Back with a New Blast

Back with a New Blast

Market Insights - Sunday Aug. 20

*after a longer hiatus than expected. QF is proud to mark the resumption of …

🕵 The Seeker 🕵

1) Big moves drawing attention from the last three trading days

Looking across the NYSE and Nasdaq, of stocks with improving fundamentals, there are only 3x names making a mark. Those companies are ANF 0.00%↑ , ROST 0.00%↑ , and PDCO 0.00%↑ . Last week Ross reported good results. Wall Street is expecting similar from Abercrombie & Finch. As you can see, looking at the weekly chart below, this stock has been on a tear. ANF 0.00%↑ reports earnings before the bell on Wednesday. Weekly options are currently pricing in a 7% move.

Another name drawing interest is Groupon, yes that Groupon(!). The historical fundamentals don’t look great. GPN 0.00%↑ isn’t currently profitable. It may also need to raise cash, but the company beat expectations in their previous quarterly update, and their statements point to some signs of good stewardship from management. We notice large interest in owning these shares recently. Here is the daily chart.

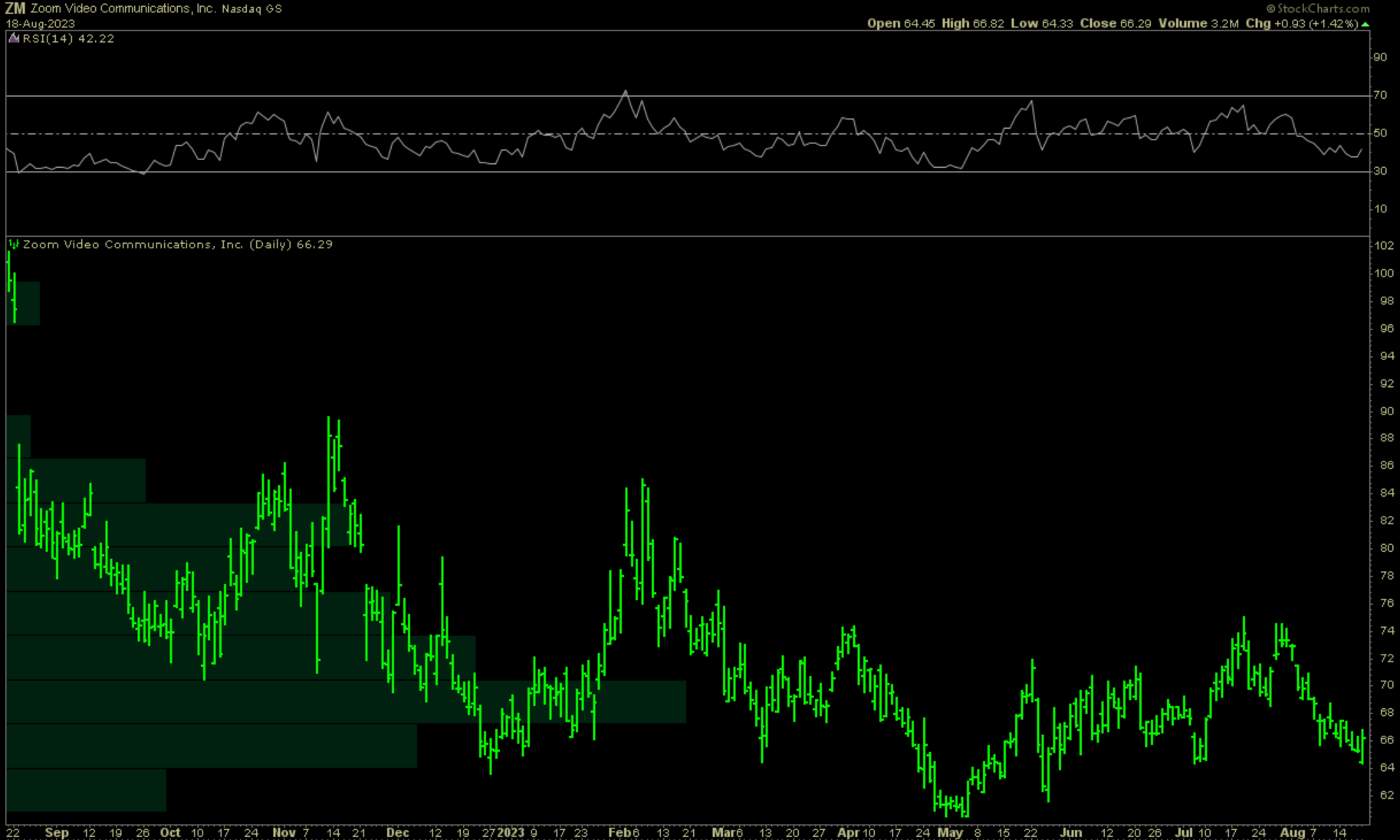

Another name of interest reporting this week is ZM 0.00%↑ , who reports earnings Monday after the close. Expectations are currently low. Revenue growth has leveled off for the company since since a big boost after the pandemic began. Though having a household name, the stock is unloved and investors are waiting for answers from management about how to return to growth, and/or generate more cash from operations. Upcoming investor reaction will be telling.

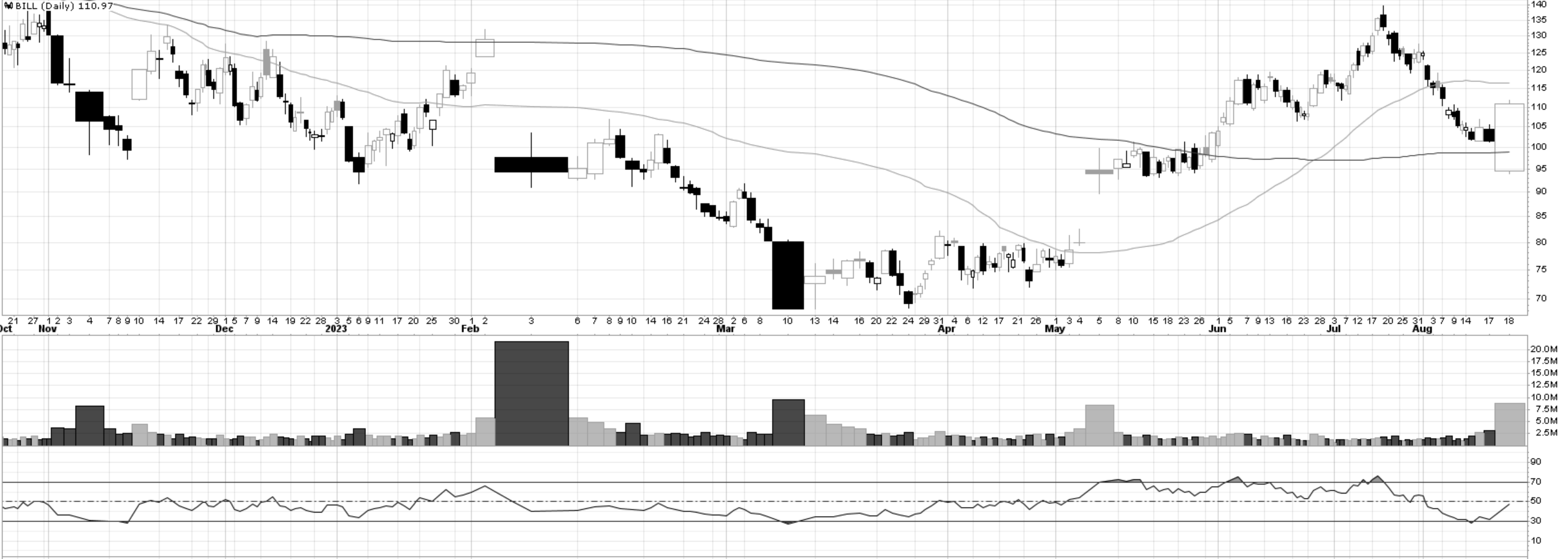

Speaking of ownership, Friday saw a lot of shares changing hands in Bill.com, a service for small businesses. Prior to earnings, the fortunes of BILL 0.00%↑ have followed the decline in small-caps to a tee. Friday however was potentially the type of volume to propel the stock higher over the long-term. With such a large daily move it’s unlikely that the price will continue an immediate explosion. However this relative performance now projects the stock onto the high-quality list for an early correction when conditions improve across the whole market.

