Easy Peasy

Hello and welcome to another issue of 🕵 The Seeker 🕵

"If something is important enough, even if the odds are against you, you should still do it." - Elon Musk

1) Big moves drawing attention from the last three trading days.

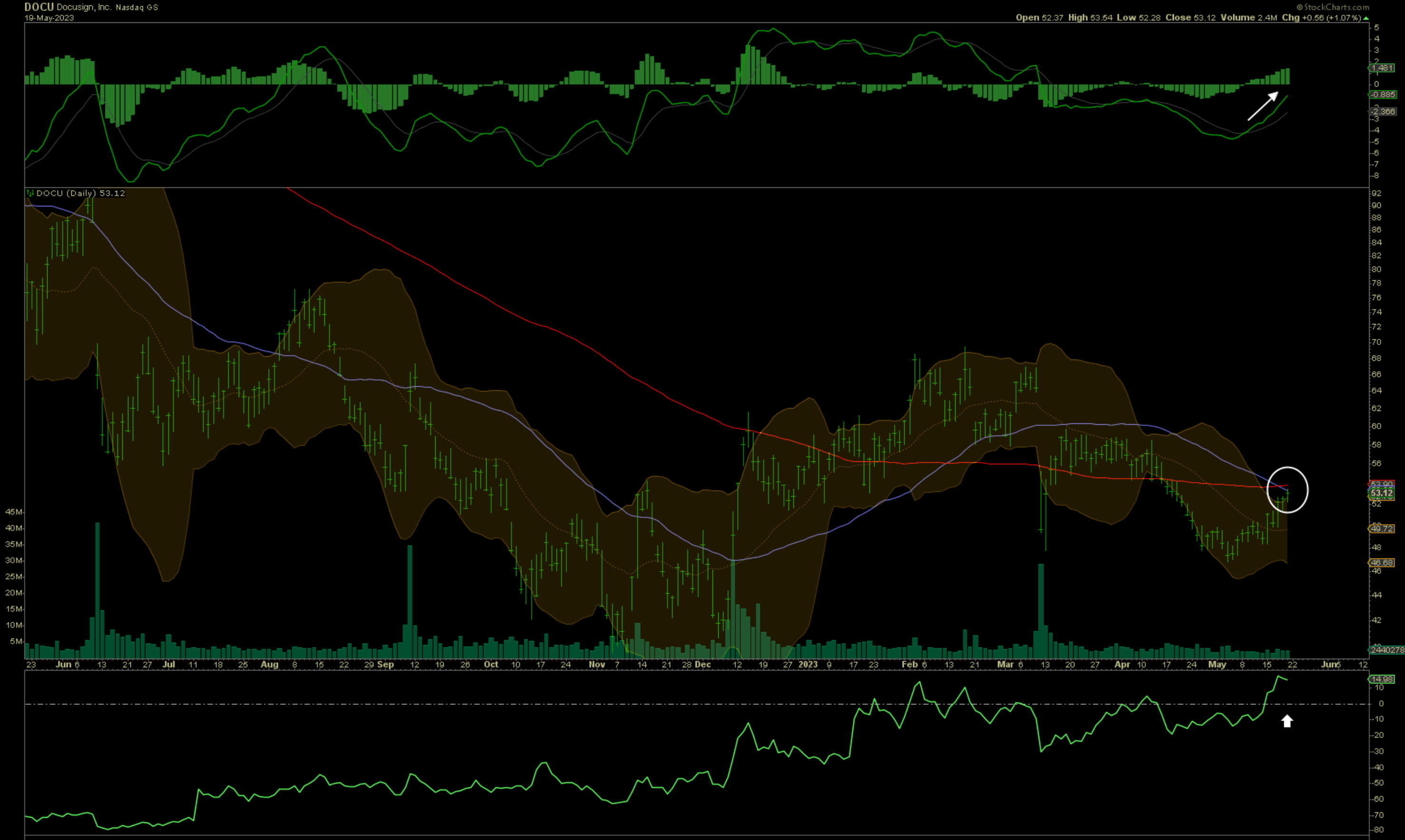

DocuSign, which reports earnings on June 8th, has been experiencing a positive streak recently. Its long-term moving average is starting to rise, and the stock is making an attempt to surpass this point once again. This time with a significant upward momentum trajectory. When this author asked Bard how many times DOCU 0.00%↑ mentioned "AI" in their previous earnings call, the answer was 23 times. Currently, DocuSign's implied volatility is greater than 70 (about smack in the middle of normal pre-earnings IV).

Next up we would be remiss not to mention NVDA 0.00%↑ and admire this chart, no markups / no noise. The clear leader in advanced chips, Nvidia reports earnings on Wednesday. With semiconductor sales down 20% YoY in one of the latest industry reports, we think the stock’s unrelenting climb seems overdone, but by judging other household names (re: $TSLA) in comparison, the most pain almost certainly exist to the short side.

