comfortably situated within its long-term channel, which has provided investors with a convenient framework for the past decade, alleviating the need for extensive individual stock analysis.

One component that didn’t have such a stellar week however was Analog Devices. On contrary display to market technicians, visible weak performance relative to it’s peers resulted in ADI 0.00%↑ a sudden re-rating triggered by earnings.

Semiconductors

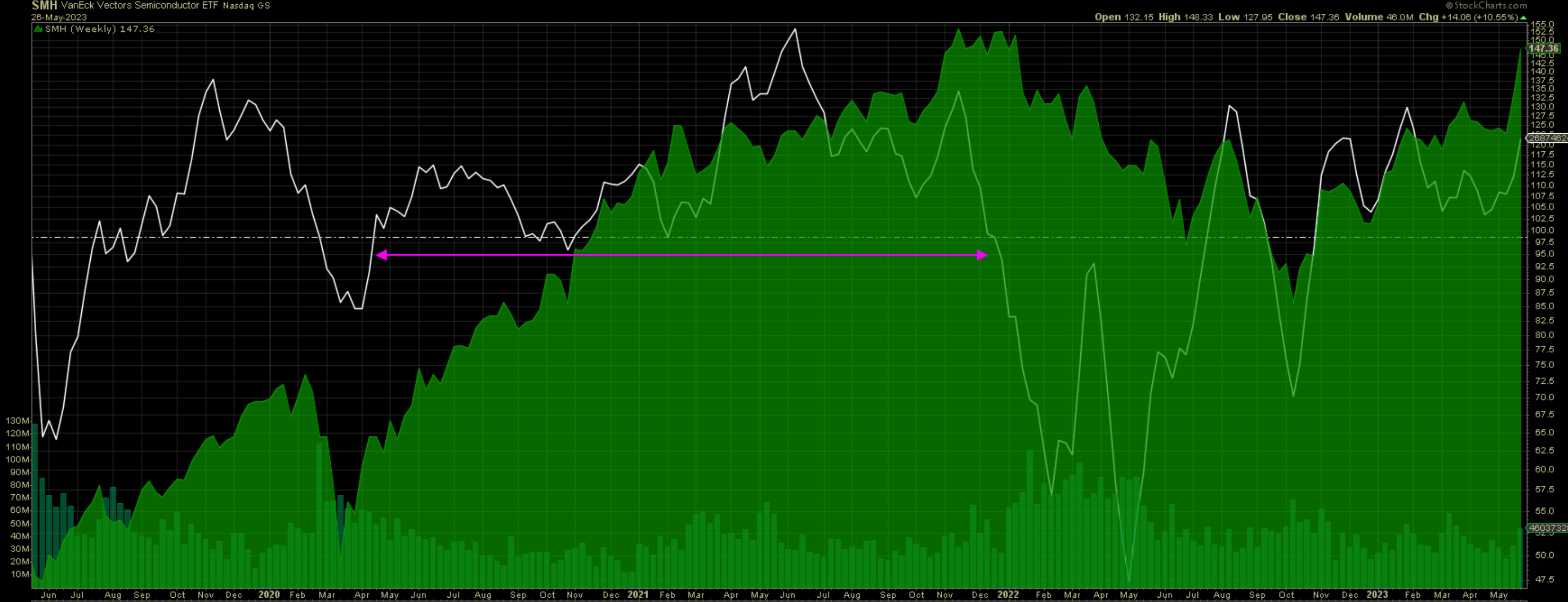

At QuantFactory, we won't spend an excessive amount of time stating the obvious, but the semiconductor sector had another exceptional week, with Nvidia leading the way and spreading goodwill across the industry.

Returning to the price oscillator, we want to look at where the SMH is now compared to it’s record run in 2020 and 2021. For a stretch of nearly two years momentum strength remained firmly intact, bare dipping negative on the odd occasion.