2) Sector Performance

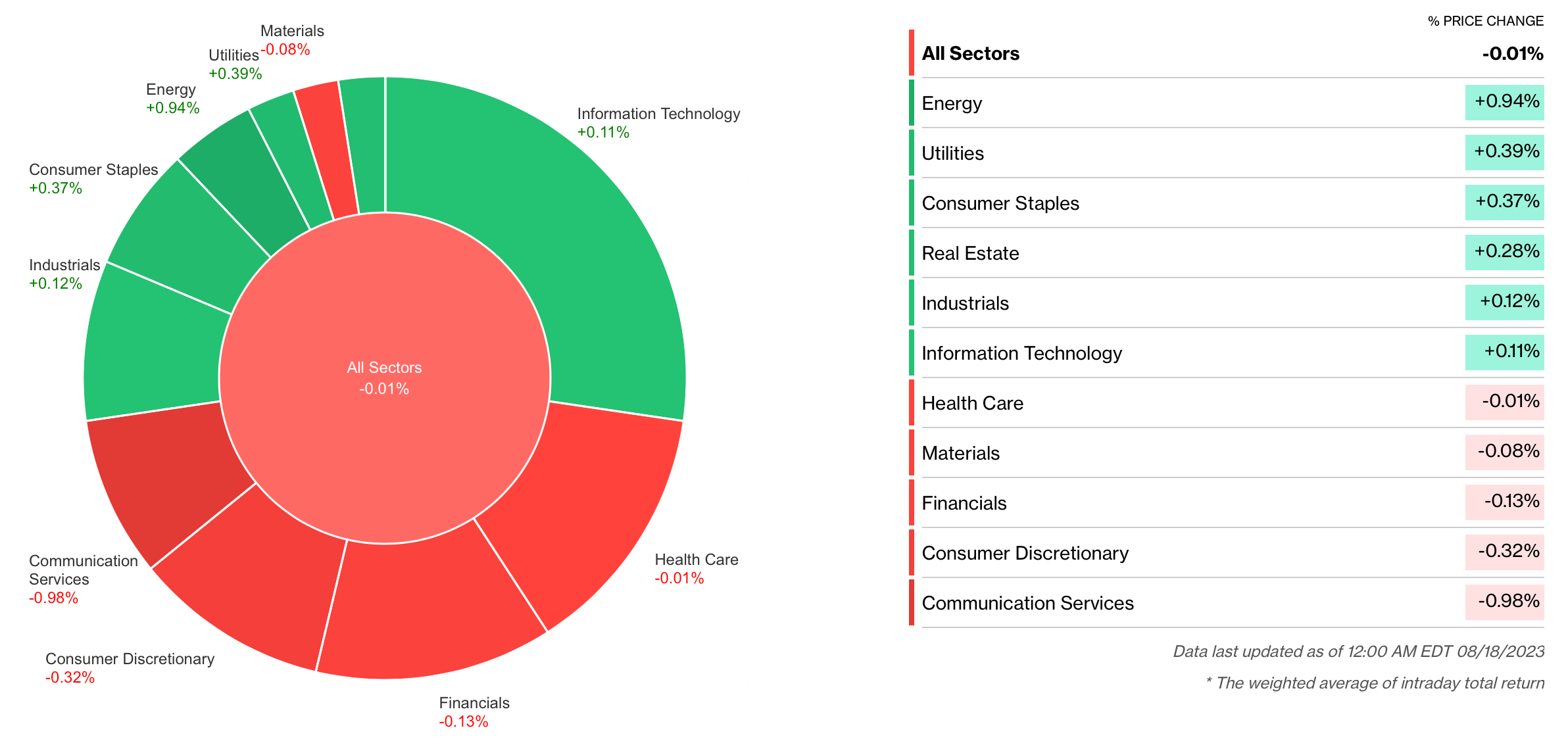

On top of Friday’s scorecard were defensive sectors, only topped by Energy. Interestingly this one day move in oil related stocks, may potentially be signaling the end of the short correction in crude.

Taking the broader weekly health of the markets, there was a strong negative correlation across all sectors. Of additional interest though was the heavy selling we witnessed on Thursday, and now after the results are tallied, the risk-on sectors of Energy and Technology are showing the most signs of improvement.