The prior week, during Friday’s session, trading in SRPT 0.00%↑ was halted. Sarepta Therapeutics is using gene-editing to target rare diseases with it’s pipeline, and last week an FDA panel gave a positive review of the company’s submission. As they seek approval, as one of the first using this biotechnology, there is a lot of interest surrounding this stock. Make notice of the especially heavy volume recently.

With so much liquidity, markets are perceived to be correctly priced at all times, but are they? A small number of ETF providers have products for tracking the results of women leaders and CEOs (e.g., FDWM 0.00%↑ & WCEO 0.00%↑ ). One hypothesis is that there could be significant opportunities in such an investment style, as opposed to betting on more promotional accolades from the same hypesters. One company hoping to address some of the unmet medical needs of women is Dare Biosciences. DARE 0.00%↑ is currently awaiting the Phase 2b readout for Sildenafil, and we observe the formation of a possible tradable bottom for the stock.

2) Sector Performance

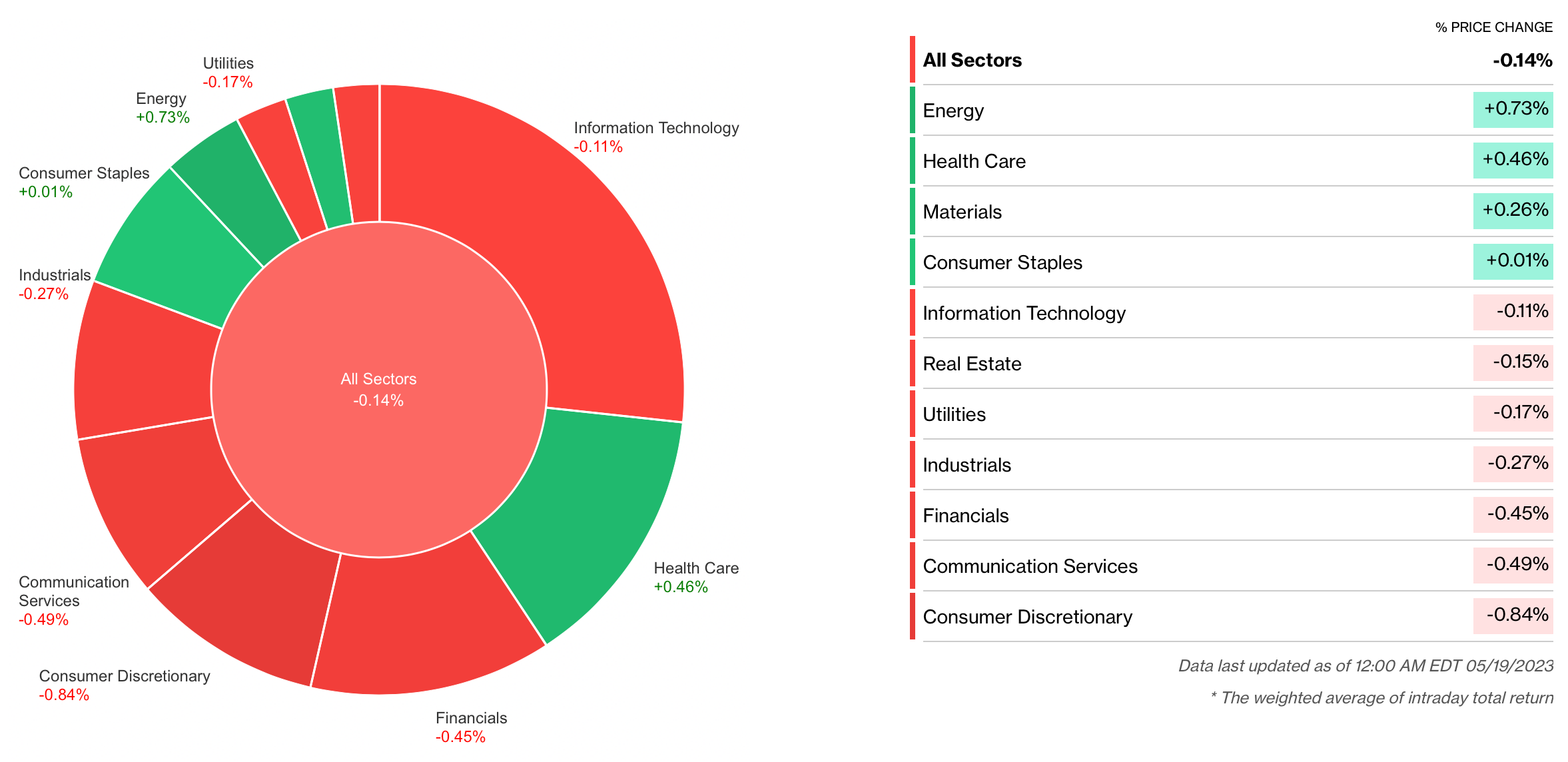

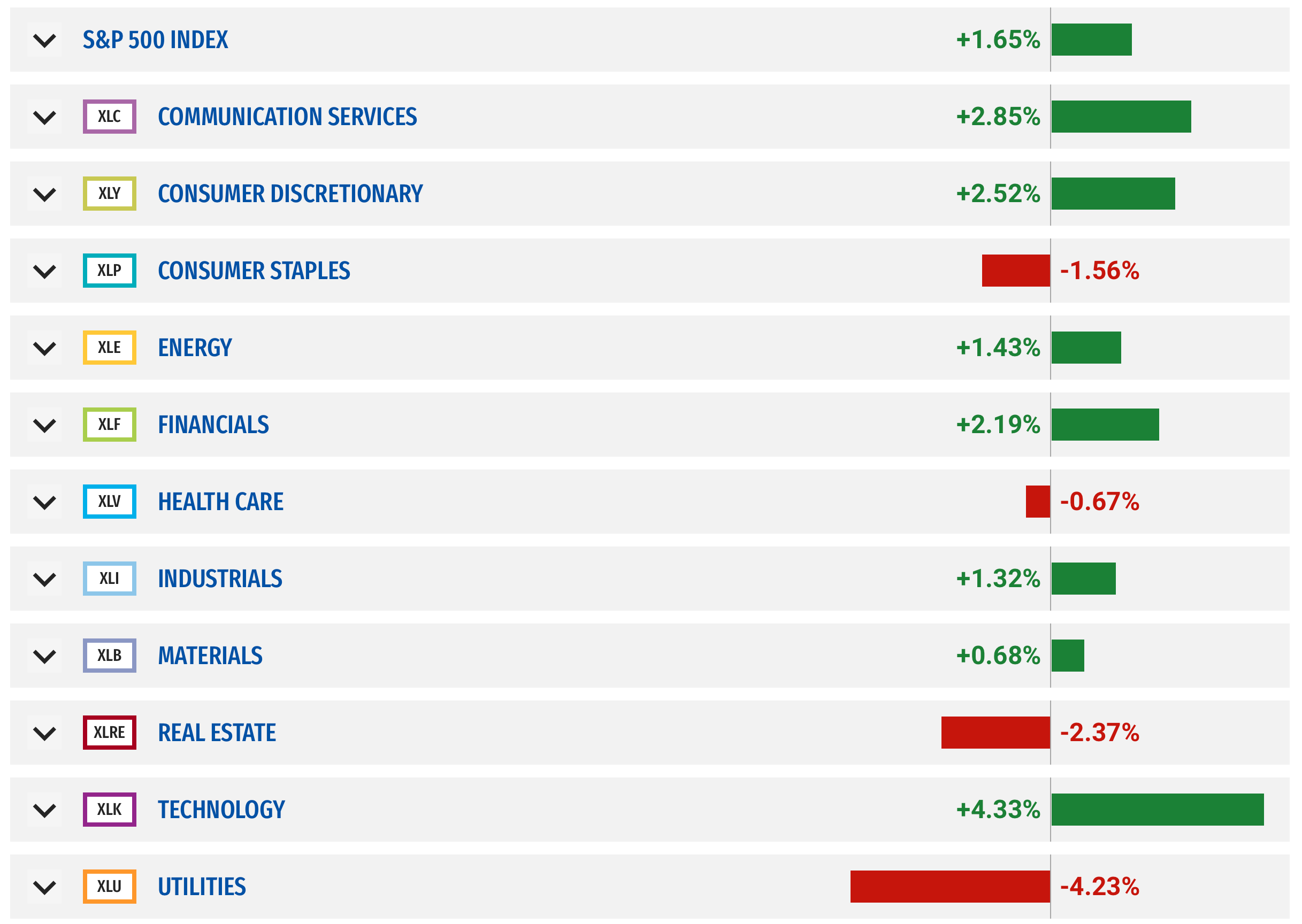

Friday saw expiring monthly options creating a bit of a mixed bag, with some beaten-down sectors leading the charge, including Energy, Health Care, and Materials. Communication Services took a pause, while Consumer Discretionary continued to show weakness.

On the week Technology, Communication Services, Consumer Discretionary, Staples, Financials and Energy advanced.

