Following the Ebbs & Flows

Hello and welcome to another issue of 🕵 The Seeker 🕵

With every investment we becoming richer or wiser, never both. - Mark Yusko

1) Big moves drawing attention from the last three trading days

Compared to the S&P500 all industry sectors of the XLV are showing relative performance. One stock in a nice buy range could be Gilead Sciences. GILD 0.00%↑ has a slew of exciting drug treatments and a stock price currently resting at the bottom of what could be a bullish consolidation range. We also like the easily definable stop-loss placement for trading rather than investing.

Last week we saw buyers return to PGR 0.00%↑. As one of the high sharpe darlings of 2022, pulling in over 25% returns while many fintechs got slaughtered, it’s worth following along when Progressive outperforms (and might not be a great sign for the market overall).

Last week we saw interest in space related stocks apparently diversify away from Virgin Galactic. Somewhat luckily, yours truly sold half his options position after returning the full initial investment. Therefore I wasn’t heartbroken when SPCE 0.00%↑ announced new stock issuance. However, with their future financing secured, it seemed to remove a heavy blanket from several of the better quality names in the sector, like RDW 0.00%↑ (shown below), BKSY 0.00%↑ or ASTS 0.00%↑.

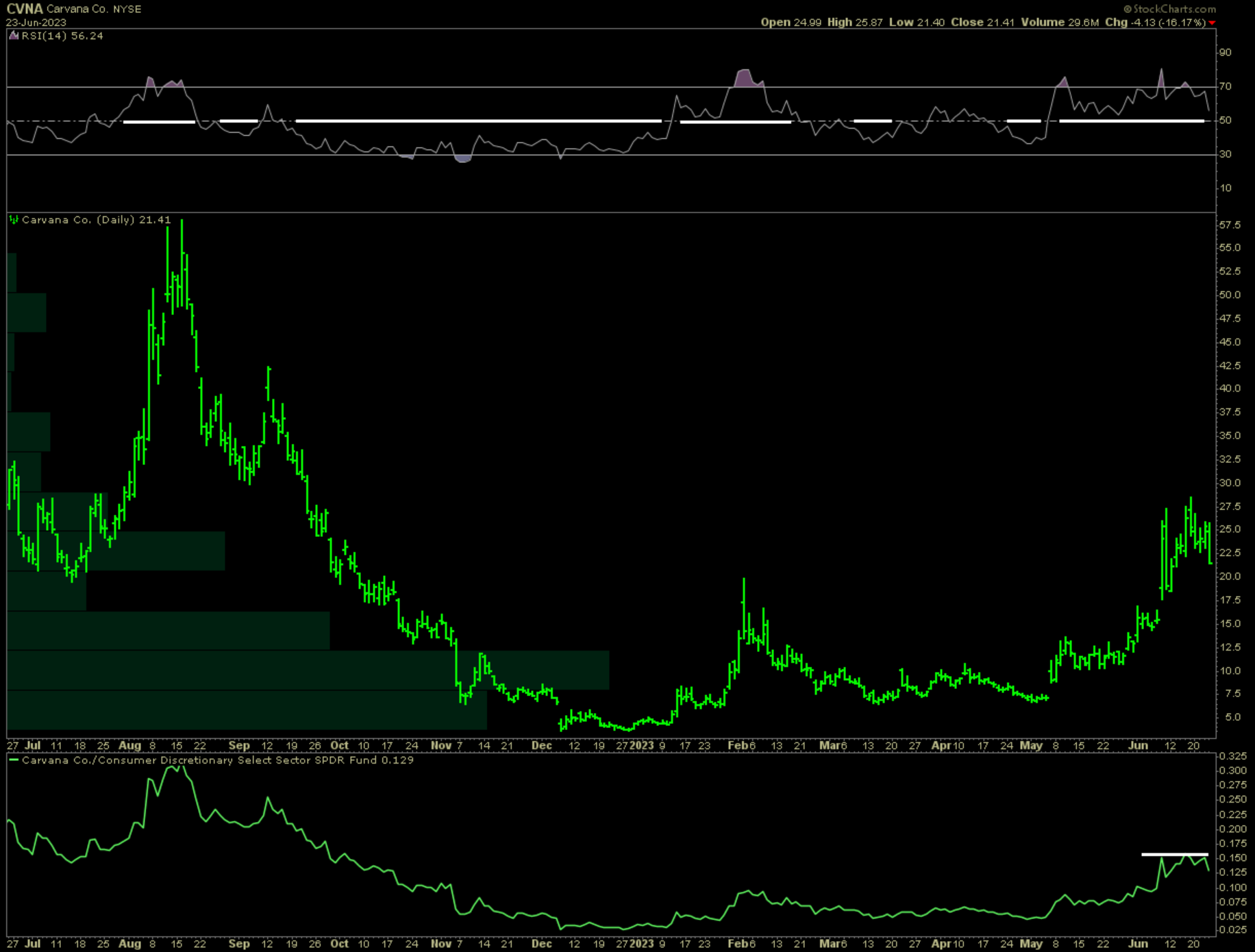

Friday was not kind to CVNA 0.00%↑. Zooming out, the chart is a hot mess. Viewed thru bear goggles, the gap to $17 on the downside looks air pocket lite and Carvana’s price should be expected to be resolved there shortly, unless participants who have driven this rally are able to immediately defend the ongoing squeeze.