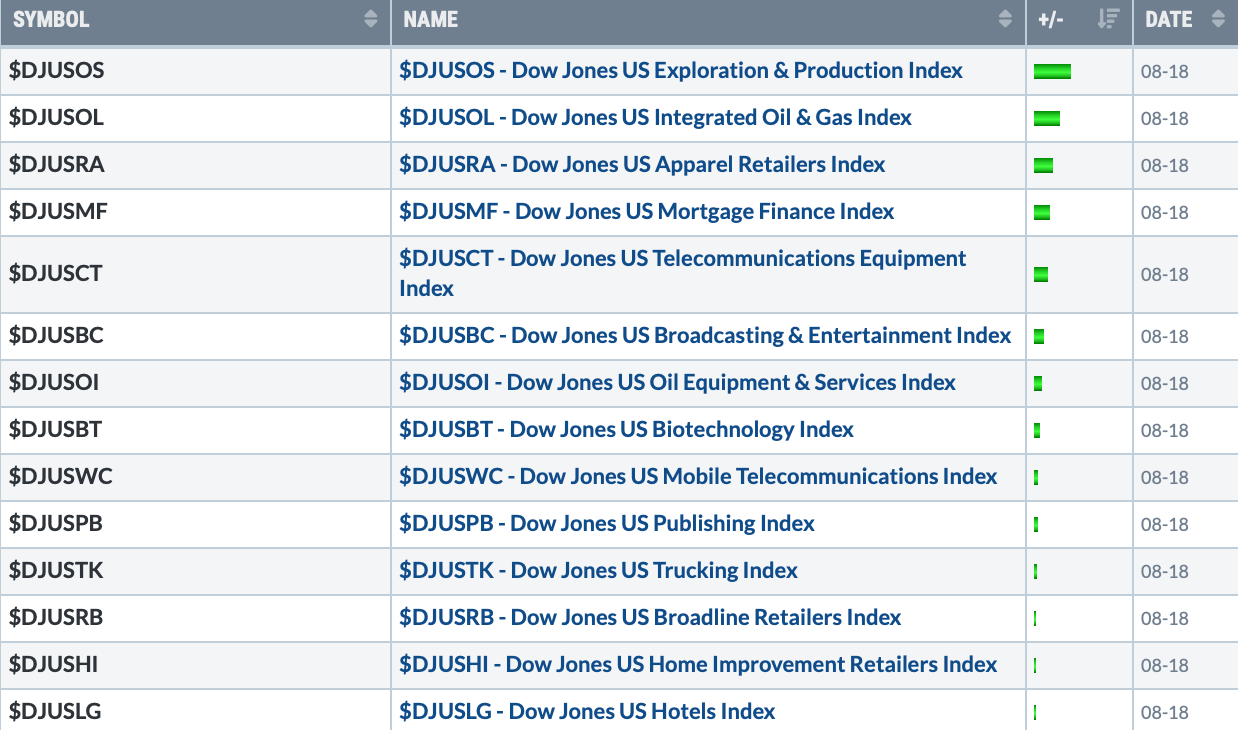

The following industries have regardless held up the best during recent broader market weakness.

As noticed by the table above, semiconductors, our preferred gauge of risk-on sentiment, hasn’t floated anywhere near the leadership top, and relative to the S&P500, semis are currently making a low.