The Trend

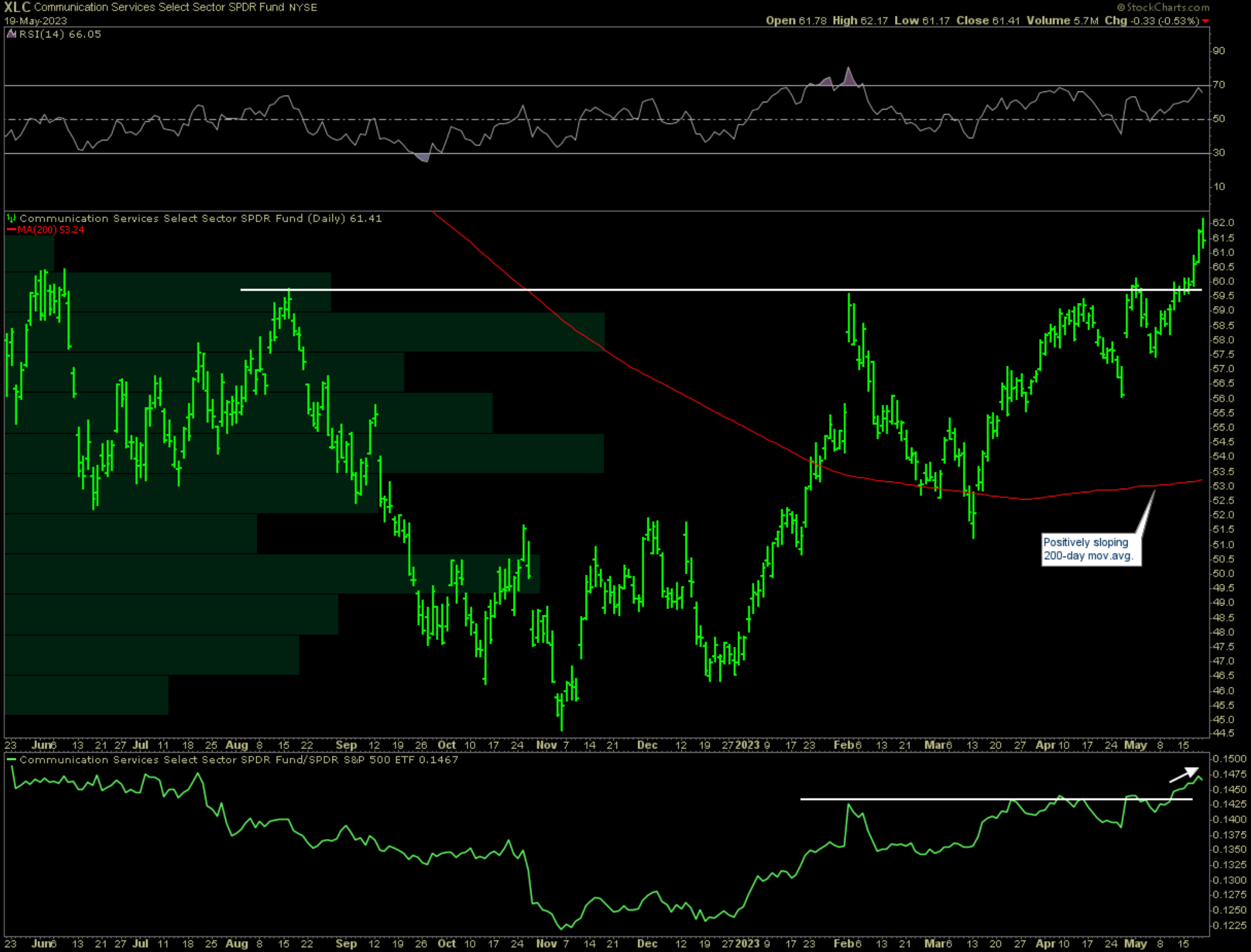

The strength in Communication Services deserves our attention as a clear trend appears to be forming. We are currently awaiting confirmation from the S&P 500, with a break above the recent February resistance. However XLC 0.00%↑ , led by the internet sub-sector and companies like GOOG 0.00%↑ , META 0.00%↑ , and NFLX 0.00%↑ which have already surpassed their May and August highs to confirm their leadership. This is particularly evident when observing the relative strength chart below.

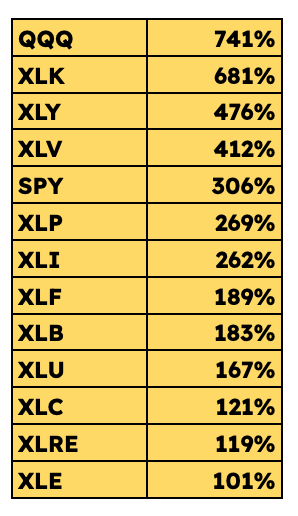

It’s observed that the current top performance groups are starting to eerily resemble the macro-trends from the last 10-yrs. These are the sector results from the last 10-years of bull market returns:

(NOTE: XLC and XLRE have not been around over this entire timeframe. Therefore the list is supplemented with QQQ to give a representation of tech’s outperformance)

It was another strong week for the semiconductor industry, with SMH gaining over 8%. Of particular note was Micron (MU 0.00%↑ ) , a company whose fundamentals have been less than impressive. However, buyers are looking past its current challenges, and the stock is finally breaking out of its bear market phase by reentering its bull market trading zone of 2021.

Sector Contrarian

Options expirations can often squeeze the pressure from off-side positioning, with counter-trend reversals frequent. This week, we witnessed a similar rebound in the Energy sector.

