Navigating Quad Witching

Hello and welcome to another issue of 🕵 The Seeker 🕵

“If you do the right thing with your money, you'll have more of it." - Shaq

Dear readers this week we are going to do something a little different, since market trends are ‘stabily’ defined and sentiment remains little changed, we’re going to hone in on the week ahead. Let’s contemplate upcoming events and their possibilities for impacting stocks. Could they cause a shift in the current market regime? Are there any fat pitches setting up?

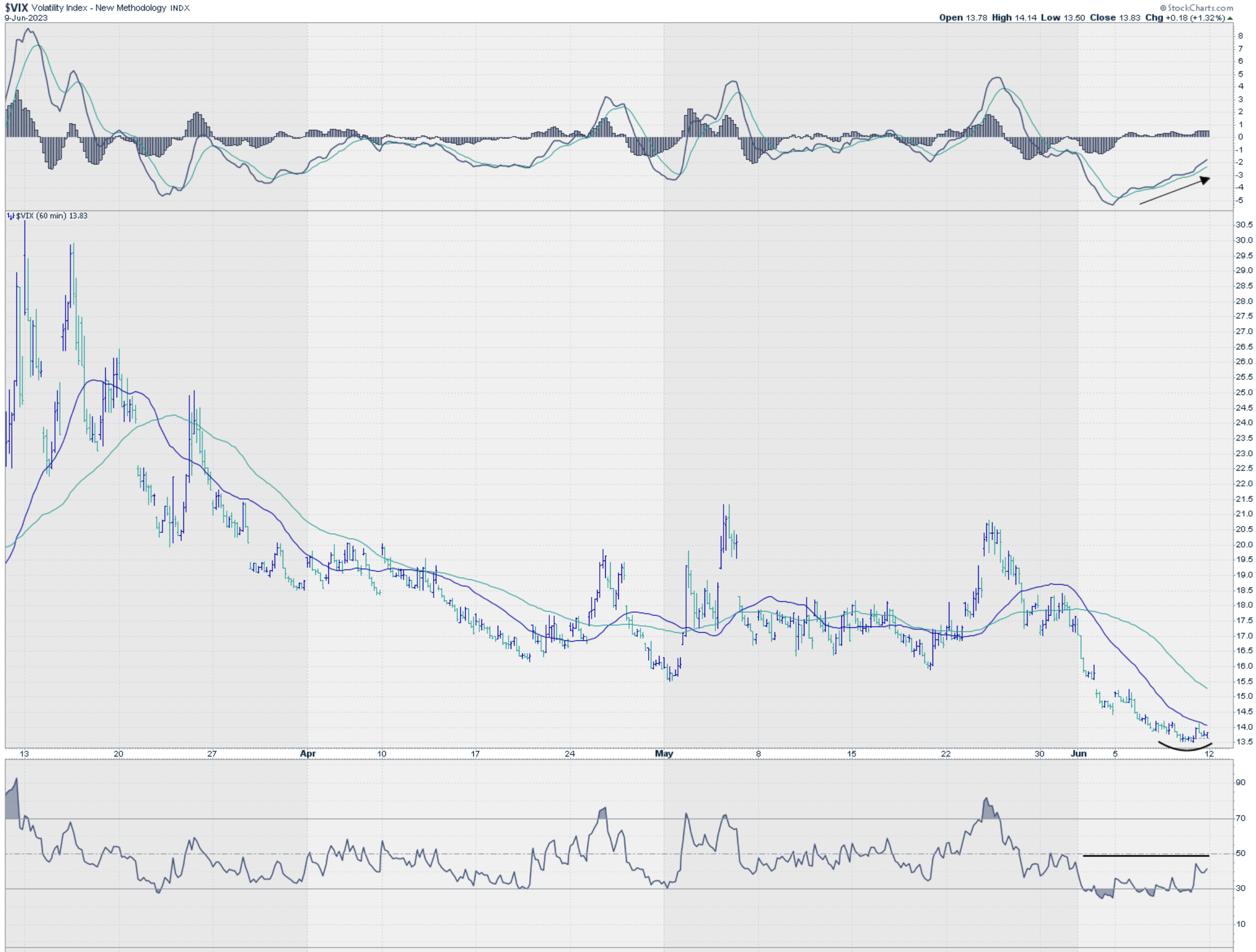

The last trading day of the week represents only one day of data, but the VIX warrants attention. Market’s closed up Friday, and so did the VIX(*). Looking at a 60-minute chart, there is a slight positive divergence setting up, with momentum on the rise, and price’s downward motion stalling out.

