Insightful Charts - 2023/11/13

Insightful Charts - 2023/11/13

Plus latest news from the market

This is The Seeker with the latest on the stock markets. You can send questions, comments, and suggestions by clicking the button.

No More Rate Hikes: For Now

Fed Chair Jerome Powell indicated that the central bank is not ready to end its historic interest-rate increases until there is more evidence of cooling inflation. Despite the recent easing of price and wage pressures, Powell emphasized in a speech that the Fed is more likely to tighten policy than ease it if any changes are necessary. He mentioned past instances of inflation "head fakes" and emphasized the need to monitor economic conditions closely to avoid being misled by short-term data. While the Fed has raised interest rates to combat inflation, Powell left the possibility open for keeping rates on hold or raising them again next year based on economic and inflation trends. The recent pause in rate increases is the first since March 2022. Powell acknowledged the challenge of lowering inflation sustainably to the 2% goal and highlighted the potential difficulty if supply-side tailwinds diminish. The next Fed meeting is scheduled for December 12-13.

“We’re trying to make a judgment at this point whether we need to do more.”

—Fed Chair Jerome Powell

Recent Highlights From The Earnings Reports

The Aerospace & Defence Transdigm Group TDG 0.00%↑ reported strong numbers, sitting at $8.03 EPS.

Wynn Resorts WYNN 0.00%↑ reported $0.99 EPS, beating the estimates with 34.13%.

MGM Resorts MGM 0.00%↑ reported $0.64 EPS, beating the estimates with 22.64%.

Biogen BIIB 0.00%↑ reported $4.36 EPS, beating the estimates with 9.73%, but still suffered a 3 day losing streak. Morgan Stanley, adjusted their target price to $373 from $361, and still maintain their Overweight rating.

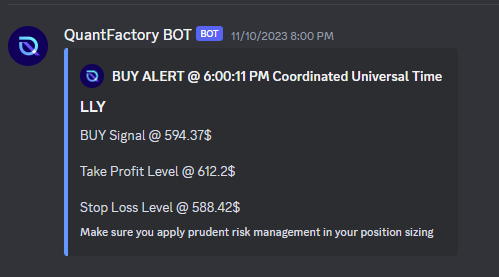

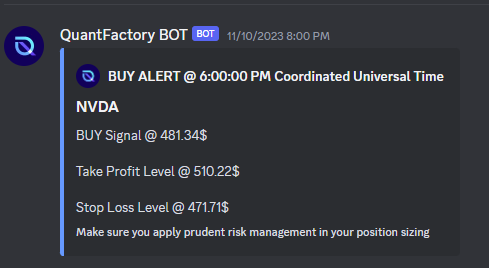

Recent Signals From Our Quant Trading Bots

Buy Long alert still in tact on LLY 0.00%↑

Buy Long alert still in tact on NVDA 0.00%↑

What to Watch Today

Federal Reserve governor Lisa Cook delivers introductory remarks at a Fed conference on nontraditional data, machine learning, and natural language processing in macroeconomics at 8:50 a.m. ET

The U.S. federal budget deficit is expected to narrow to $70 billion in October from $88 billion one year earlier. (2 p.m. ET)

Forecasts

🕵Discovering hidden treasures.🕵

1) Saucer Bottom Formation On PWR 0.00%↑.

PWR 0.00%↑ Price is starting to increase after forming a saucer bottom on the long-term uptrend line right around Earnings report (2nd Nov).

The pattern has been forming over the span of more than 1-month, to be precise around 37 days, making it significant.

Volume has significantly increased around the bottom, confirming support and heightened interest in the stock at these levels.

If support keeps on holding with high volume, then it would be confirming the trend continuation. And potential new leg higher may be expected up to the zone of the previous all-time high.

On 5th September Argus Research - Confirmed its grade on PWR 0.00%↑.

From: Buy

To: Buy

On 13th September Baird- Confirmed its grade on PWR 0.00%↑.

From: Outperform

To: Outperform

Price likely to converge upwards towards the 2-month average.

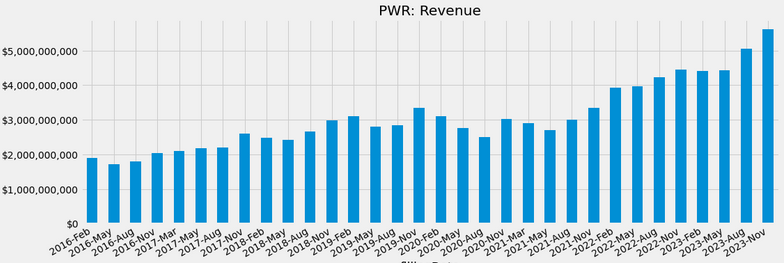

The company announced record third-quarter revenues of $5.6 billion, reflecting strong performance across its business segments.