Worth noting is possible formation of a bottom and higher low compared to March in XLE 0.00%↑ , while the rate of change of the long-term trend is defying negative territory. Other charts that bear resemblance include CVX 0.00%↑ , etc.

The argument for buying centers around Buffett's continued bullishness and OXY 0.00%↑ accumulation, along with the potential for a positive rate environment reversing the fortunes of underperforming value sectors (re: 10-year returns above). Due note however Buffett’s varying investor timeframe, and differing liquidity requirements for entering trades compared to mom&papp.

…Bonus Sector Update

Since the October lows home builders have rallied significantly and now appear to be at a critical juncture with momentum easing, and seasonality likely to give less of a tailwind. ITB 0.00%↑ corrected somewhat on Friday’s OPEX. It wouldn’t be uncommon for the price to consolidate here, probably re-test making a new high, but significant further upside could be capped.

3) Earnings reports from the previous week:

Weekly results from some names of significant interest.

4) The week ahead

From Barrons:

The Calendar

Inflation data, Federal Reserve meeting minutes, and first-quarter earnings reports from retailers and chip makers are the highlights on next week's calendar.

Zoom Video Communicationsreleases results on Monday, followed by AutoZone, Intuit, and Lowe’s on Tuesday. Nvidia, Analog Devices and Snowflake report on Wednesday.

Thursday will be busy: Best Buy,Costco Wholesale, Dollar Tree, Marvell Technology, Ulta Beauty, and Workday all publish results.

JPMorgan Chase and Ford Motorhost investor days on Monday, followed by PG&E and Thermo Fisher Scientific on Tuesday and Zoetis on Thursday.

On Wednesday, the Federal Open Market Committee releases the minutes from its early-May monetary-policy meeting. Those will be closely parsed for officials' discussion of when to pause interest-rate increases.

On Friday, the U.S. Bureau of Economic Analysis will report personal income and expenditures for April—both are expected to have risen from March. The release will include the Fed's preferred inflation measure: The core personal-consumption expenditures price index. That's forecast to slow from the prior month, to 4.4% year over year.

Other data out next week includes S&P Global's manufacturing and services purchasing managers’ indexes for May on Tuesday. Both measures of economic activity are expected to slip from April. The Census Bureau will also release the durable goods report for April on Friday.

NOTE: the direction of markets the week following options expiration has quite often recently been further trend-setting for the near term. It’ll be important to watch how markets unfold over the course of the full week.

5) Macro conditions

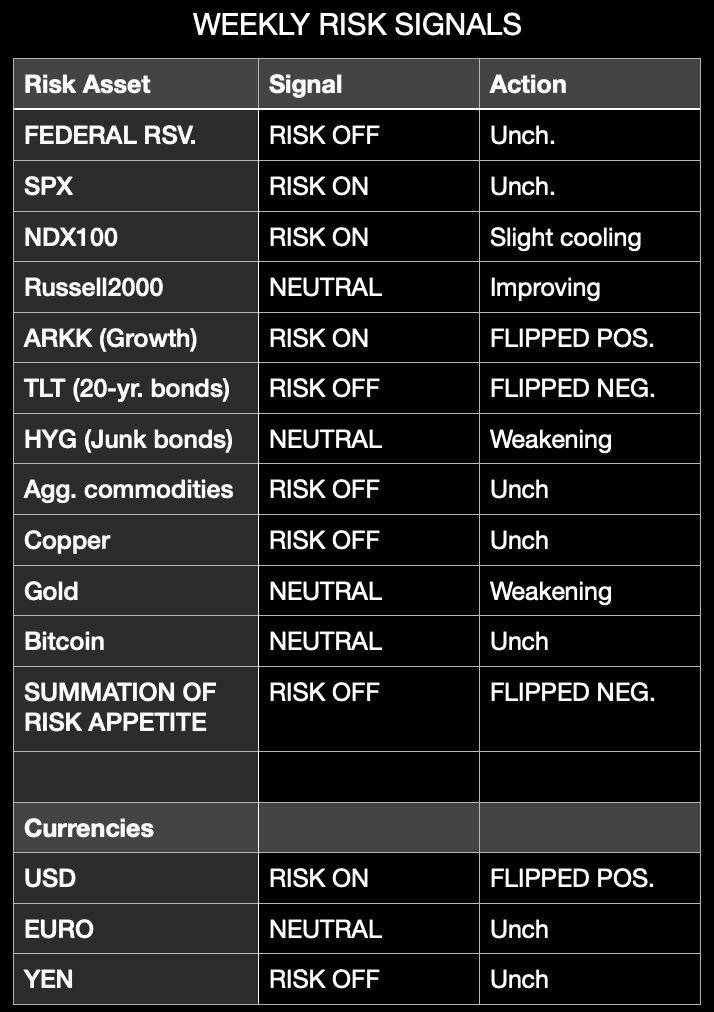

Weekly risk signals are based on intermediate and long-term trend in markets, as well as money flows into or away from asset classes. Not included are potential fundamental or gamma implied volatility tail risks.

