Bulls on Parade

Hello and welcome to another issue of 🕵 The Seeker 🕵

"Summertime is the perfect opportunity to review your investment strategy, adjust your sails, and navigate the stock market's waves." - Ray Dalio

1) Big moves and/or interesting developments from the last three trading days.

This week Virgin Galactic Holdings, the first public traded space flight company, announced it would commence with monthly trips at the end of June. On Friday it’s stock took off, but SPCE 0.00%↑ was quickly reeled in by eager short sellers. After cooling off midday it’s now testing it’s long-term moving average from above, with interesting potential should it continue to be a summer market for stock picking.

Last week on the brink of quad witching, we mentioned the possibility for new paradigms to shift. One of these shifts could be showing itself through a bullish trend being formed at Teleflex. Wall Street has been accumulating TFX 0.00%↑ for some time and maybe now is the time for price to leg higher.

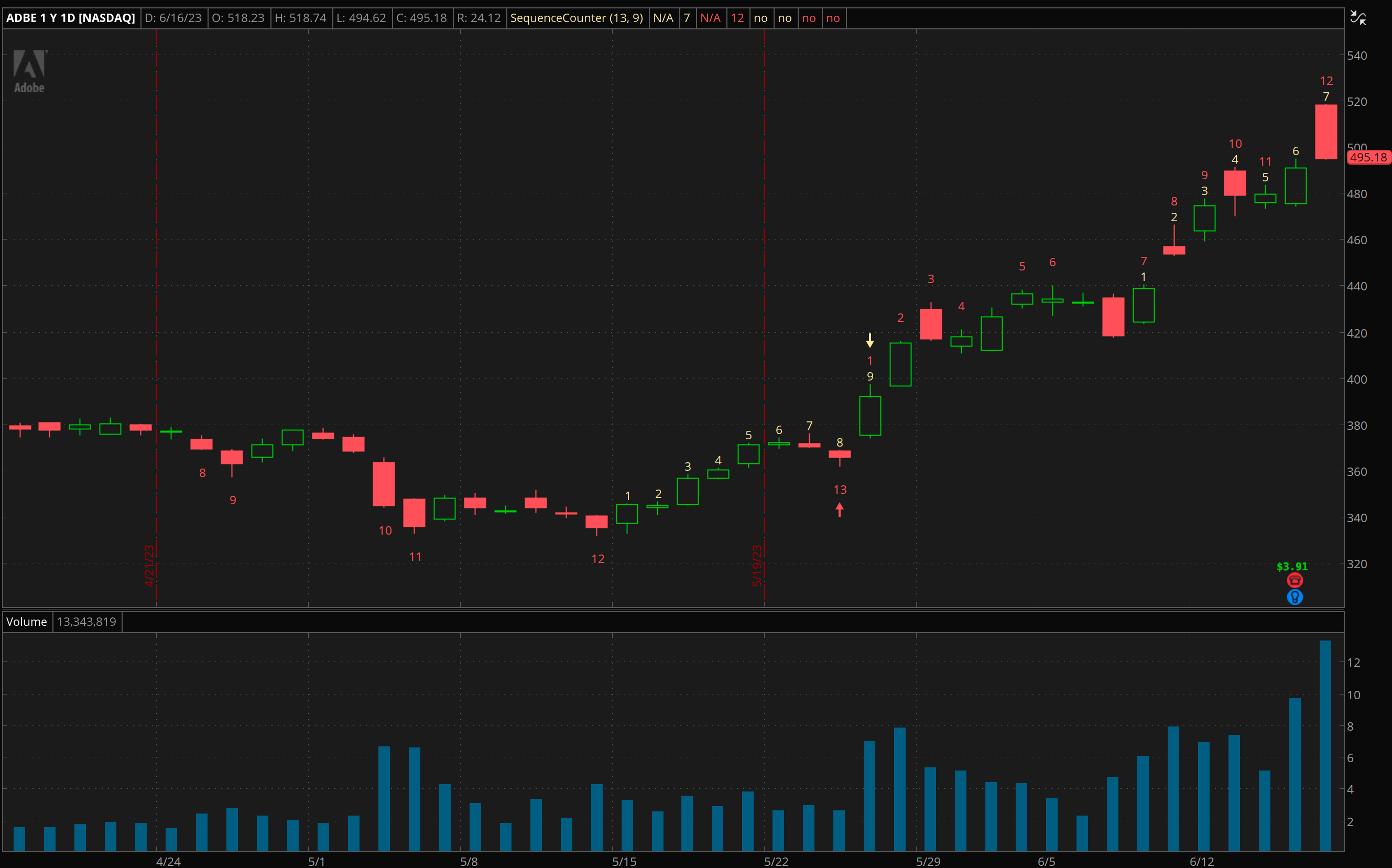

Returning to Adobe, it’s necessary to highlight the ominous candle that formed on Friday. This reversal from an overbought extended situation should signal for those who haven’t taken profits in ADBE 0.00%↑ already that now may be the right time to lock in those gains before some retrenchment; though it should be pointed out, a significant amount of implied volatility rolled off during Friday’s selloff alleviating some worry..