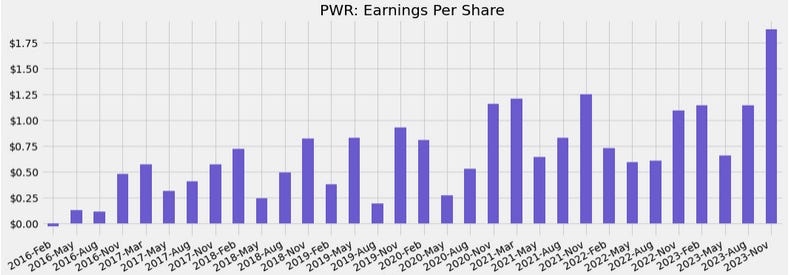

Net income attributable to common stock was $273 million or $1.83 per diluted share, and adjusted diluted earnings per share reached a record $2.24.

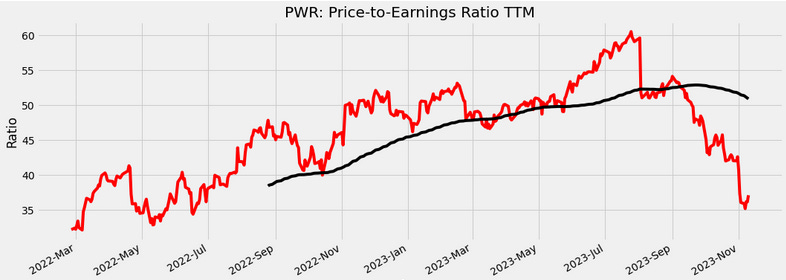

Recent Earnings make PWR 0.00%↑ look cheaper than before, with Price-to-Earnings ratio dropping to around 36.

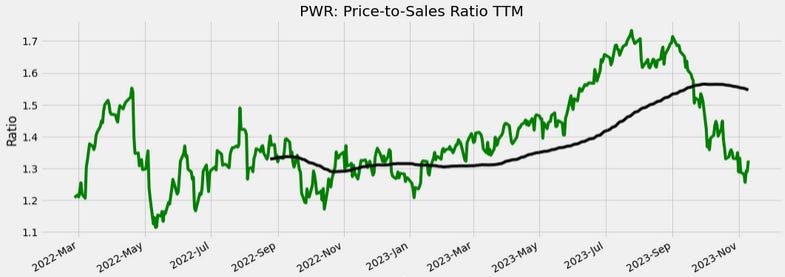

The “cheapness” argument is rather confirmed by the long-term Price-to-Sales ratio.

PWR 0.00%↑ Recent Earnings Transcript Summary (Future potential, implied by management vision):

Backlog and Financial Position:

Total backlog reached a record $30.1 billion at September 30, 2023, showing an increase of $2.9 billion compared to June 30.

The company reported free cash flow of $280 million for the third quarter and maintained a total liquidity of approximately $2 billion.

Guidance and Outlook:

Consolidated revenue expectations for the year have been raised to range between $20.1 billion and $20.4 billion.

Electric segment revenues for the year are now expected between $9.6 billion and $9.7 billion, with margins ranging between 10.4% and 10.6%.

Renewable segment full-year revenue expectations have been raised to range between $5.8 billion and $5.9 billion, with margins around 8%.

Underground segment revenue is now expected to range between $4.7 billion and $4.8 billion, with improved full-year margins ranging between 7.6% and 7.8%.

The company expects revenues for the year to be almost 20% higher than 2022 and has increased expectations for full-year adjusted EBITDA to range between $1.91 billion and $1.95 billion.

Acquisitions and Strategic Opportunities:

The company made a small acquisition reported through the Electric segment.

The strategic acquisition of Pennsylvania Transformer has closed, addressing a critical supply chain constraint for utility, renewable, and industrial customers.

Long-Term Outlook:

The growing backlog and favorable multiyear outlook give the company confidence in achieving the multiyear targets laid out in the April 2022 Investor Day.

The acquisition of Pennsylvania Transformer is seen as a strategic move, further cementing the company's ability to provide differentiating solutions in the North American energy transition.

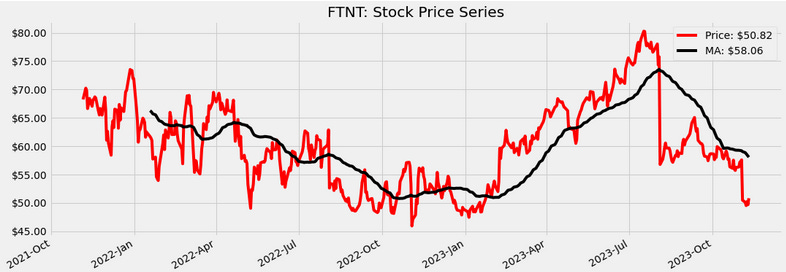

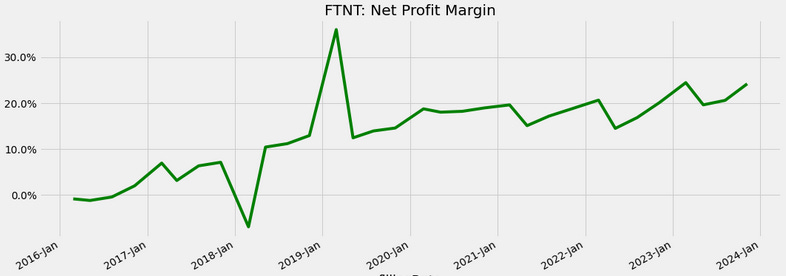

2) Double Bottom Formation On FTNT 0.00%↑.