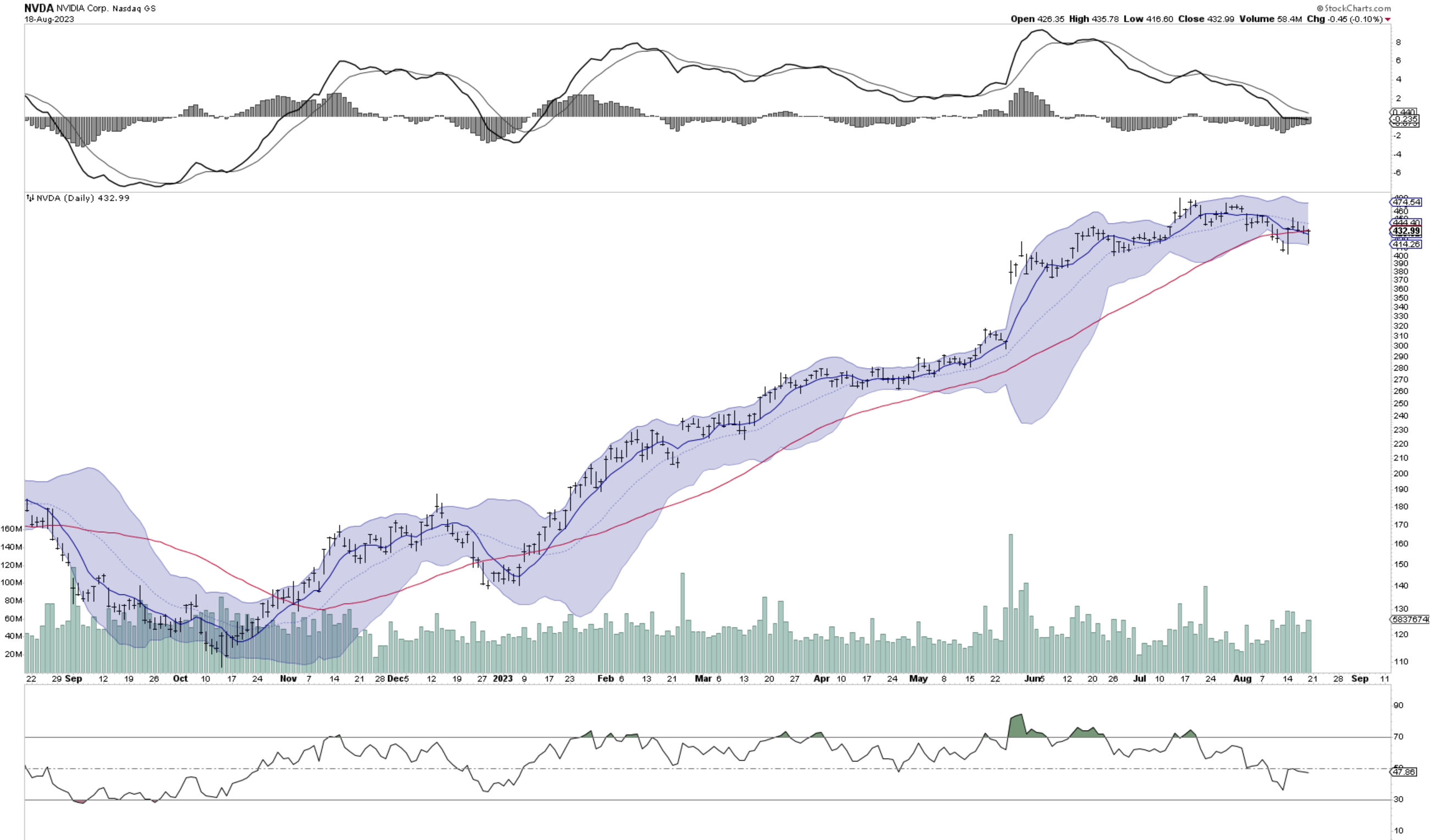

Of course some names have been performing better like LRCX 0.00%↑ and KLAC 0.00%↑ , but most eyes will be on Nvidia’s results this week. Currently the sentiment in NVDA 0.00%↑ is being reset. Looking at it’s chart, it’s RSI recently dipped below 50, came up and then rejected this mark. Throughout it’s remarkable run-up this year, this was the first and only time this has happened, and could signal that earnings might be more of a liquidation than accumulation event.

3) Earnings reports from the prior week:

Weekly results from some names of significant interest.

4) The week ahead

From Barrons:

The Calendar

The majority of second-quarter earnings season is over, but there are a handful of major technology and retail names left to report next week. Economists will be focused on any news from an annual gathering of monetary policy thinkers and practitioners in Jackson Hole, Wyoming.

Zoom Video will report on Monday then Lowe's on Tuesday, followed by a busy Wednesday: Nvidia, Snowflake, Advance Auto Parts, Bath & Body Works, and AnalogDevices are all on the schedule. On Thursday, Dollar Tree, Intuit, Nordstrom, and Ulta Beauty will be the highlights.

The Federal Reserve Bank of Kansas Citywill host its 2023 Economic Policy Symposium from Thursday through Saturday. This year's topic will be "Structural Shifts in the Global Economy." Fed chair Jerome Powell is scheduled to address the conference on Friday.

Economic data out next week includes Markit's manufacturing and services purchasing managers’ indexes for August on Wednesday. Both are expected to tick down from their July levels.

Other releases will include the National Association of Realtors' existing-home salesfor July on Tuesday, new-home sales data for July on Wednesday, the Census Bureau'sdurable goods report for July on Thursday, and the University of Michigan's consumer sentiment index for August on Friday.