Note: top traders themselves have a hit rate approaching the 50% lower bound. Controlling risk on losing positions and letting winners prosper is for many the difference in creating a successful track record over time.

During this week, several of our signals changed, leading to a reduction in 'Risk Off' stance for the summation score. This adjustment was prompted by the changing of narrow margins in the current market environment, and primarily the rise in bond yields.

Given the increased correlation between small-cap stocks and bonds, it is worth assessing the status of $RPAR (Risk Parity), which refers to an investment portfolio comprising both stocks and bonds.

$RPAR has been trading above its long-term moving average for a significant part of the year, but it is now approaching a critical juncture. The strategy has been consolidating without a substantial further move. Weakness is evident in momentum indicators such as MACD and Stochastics. Could this indicate a retest of the lows and potentially signal weakness in other areas of the market?

6) Opportunities Internationally

Japan… Japan… Japan

Equity strategists are foaming at the mouth to move their clients here. Buffet is investing in the future of the island nation. Even tiny Proximar Seafoods is going here to feed the nation with Atlantic salmon hatched at the foot of Mount Fuji. But will a nimble Ichiro Suzuki be able to fill the shoes of the iconic Ken Griffey Jr? Don’t get all crazy…Oh wait!

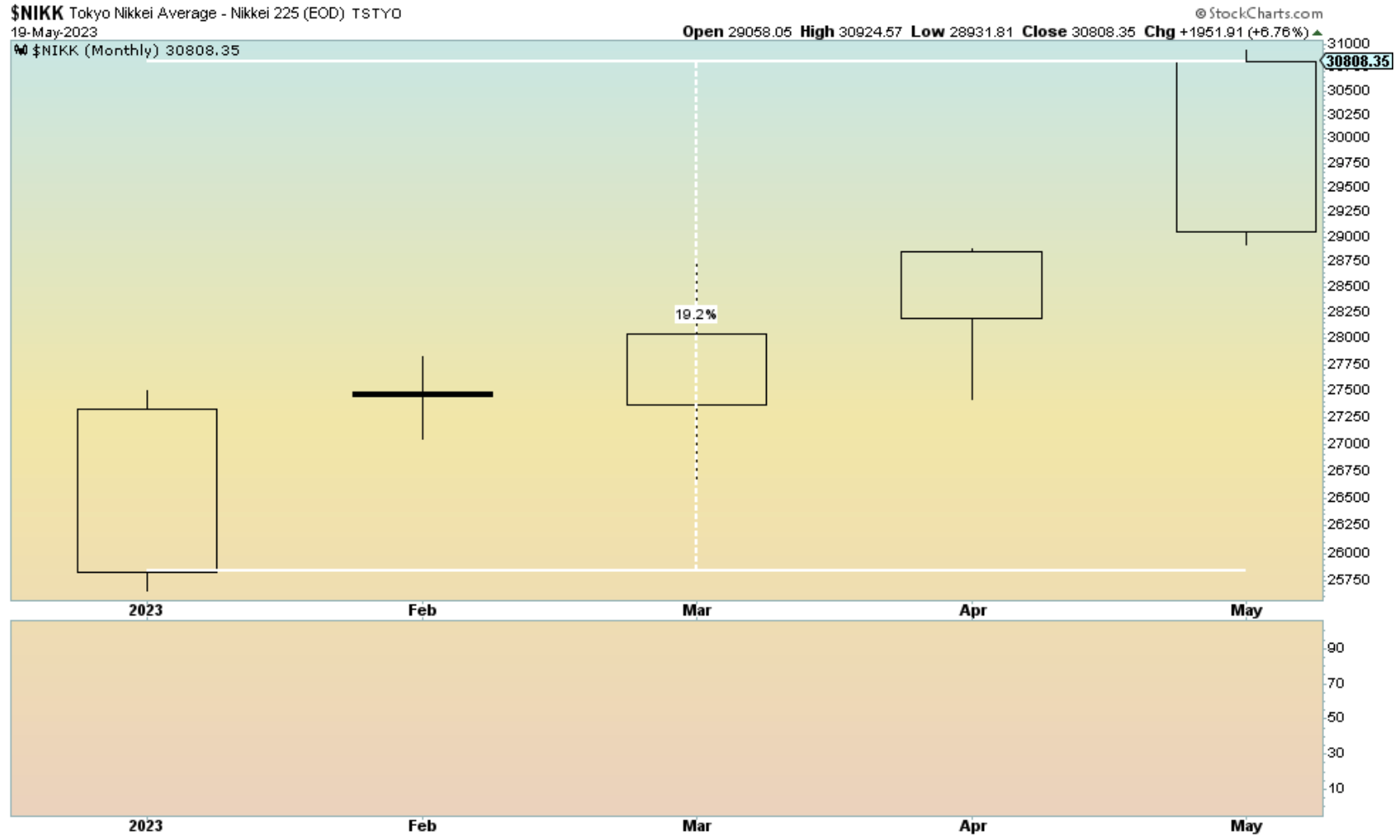

Here are the monthly results from the Nikkei 225, returning over 19% this year, far exceeding the results of the S&P.