*This happens often in simple stocks but not so often on the SPY

RSI however remains below 50 not ready to confirm yet a reversal. Is there a reason to give more importance to the ebbs and flows of the put options on the SPY now, rather at any other point of this recent 4-month crushing of the VIX that’s been witnessed?

I recently asked ChatGTP for a short summary of Quad Witching. Here is the response:

First thing that is apparent, is that the last major options expiration was in March. Following a harsh slap on the wrist for equity owners then, the reversal in markets and ability to follow-thru up and to the right has been admirable.

We’ve recently observed call buying exceeding put buying at levels returning to the 2021’s record setting range. Here is a smoothed out chart looking at 5-day moving average of the CBOE put/call ratio (inverted).

Another way to look at this is charting just how much in the money premium is baked into the major indices at current price levels. Looking across future expiries, we can also see that call buyers are currently being better rewarded that the bears.

Taking a look at the indices, current trends of higher highs and lower lows are established, but are these levels we want to put new money to work?

Price of large cap technology is being obviously lead by secular tailwinds. After consolidation at this level(s) a few more weeks time, more interest could be warranted; a pull-back however would still fall in the realm of healthy for it’s constituents.

A significant move by S&P500 with confirmation; a re-test and hold would appease any worries that economic woes are behind.

IWM still not a significant price levels for overweighting the group by technicians. This week’s positivity a step in the right direction.

It’s possible with QuadWitching, market makers could be forced to stay locked into their positions, firmly managing risk and maintaining a positive upward drift to markets, but given the opportunity for reversal and de-leveraging move to the downside could be stark. These levels might represent important levels for pullback buying or major sentiment shift.

Here is a list of the most liquid options names from the CBOE:

Knowing now what market regime we are in and that there is a structural reason for higher focus this week. Let’s check the calendar.

From Barrons:

The Calendar

Next week is big one on the economic data and policy fronts. Investors will contend with major inflation data and central bank meetings, plus other economic and earnings releases.

The Federal Reserve's monetary-policy committee will announce a decision on Wednesday. Futures markets are overwhelmingly pricing in a pause in interest rate hikes. The European Central Bank is widely expected to raise its target interest rate by a quarter of a percentage point on Thursday.

The Bureau of Labor Statistics will report the consumer price index for May on Tuesday, followed by the producer equivalent on Wednesday. The consensus estimates are for increases of 4.2% and 1.5%, respectively.

Other economic data out next week includes the National Federation of Independent Business' small business optimism index for May on Tuesday, the Census Bureau's retail sales data for May on Thursday, and the University of Michigan's consumer sentiment index for June on Friday.

Earnings reports will come from Oracle on Monday, Lennar on Wednesday, and Adobeand Kroger on Thursday. Home Depot will also host an investor day on Tuesday.

--Nicholas Jasinski

Expectations when the FOMC meets this week are for them to hold borrowing rates unchanged. A pause is undoubtably a welcome event but very likely built into markets now. Looking further out, participants are pricing in little to no chance of the Fed keeping rates here “for longer.” This optimism was backed up by new data this week, including rising jobless claims and a weak ISM survey.

With the pause upon us, there is the chance of this being a hawkish event, where markets could enter a turbulent period, where freshly peaked optimism meets, tightening credit, stubborn inflation and a Federal Reserve without further options.

Here is a backward looking chart of CPI. Notice that in August of last year, and the next two month, there was little upward pressure on CPI. This means that it will take significantly soft readings this year to push our inflation readings lower in the summer and autumn.

When we put it together, what does this all mean?

I wouldn’t rule out that equities can push higher. More rotation into a broader cross-section of stocks would increase general optimism. However, the size of the moves up and down may also increase as the pull and tug of the VIX increases.

Bonus…Some charts being watched (in random order)

😎 Cheers! 😎

Disclaimer: Please note that the information provided in this article is for general informational purposes only and does not constitute financial, legal, or professional advice. The information provided should not be relied upon as a substitute for financial, legal, or professional advice. Before making any decision, it is important to consider all relevant information and consult with a professional who can provide personalized advice based on your specific circumstances. The author and publisher of this article cannot be held liable for any actions taken based on the information provided. This is not a recommendation to buy or sell any specific securities or financial instruments.