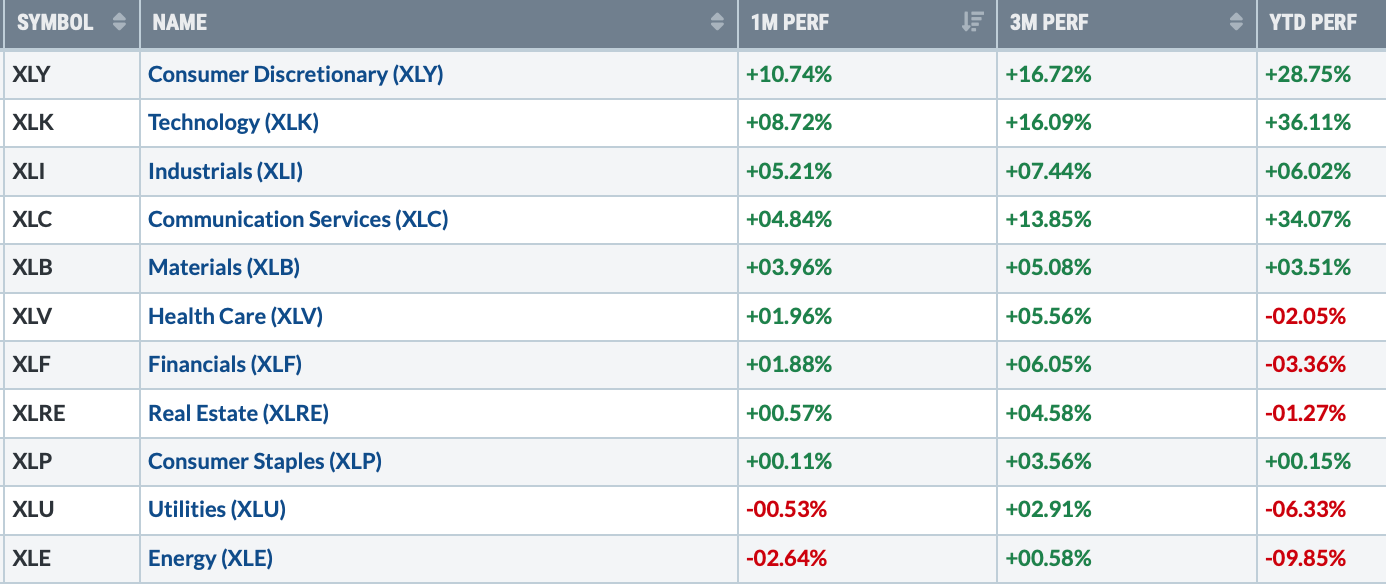

2) Sector Performance

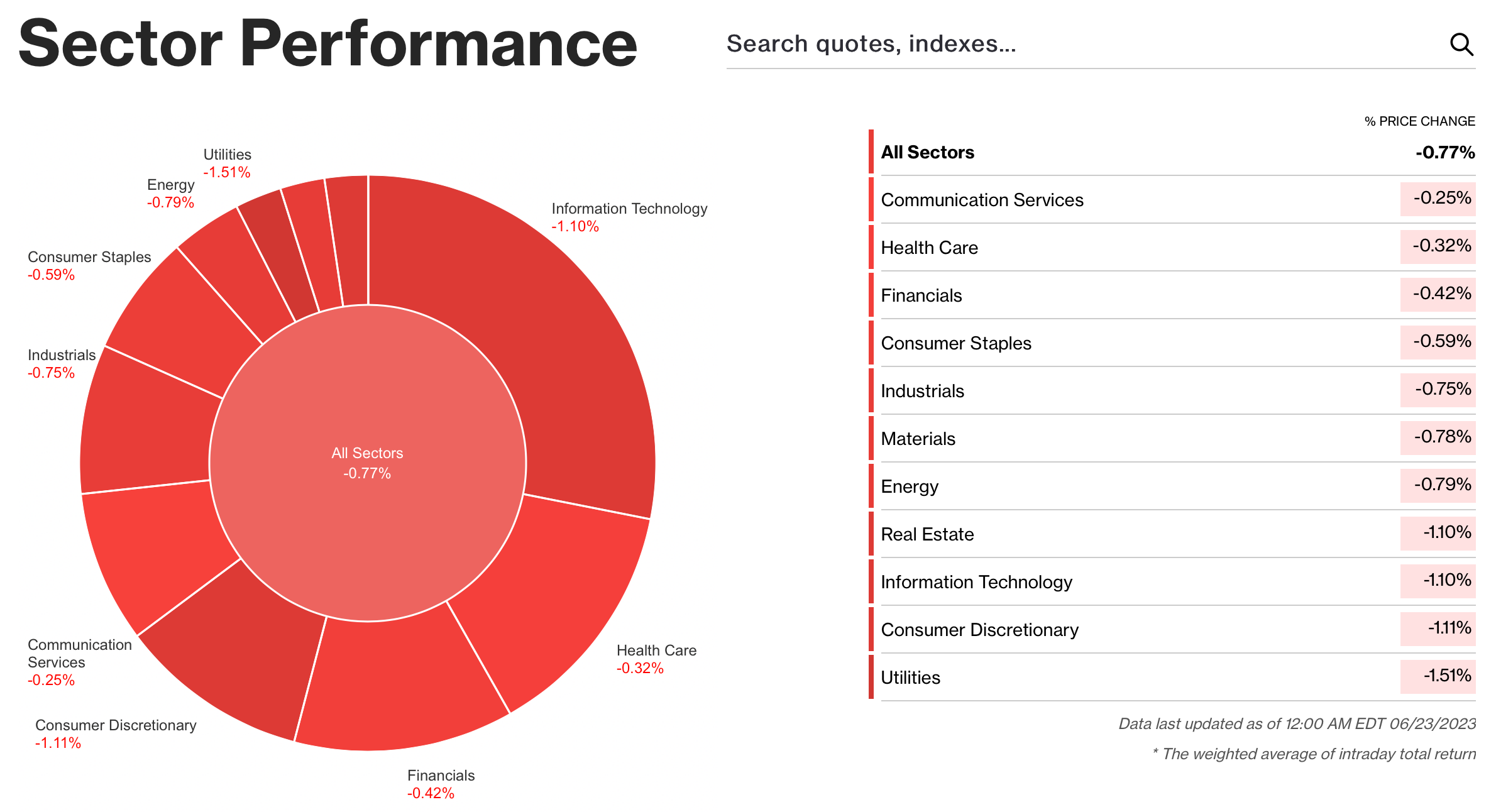

For the second straight week we saw clearly negative Friday returns. This Friday all sectors were in the red. Excluding Utilities (which abhor rising interest rates), it was growth sectors like Consumer Discretionary and Tech leading to the downside.