Zooming out to the big picture, Japan’s wrestle hold on our lives reached a crescendo top with the GameBoy. Compounded by China’s entry into the WTO and rise as the world’s factory, an end of the modern bear market has been over 30 years in the making.

With political winds changing, perhaps Japan’s battery expertise or shear determination will force continuation of 2023’s strong start and propel Japan to re-assert global leadership.

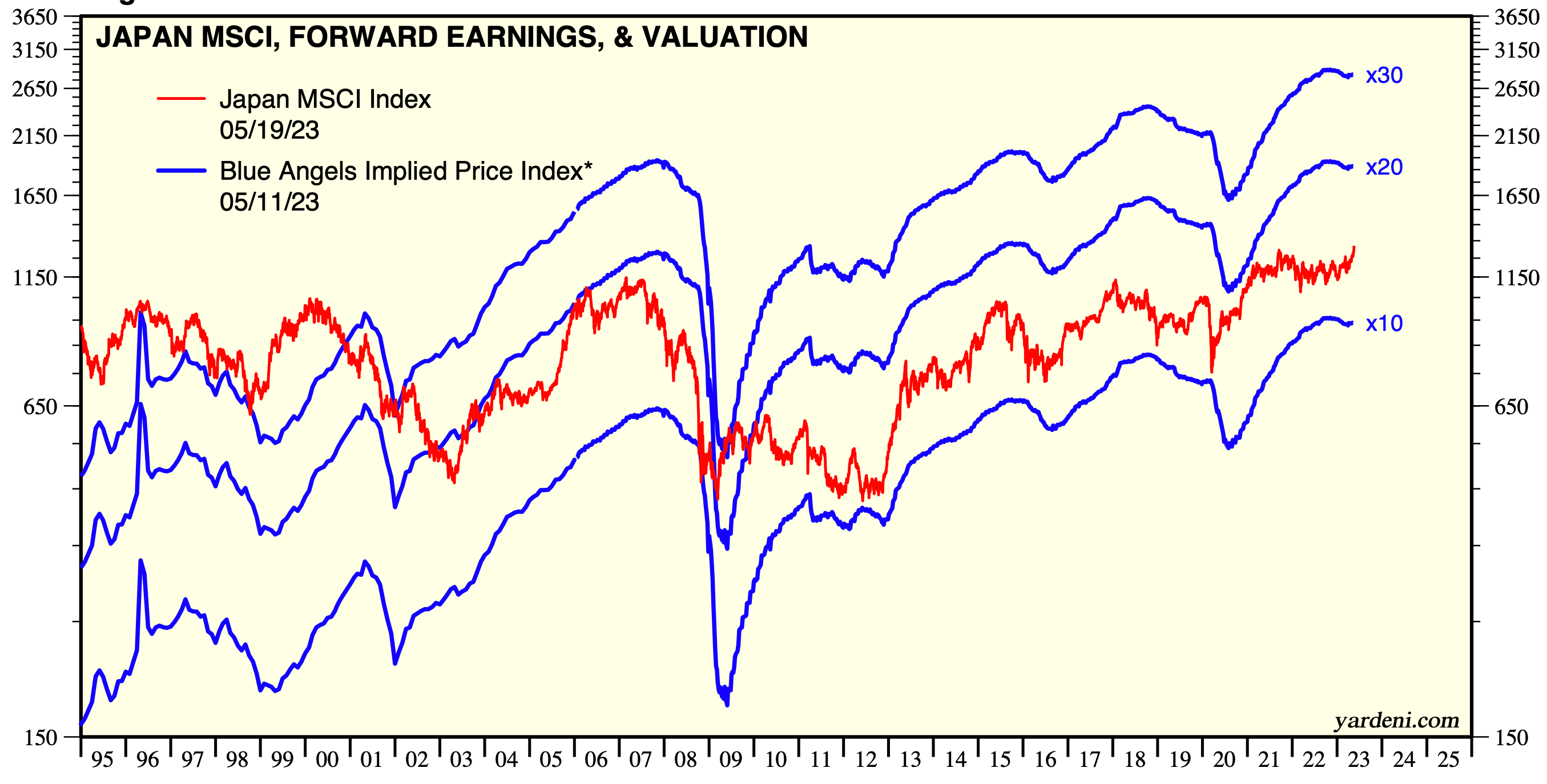

From Yardeni Research, the forward valuation of the Japan MSCI index remains compelling.