On the more speculative side of things, over in the Discord, there is an ongoing discussion regarding tech laggards such as Airbnb and Fiverr. Another name that’s been tossed out with the bath water is DAVA 0.00%↑ . Even though top-line growth is still being reported, this UK-company has a firm footing in the South Pacific where there is a lot of secular optimism, the stock is off over 40% from it’s recent February high. A potential breakout Endava’s primary downward trend should be monitored.

2) Sector Performance

Looking at Friday’s closing auction most risk-on sectors were flat to negative on the day, and the opposite was true for Utilities, Materials and Staples.

However, reflecting on the entire week, the bull market continued with large gains in most segments of the market, with the exception being energy, which finished on a loss.

Though not making the largest move on the week, one sector that certainly made an impact, and highlights just how little traders and investors are currently worried about a deep recession, is the participation of the industrials in this rally. Here is a chart of the equal weight industrial etf which is keeping up step for step with the blue chip heavy S&P500, and also breaking to new highs.

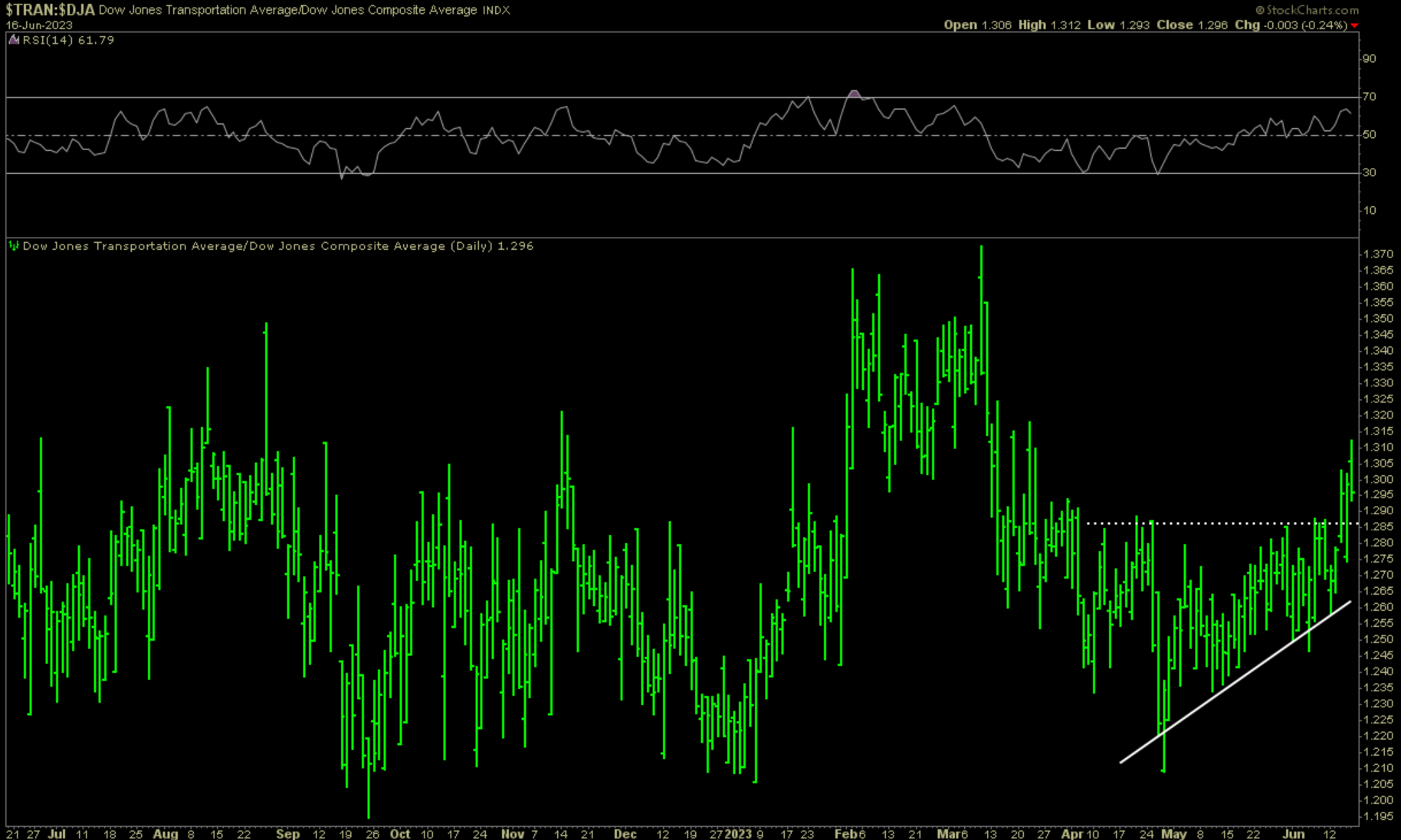

Inside industrials, currently leading the show are transportation sectors. Taking a look at the chart of the Dow Jones Transports vs. the Dow Jones Composite, we see just how strong this relationship is.

…and getting even more granular. Here is the chart of FDX 0.00%↑ which reports earnings this week and is also revisiting a critical level.

Semiconductors

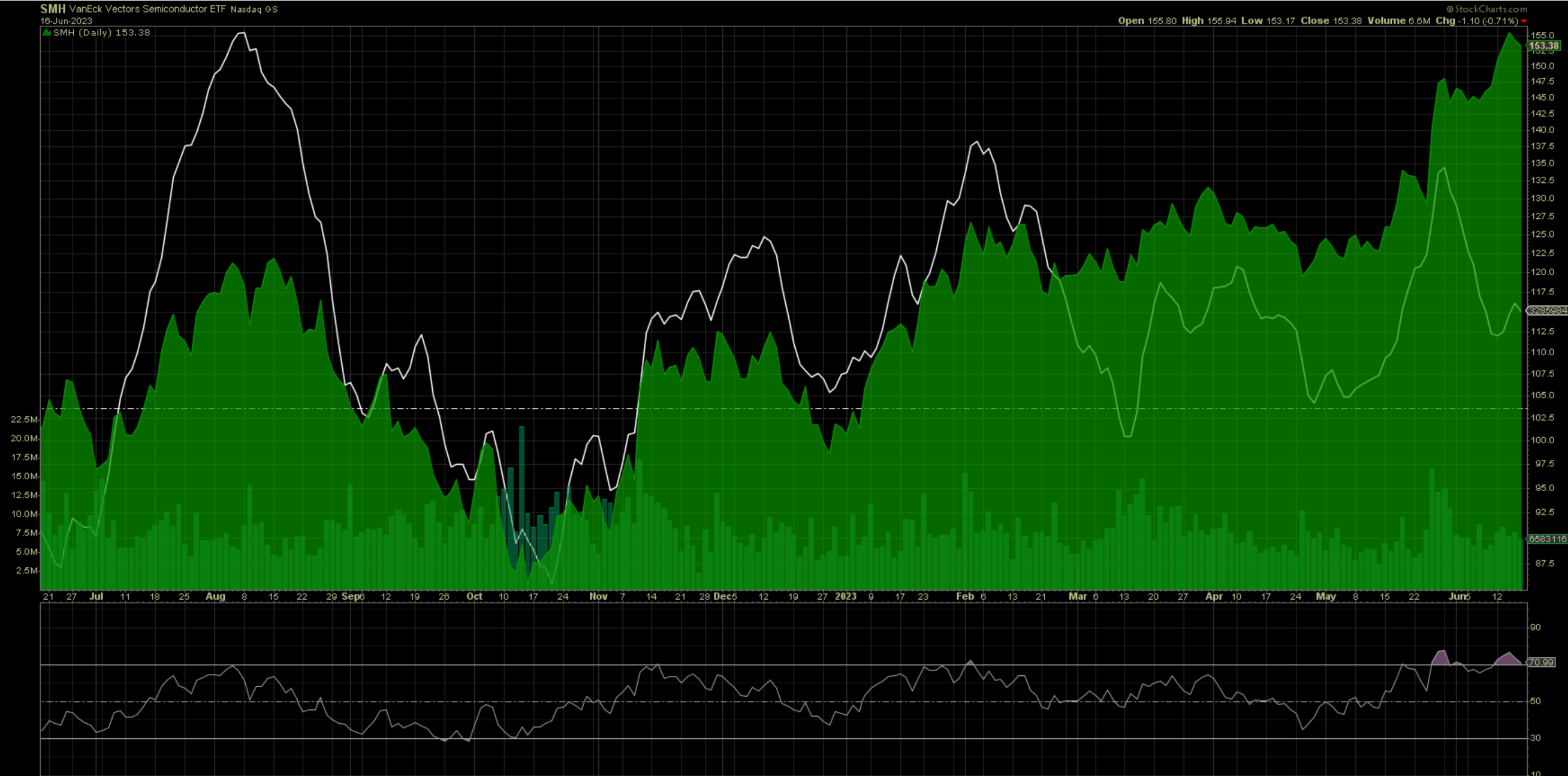

Returning back to semis where “the trend remains your friend.” Here is the chart of the SMH 0.00%↑ including daily oscillator, neither indicating an extreme overbought state or signs of fear.