5) Wisdom of Crowds

6) Macro conditions

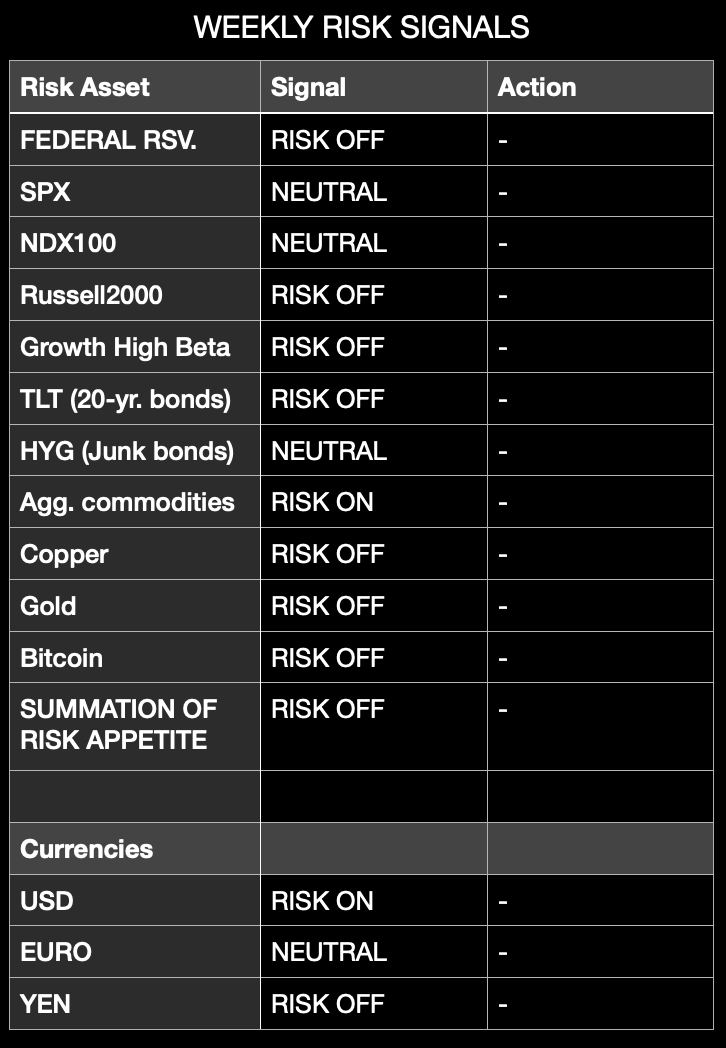

Weekly risk signals are based on intermediate and long-term market trends, as well as the flow of money into or away from asset classes. Not included are potential fundamental or gamma implied volatility tail risks.

Note: top traders themselves have a hit rate approaching the 50% lower bound. Controlling risk on losing positions and letting winners prosper is for many the difference in creating a successful track record over time.

While the bugs are still being worked out of the new Growth High Beta Index of stocks, we’re reporting the results of Cathie Wood’s ARK Innovation Fund for one final week. Together with the Russell2000, general sentiment is trending towards Risk-off.

However, we’d be remiss not to mention where the real weakness lies, and that is in the credit markets with TLT 0.00%↑ venturing towards retesting the lows of this cycle. What’s bringing this about is excess bond supply, as shown by the bidding up of 10-yr. treasury rates, closing this week at the highest levels since 2007 and currently making a firm handle formation.

6) Opportunities/Movements Internationally

India

Over the last 18 months, iShares’ etf that tracks Indian large cap dividend paying corporations is displaying significant outperformance vs. it E.M. peers - see chart below plotting the weekly moving averages of INDA 0.00%↑ and EEM 0.00%↑ .

Given the current strength of the dollar, this may make a great opportunity for averaging into this fund or it’s counterpart INDY 0.00%↑ , these baskets of stocks with major secular tailwinds at fair prices.

(Note: for our readers that may manage money. We’d look forward to your input regarding the composition of these funds in the comments, or over in our Discord)

For deep value disciples, you might want to mirror the portfolio of legendary investor Mohnish Pabrai. Here are the long-term holdings of his fund as given by website Trendlyne.

😎 Cheers! 😎

Disclaimer: Please note that the information provided in this article is for general informational purposes only and does not constitute financial, legal, or professional advice. The information provided should not be relied upon as a substitute for financial, legal, or professional advice. Before making any decision, it is important to consider all relevant information and consult with a professional who can provide personalized advice based on your specific circumstances. The author and publisher of this article cannot be held liable for any actions taken based on the information provided. This is not a recommendation to buy or sell any specific securities or financial instruments.