From Cnbc and the filing of Berkshire Hathaway, inc. these are the companies Buffett’s accumulating, signalizing non-other than a bet on Japan’s macro-economic tailwinds.

Itochu Corp.

Marubeni Corp.

Mitsubishi Corp.

Mitsui

Sumitomo Corp.

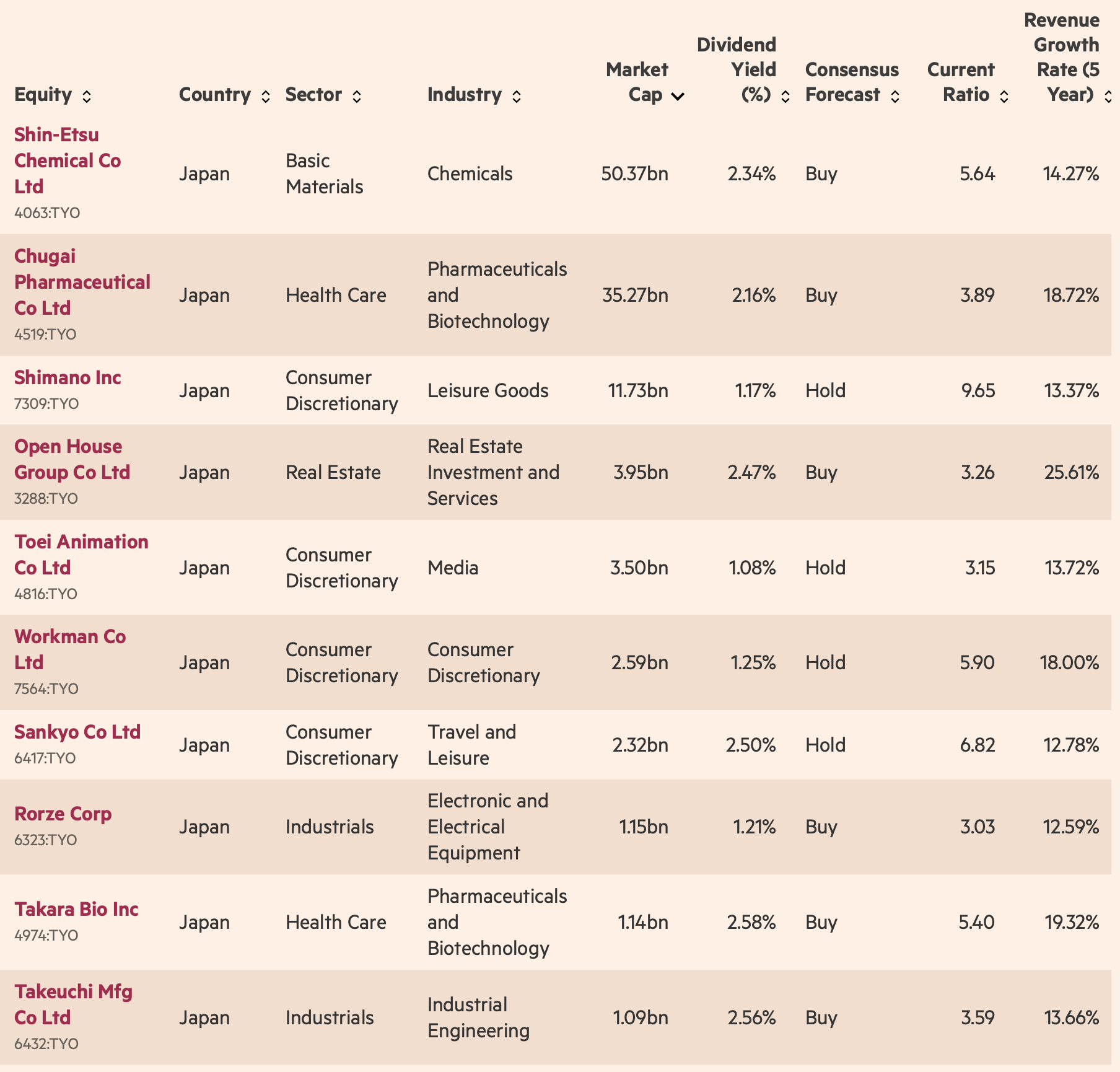

One can also run there own fundamental research. This screen using tools from the Financial Times looked at companies using value factors, including dividend, current Ratio, profit margin as well as revenue growth. (Sorted by market cap)

😎 Cheers! 😎

Disclaimer: Please note that the information provided in this article is for general informational purposes only and does not constitute financial, legal, or professional advice. The information provided should not be relied upon as a substitute for financial, legal, or professional advice. Before making any decision, it is important to consider all relevant information and consult with a professional who can provide personalized advice based on your specific circumstances. The author and publisher of this article cannot be held liable for any actions taken based on the information provided. This is not a recommendation to buy or sell any specific securities or financial instruments.