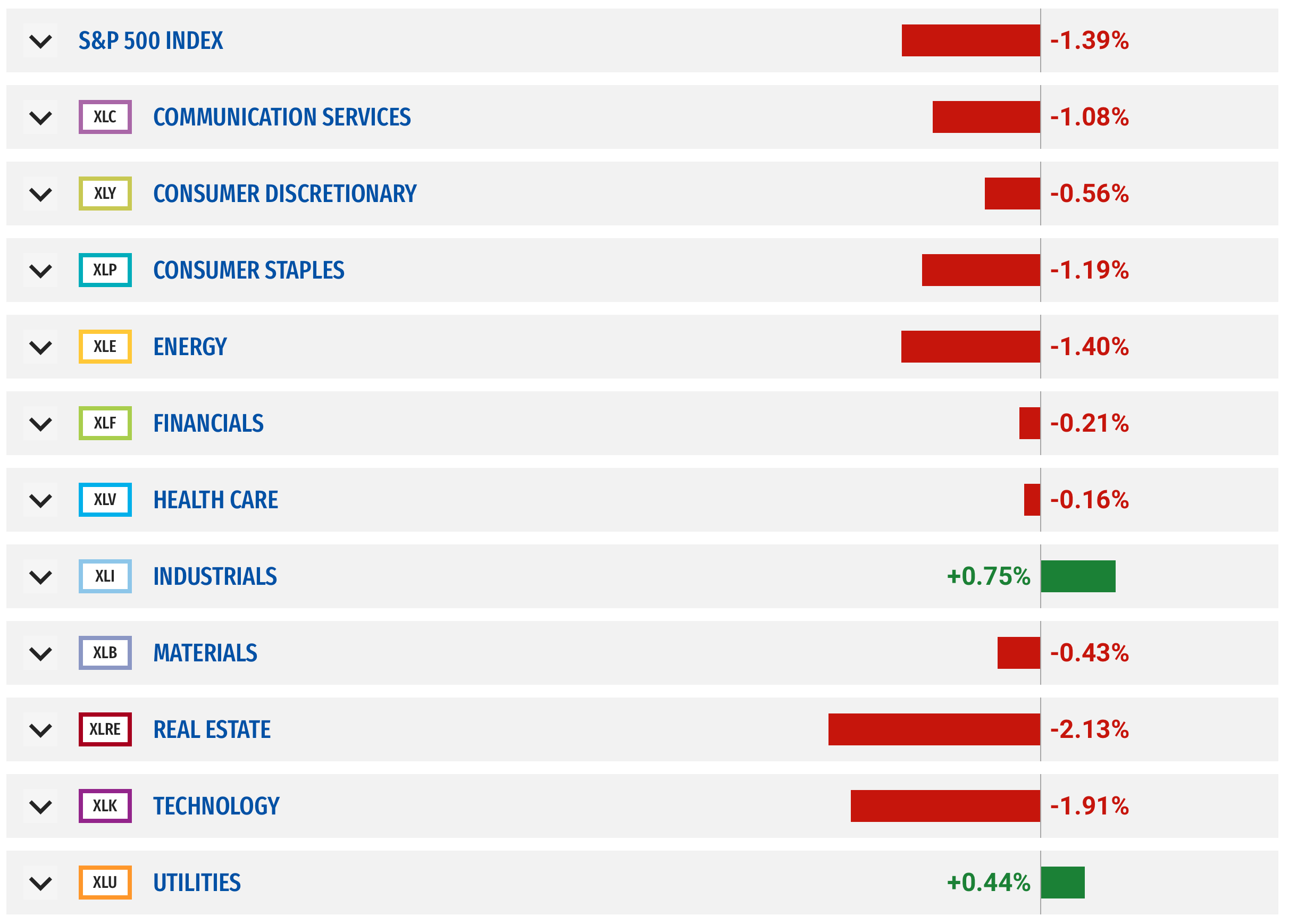

Here is the view for the full week, painting a somewhat different picture with investors in industrials still smiling, even though the broader SPY 0.00%↑ was down almost 1.4%.

Doing a half yearly check, it’s clear there is some profit-taking now in the ytd best performing sectors, and less from laggards like Health Care and Financials, in anticipation of investor’s summer holidays.