3) Earnings reports from this last week:

In the absence of significant earnings this week we diverge by looking into what banks are currently up to. Major US banks are first to report at the beginning of each earnings season. These banks are usually a harbinger for how earnings season unfolds further. In April for Q1, these money center banks surprised to the upside. Given better insight into their businesses now after the release of 10k’s, it would be nice to see price performance exceeding that of the S&P broad index in the weeks to comes. Should this cease to materialize, a careful stance should be maintained heading to the next earnings season in mid-July.

4) The week ahead

From Barrons:

The Calendar

It will be a holiday-shortened trading week with a handful of major earnings reports, economic data releases, and two days of Congressional testimony from Federal Reserve chairman Jerome Powell. U.S. stock and bond markets will be closed on Monday in observance of Juneteenth National Independence Day. This newsletter will be off Monday, as well, back in your inbox on Tuesday night.

Once Wall Street returns, FedEx reports on Tuesday, followed by Darden Restaurants, FactSet, and Accenture on Thursday, then CarMax on Friday.

There will be plenty of data out next week on the state of the U.S. housing market. On Monday, the National Association of Home Builders releases its housing market index for June. The Census Bureau publishes residential construction data for May on Tuesday and the National Association of Realtors reports existing-home sales for May on Thursday.

The Conference Board will also release its leading economic index for May on Thursday.

Fed chairman Powell will deliver semiannual testimony before the House Financial Services Committee on Wednesday and before the Senate Banking Committee on Thursday.

The Bank of England will announce a monetary-policy decision on Thursday, with markets pricing in a 13th-straight interest-rate increase.

--Nicholas Jasinski

5) Macro conditions

Weekly risk signals are based on intermediate and long-term market trends, as well as the flow of money into or away from asset classes. Not included are potential fundamental or gamma implied volatility tail risks.

Note: top traders themselves have a hit rate approaching the 50% lower bound. Controlling risk on losing positions and letting winners prosper is for many the difference in creating a successful track record over time.

The summer solstice is quickly upon us and the situation for stocks is nearly perfect-like. As the preferred alternative to FX, bonds or commodities, this is where the momentum is lying.

As the only gauge not complying, I’ll provide a little more color on the tool for the Federal Reserve above. In this regard the metric for the Federal Reserve uses the KISS or keep it simple stupid principle. The Risk-on/-off gauge takes the Fed’s intention, as relayed to markets, as it’s guide. That intention now is to keep a policy significantly restrictive to bring down inflation. Keep in mind that inflation is good for a company with a large moat and pricing power, so destroying demand for these goods and services in not automatically considered a positive.

With that said, there is some importance to keeping an eye on the current balance sheet (unchanged recently) and the neutral rate, as well as the Fed’s own tools of financial indexing and manufacturing data. It is however believed by yours truly that none of these free FRED models give any significant ability to predict market directions, or will give a flashing red signal prior to an exogenous event. Therefore our gauge uses more intuiting than being “data dependent.”

6) Opportunities Internationally

The UK (a mini-introduction)

We’ll revisit our next island nation in more detail again at a later date, but given the ongoing success of Japan, it’s worth continuing to scout for certificates selling at a discount. What makes the UK interesting in my opinion are public markets with a bit more exposure to growth when compared to the continent. This may gain more attention as Arm nears it’s upcoming ipo, which could be spectacular.

A similar company that looks interesting is Alphawave IP Group, a semiconductor services company. Here is the chart:

Other growth opportunities include Abcam ABCM 0.00%↑ which recently migrated it’s listing to the US, and Fevertree Drinks (charts below).

😎 Cheers! 😎

Disclaimer: Please note that the information provided in this article is for general informational purposes only and does not constitute financial, legal, or professional advice. The information provided should not be relied upon as a substitute for financial, legal, or professional advice. Before making any decision, it is important to consider all relevant information and consult with a professional who can provide personalized advice based on your specific circumstances. The author and publisher of this article cannot be held liable for any actions taken based on the information provided. This is not a recommendation to buy or sell any specific securities or financial instruments.