Take aways in/on/around/from a bubble

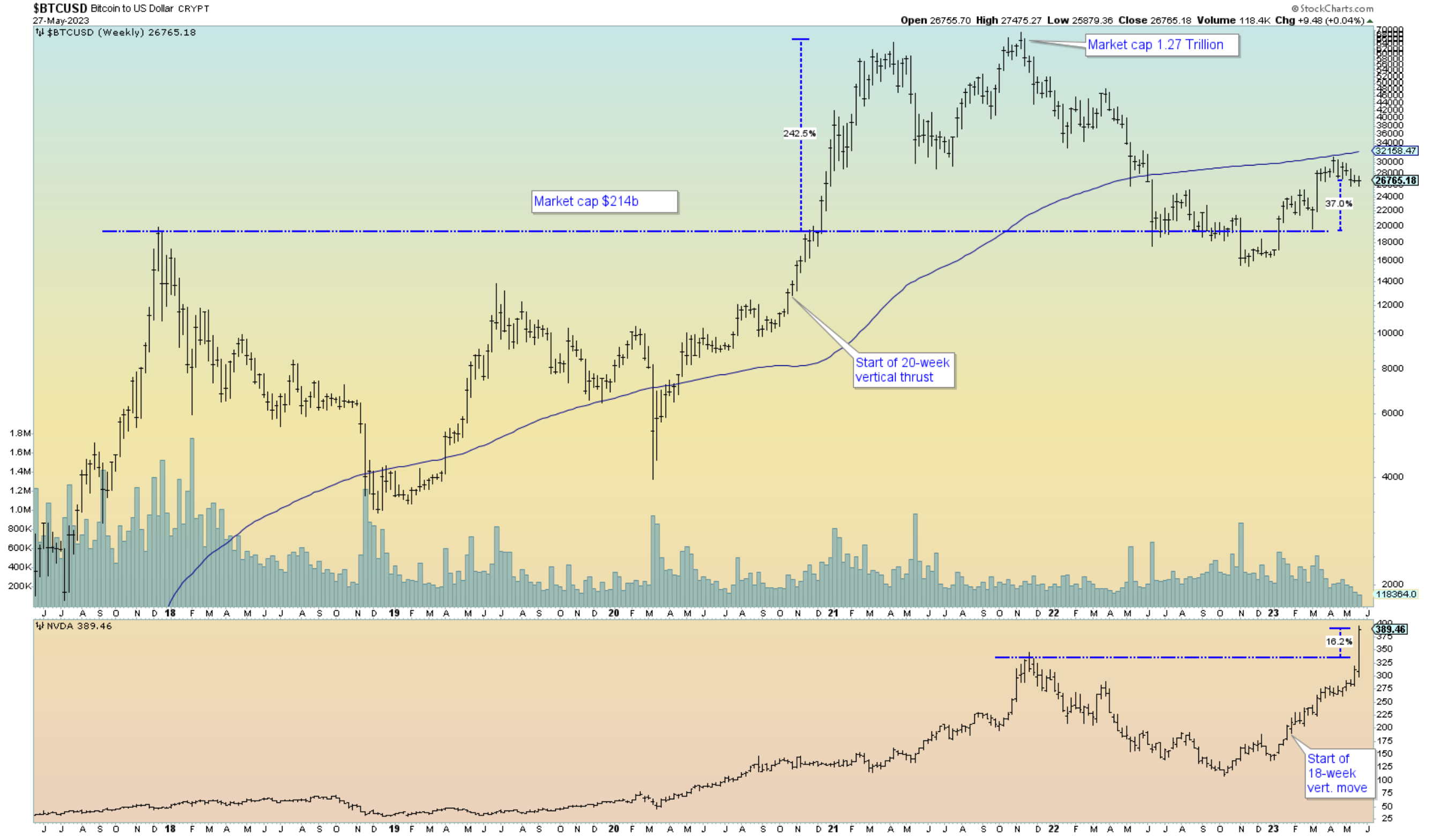

Below is a chart depicting the performance of Bitcoin over the past five years, with NVDA displayed beneath. During the peak of Federal Reserve liquidity injection, Bitcoin experienced a significant breakout, surpassing its previous high of $20,000 and entering a new phase of speculative fervor. Over the following eight months, Bitcoin delivered extraordinary returns and witnessed substantial market capitalization growth. Can we draw any lessons from this phenomenon that may apply to other assets, especially NVDA?

NVDA 0.00%↑, currently trading at an impressive valuation of over 30 times its sales, has been experiencing a prolonged and uninterrupted bullish trend. In this author’s opinion it would be beneficial for the stock to undergo a period of consolidation at this stage. It is worth noting that the collapse of FTX, Luna, and Two Arrows last year revealed that margin trading, especially with leverage as high as 100x on various crypto exchanges, played a significant role in driving these extraordinary price movements. Considering the macro perspective, does this justify a further push towards AI exposure? For sure.. Does Nvidia have what it takes to reach $1T market cap++? Probably, including all possible outcomes of a mania, include also leverage, exit liquidity and bagholding.