Semis

As could be expected, SMH 0.00%↑ is showing that it needs some time before being able to break through it’s previous all-time. I’ll be bold and say that this is THE chart to watch for diagnosing this current version of U.S. markets. There is positivity in the rising moving averages, and if dip-buyers come in to support these levels, a new economic cycle could be upon us. However, if the new bear market line doesn’t hold, more rotation away from semiconductors is to be expected.

3) Earnings reports from this following week:

(Note: normal earnings updates will return once earnings season is underway)

With earnings a couple of weeks away, it may be too early to expect Wall Street to be already gearing up, but we’re still looking for signs of optimism in banking. Bring up the chart of KRE 0.00%↑. Regional banks had an outside week, giving up all nearly all the returns of the previous month. So far this is not instilling confidence that renewed optimism is sustainable in this economic sector.

As we’ve covered at QuantFactory previously, we know of the outperformance of homebuilders and autos which are still ongoing. One surprising sector where if I’d have to guess earnings surprises are being expected, is Broadline Retails where we se money being rotated.

4) The week ahead

The Calendar

A number of high-profile companies are scheduled to report earnings next week. Bank stress tests and inflation data will be other highlights.

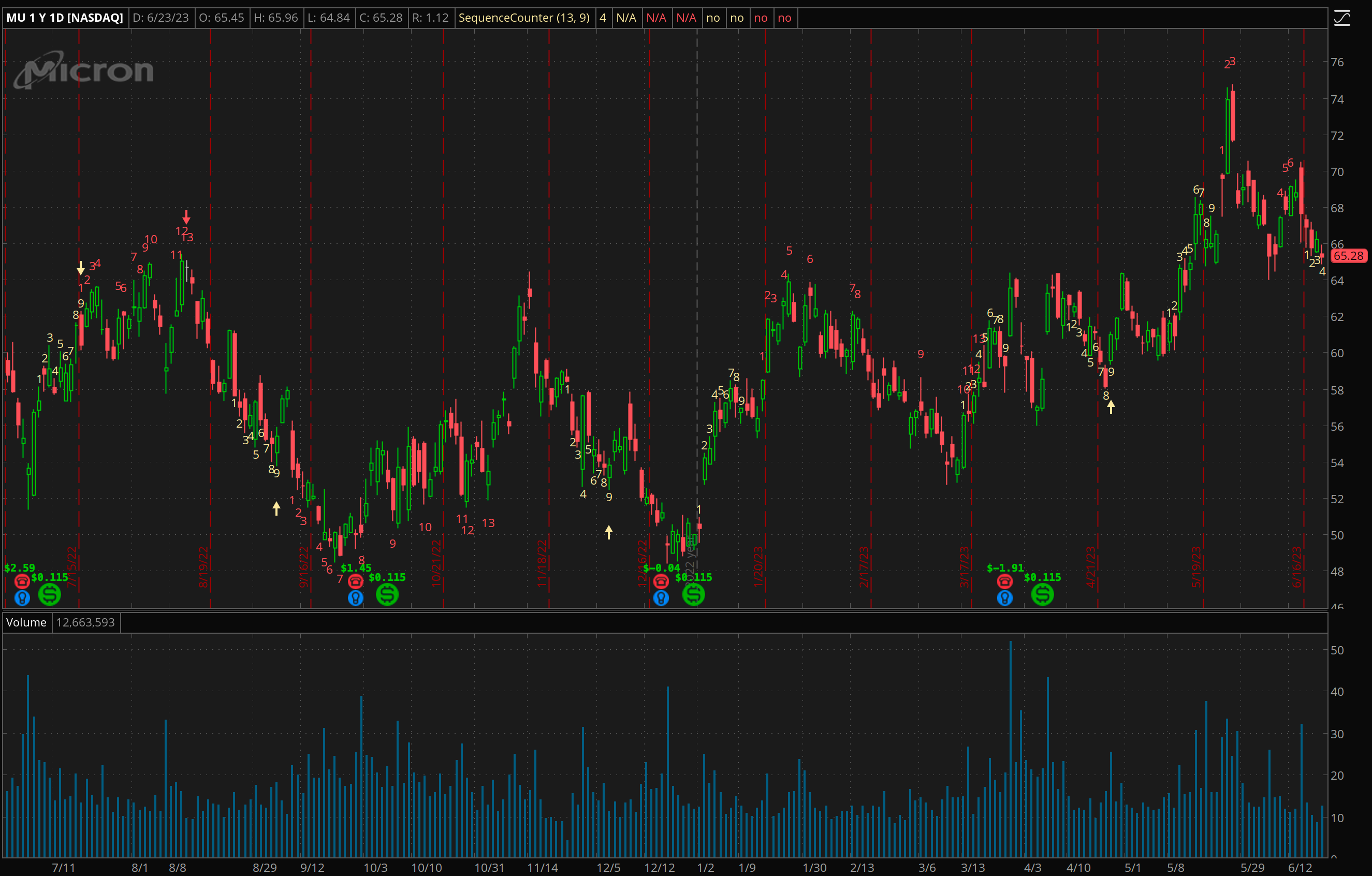

Carnival reports on Monday, followed by Walgreens Boots Alliance on Tuesday. On Wednesday, Micron Technologies and General Mills release results, then Nike, McCormick, and Paychex go on Thursday. Constellation Brands closes the week on Friday.

Meanwhile, on Wednesday, the Federal Reserve will reveal the results of its annual stress test of the U.S.'s largest banks, including determining how much banks can return to shareholders via stock buybacks and dividends.

Economic data out next week will include the Census Bureau's durable goods report for May and new-home sales data for May, both on Tuesday.

The Bureau of Economic Analysis will also report personal income and expenditures data for May on Friday. Economists are expecting to see a 0.4% rise in income and a 0.3% increase in spending last month. The Federal Reserve’s preferred inflation measure, the core personal-consumption expenditures price index, is forecast to be up 4.7% from a year earlier, matching April.

--Nicholas Jasinski

With Micron reporting this week it’s clear that Wednesday evening entertainment fully secured. If fundamentals don’t improve for MU 0.00%↑, there is full possibility it skips back to it’s 2022 lower trading range that the 2021 bull market range it’s currently been rewarded with. We’ll be watching!