FTNT 0.00%↑ Price has bounced back from deep and sharp decline on their recent earnings day (2nd Nov), forming a Double Bottom pattern.

Strong support hit on those recent low levels as well price is starting to gradually increase after forming this long-term Double Bottom.

Furthermore, a gap has opened after the earnings report. (Gaps are usually filled and closed)

The pattern has been forming over the span of more than 1-year, to be precise around 370 days, making it very significant.

Volume has significantly increased around the bottom levels, confirming support and hightened interest in the stock at these levels.

If support keeps on holding with high volume, then a potential new leg higher may be expected up to the zone of closing the gap.

FTNT 0.00%↑ has no recent (last 3 months) analyst grade changes or confirmations.

Price far away from 2-month average.

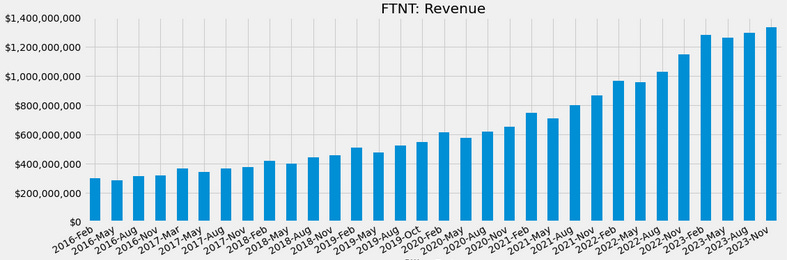

Total revenue grew 16% to $1.33 billion, with product revenue down 1% and service revenue up 28%. Service revenue accounted for 65% of total revenues.

Net Profit Margin is on a slight uptrend.

Very strong EPS growth in most recent quarter.

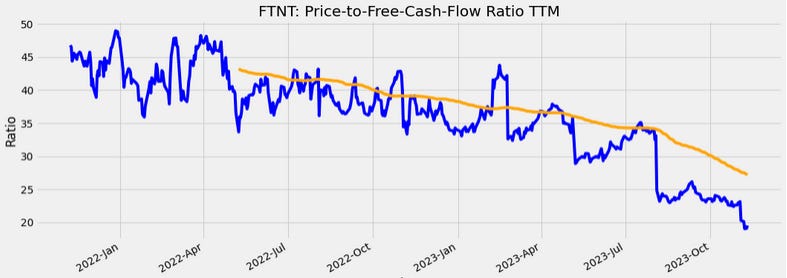

Recent Earnings make FTNT 0.00%↑ look even cheaper than before. However, is this a sign that the stock is maturing?

Operating margin exceeded guidance, and free cash flow was strong at $481 million, representing a margin of 36%.

FTNT 0.00%↑ Recent Earnings Transcript Summary (Future potential, implied by management vision):

Strategic Shift and Focus:

The company is confident in its integrated 400S driven platform strategy, shifting R&D and go-to-market investments towards the faster-growing SASE (Secure Access Service Edge) and SecOps (Security Operations) markets.

Market Share and Growth Projections:

SASE and SecOps currently account for 20% and 10%, respectively, of the business and are expected to grow in the mid- to high teens annually. Secure Networking, currently 70% of the business, is expected to experience lower growth for the near term.

Strategic Investments and Wins:

Tactical steps and investments include integrating single SASE features, expanding SecOps capabilities with AI technology, and co-development agreements with large enterprise customers.

Key SASE wins include upselling SASE solutions to existing customers and strategic transitions to SaaS and cloud-based applications.

Outlook and Guidance:

The company acknowledges increased deal scrutiny and longer sales cycles, constraining near-term results. Fourth-quarter guidance considers these factors.

Billings for Q4 are expected to decline by 5%, with revenue growth of 10%. Full-year outlook includes a 10% growth in billings and 20% growth in revenue.

Expectations for 2024 include a focus on improving profitability, gradual increase in billings growth, and approaching double-digit growth by the second half of 2024.

Long-Term Confidence:

The company expresses confidence in its solutions and the ability to adapt its strategy to market shifts, aiming to return to balanced growth and profitability in the long term.

Disclaimer: Please note that the information provided in this article is for general informational purposes only and does not constitute financial, legal, or professional advice. The information provided should not be relied upon as a substitute for financial, legal, or professional advice. Before making any decision, it is important to consider all relevant information and consult with a professional who can provide personalized advice based on your specific circumstances. The author and publisher of this article cannot be held liable for any actions taken based on the information provided. This is not a recommendation to buy or sell any specific securities or financial instruments.