Earnings reports from the prior week:

Weekly results from some names of significant interest.

The week ahead

From Barrons:

The Calendar

U.S. stock and bond markets will be closed on Monday for Memorial Day. This newsletter will be off, as well, and back in your inboxes on Tuesday night.

Tuesday kicks off a busy week of earnings reports and job-market data.

Earnings highlights will include results from Hewlett Packard Enterprise and HP Inc. on Tuesday, then Advance Auto Parts, Chewy, and Salesforce on Wednesday. Broadcom, Dell Technologies, Dollar General, and Lululemon Athletica report on Thursday.

On Wednesday, the Bureau of Labor Statistics will release the job openings and labor turnover survey, or JOLTS, for April. Economists are expecting a slight decline to 9.44 million job openings on the last business day of the month.

That's ahead of Jobs Friday, when the the BLS is expected to report a gain of 200,000 nonfarm payrolls in May, after a 253,000 increase in April. The unemployment rate is expected to tick up by a tenth of a point, to 3.5%.

Other economic data to watch next week include the Conference Board's consumer confidence index for May on Tuesday and the Institute for Supply Management's manufacturing purchasing managers’ index for May on Thursday.

--Nicholas Jasinski

Macro conditions

Weekly risk signals are based on intermediate and long-term trend in markets, as well as money flows into or away from asset classes. Not included are potential fundamental or gamma implied volatility tail risks.

Note: top traders themselves have a hit rate approaching the 50% lower bound. Controlling risk on losing positions and letting winners prosper is for many the difference in creating a successful track record over time.

This week encompassed various significant events, highlighting the importance of disruptive innovation in our era. Positive revisions in GDP, a turnaround in oil reserves, and a notable decrease in core inflation supported the case for further Fed rate hikes.

However, general risk appetite remained weak for the second consecutive time, while the focus continued to be on the reversal of the dollar using UUP 0.00%↑.

At the time of publishing, there seems to be a potential deal in the works between Congressional leadership and the White House for resolving the US debt ceiling standoff. As the dollar approaches gap resistance, it becomes an interesting point to monitor for potential rejection at this level or as an indicator of increased risk-off sentiment impacting short-term lending rates.

Nevertheless, much attention has been drawn to the lackluster participation of small and mid-cap stocks in the market. The chart below depicts the performance of SPY 0.00%↑ (S&P 500 ETF) and compares it to the correlation of its equal weight counterparts. It is evident that the weighted index, driven by momentum, has demonstrated the ability to deliver positive results in various market environments, even during periods when value stocks may have fallen out of favor.

Opportunities Internationally

Germany

This week headlines emerged of German GDP dipping negative. This -0.2% print surprised exceptions to the downside.

This came on the heels of a new all-time high in the German DAX40.

The transition to EV and outperformance of luxury has bolstered this indices returns since the autumn lows, and it’s possible this low may have been a generational buying opportunity to buy cheaply some of these iconic companies.

Markets have also benefited from a "Goldilocks" scenario characterized by 2% interest rates. This can be observed in the following chart depicting the 10-year yield in the German Bund.

If rates are encounter resistance at historical points, a rotation to higher beta quality growth may be likely, including other notables such as BioNTech (cancer pipeline+AI), Adidas, Puma, Siemens Energy(infrastructure incl. wind), Zalando, and Hello Fresh.

From Heidelberg Cement:

The Brevik CCS project

With 400,000 tonnes of CO₂ to be captured annually and transported for permanent storage, HeidelbergCement will realise the first industrial-scale carbon capture and storage(CCS) project at a cement production facility in the world at Brevik. The CCS project in Norway is an important cornerstone in our climate strategy: It will enable HeidelbergCement to reduce greenhouse gas emissions related to the cement production process.

😎 Cheers! 😎

Disclaimer: Please note that the information provided in this article is for general informational purposes only and does not constitute financial, legal, or professional advice. The information provided should not be relied upon as a substitute for financial, legal, or professional advice. Before making any decision, it is important to consider all relevant information and consult with a professional who can provide personalized advice based on your specific circumstances. The author and publisher of this article cannot be held liable for any actions taken based on the information provided. This is not a recommendation to buy or sell any specific securities or financial instruments.