(Note: the poor price strength of the last week, showing investors reducing risk ahead of earnings)

5) Macro conditions

Weekly risk signals are based on intermediate and long-term market trends, as well as the flow of money into or away from asset classes. Not included are potential fundamental or gamma implied volatility tail risks.

Note: top traders themselves have a hit rate approaching the 50% lower bound. Controlling risk on losing positions and letting winners prosper is for many the difference in creating a successful track record over time.

Saw flows leaving growth and tech, with heavy selling in small-caps IWM 0.00%↑. Otherwise there was some drama in currencies with the Dollar gaining wind, lot’s of selling in the Euro and the Yen starting to look far extending in it’s sell-off.

We’d also be remiss not to observe Bitcoin which is decoupling with Gold.

6) Opportunities/Movements Internationally

This week there was a very interesting development on the future of electrolysis for hydrogen and investments into this technology.

June 23 (Reuters) - Thyssenkrupp (TKAG.DE) and Industrie De Nora (DNR.MI)pushed ahead with the planned initial public offering (IPO) of their hydrogen joint venture Thyssenkrupp Nucera on Friday, setting the price range at the lower end of expectations.

The IPO will be the first in Germany since February, when shares in web hosting company IONOS (IOSn.DE) debuted in Frankfurt, as stock market volatility and an uncertain economic outlook have put other company listings on the back-burner.

Being priced at the lower end of it’s range, this placed a firm price cap on it’s smaller competitors which have been able to enjoy premium valuations due to a lack of other similar investment opportunities.

Looking at the weekly performance of NEL ASA who has similar technology, we see just how this repricing is unfolding in the public markets.

😎 Cheers! 😎

Disclaimer: Please note that the information provided in this article is for general informational purposes only and does not constitute financial, legal, or professional advice. The information provided should not be relied upon as a substitute for financial, legal, or professional advice. Before making any decision, it is important to consider all relevant information and consult with a professional who can provide personalized advice based on your specific circumstances. The author and publisher of this article cannot be held liable for any actions taken based on the information provided. This is not a recommendation to buy or sell any specific securities or financial instruments.