Back with a New Batch

Back with a New Batch

Market Insights - Sunday Aug. 27th

Hello and welcome to another issue of 🕵 The Seeker 🕵

I never lose. Either I win or learn. - Nelson Mandela

1) Big moves drawing attention from the last three trading days

With much of the seasonal equity selling now front-loaded to August, the theme this week is mean reversion to the primary trend which has been upward for the greater part of 2023.

One stock that the sell side has been raving about recently is ENVX 0.00%↑. There could be incentive here for higher prices ahead of new investment banking business down the road. Strict risk control is a must, but the path could be higher if last month’s correction is over.

Another stock we’re watching at the bottom-end of it’s range is AEHR 0.00%↑, a strong outperformer in 2022 with follow-through moving in large gaps this year.

One stock with strong fundamentals and trading back to former resistance (i.e. support) is NPK 0.00%↑. If the RSI is unable to make a bounce off 40-50, exactly where it sits now, then we’ll take our loss, as this level usually signifies support in a bull market.

NERV 0.00%↑ has most likely issued a ton of stock at lower and lower evaluations since the all-time high, but at the current moment, this set-up has potential. There are known investors invested, and with services like eToro, that might be what’s causing the base. However, Steve Cohen could be out long before an updated 13F. (Tread with caution)

Sometimes investing can be as simple as the Peter Lynch makes it out to be; re: NVO 0.00%↑ . Here is Mattel, surrounded in hype from the success of the Barbie franchise. MTL 0.00%↑ is holding a nice support level. If it goes higher from here it becomes an even stronger buy 🤯

…and a bonus chart for the week. In another mind-blower, the beta of Alibaba as according to Yahoo Finance is 0.68(!). Even though others are also making this call, and that’s not always a bullish sign. I agree and think BABA 0.00%↑ looks set-up to move higher.

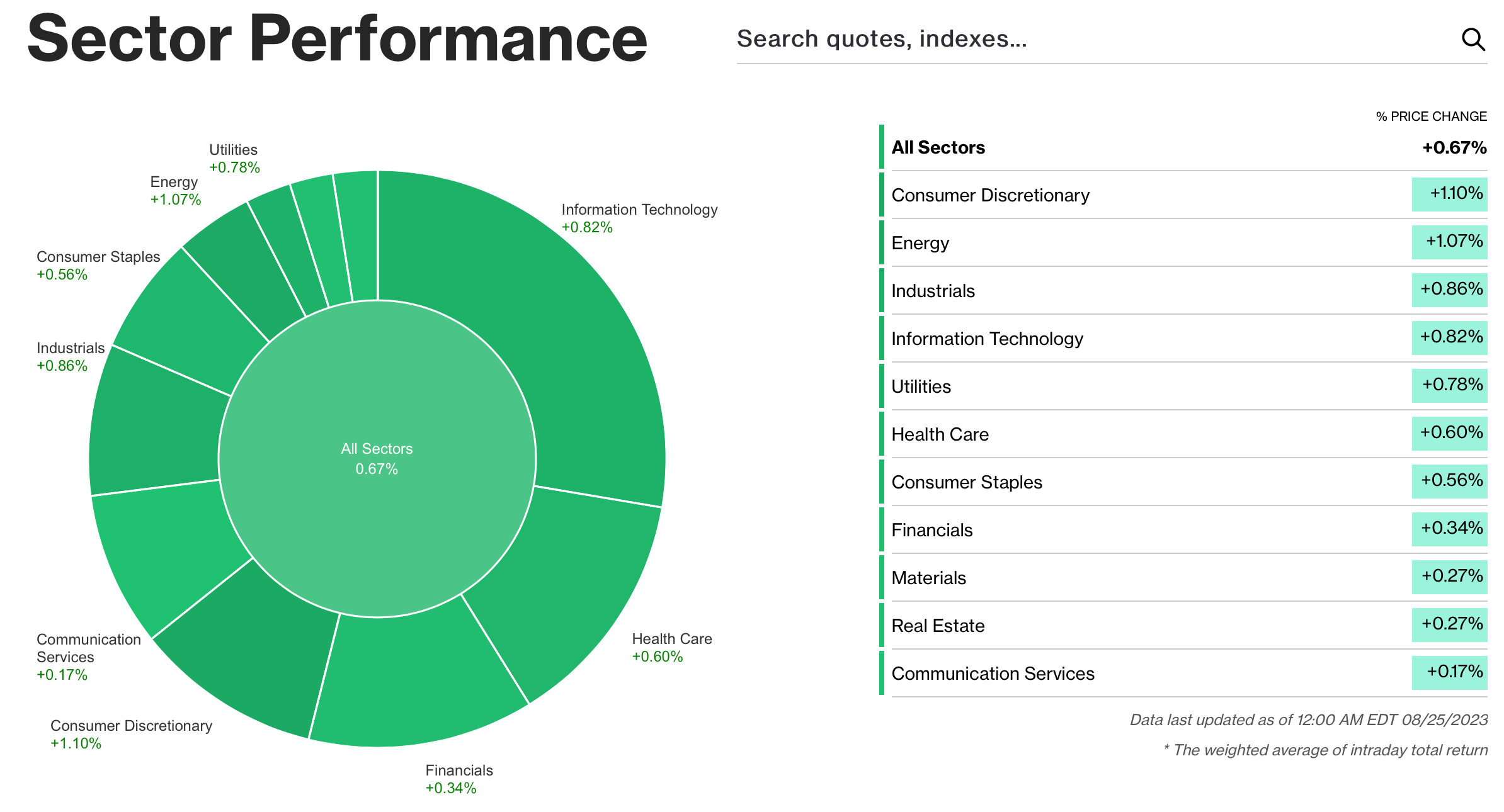

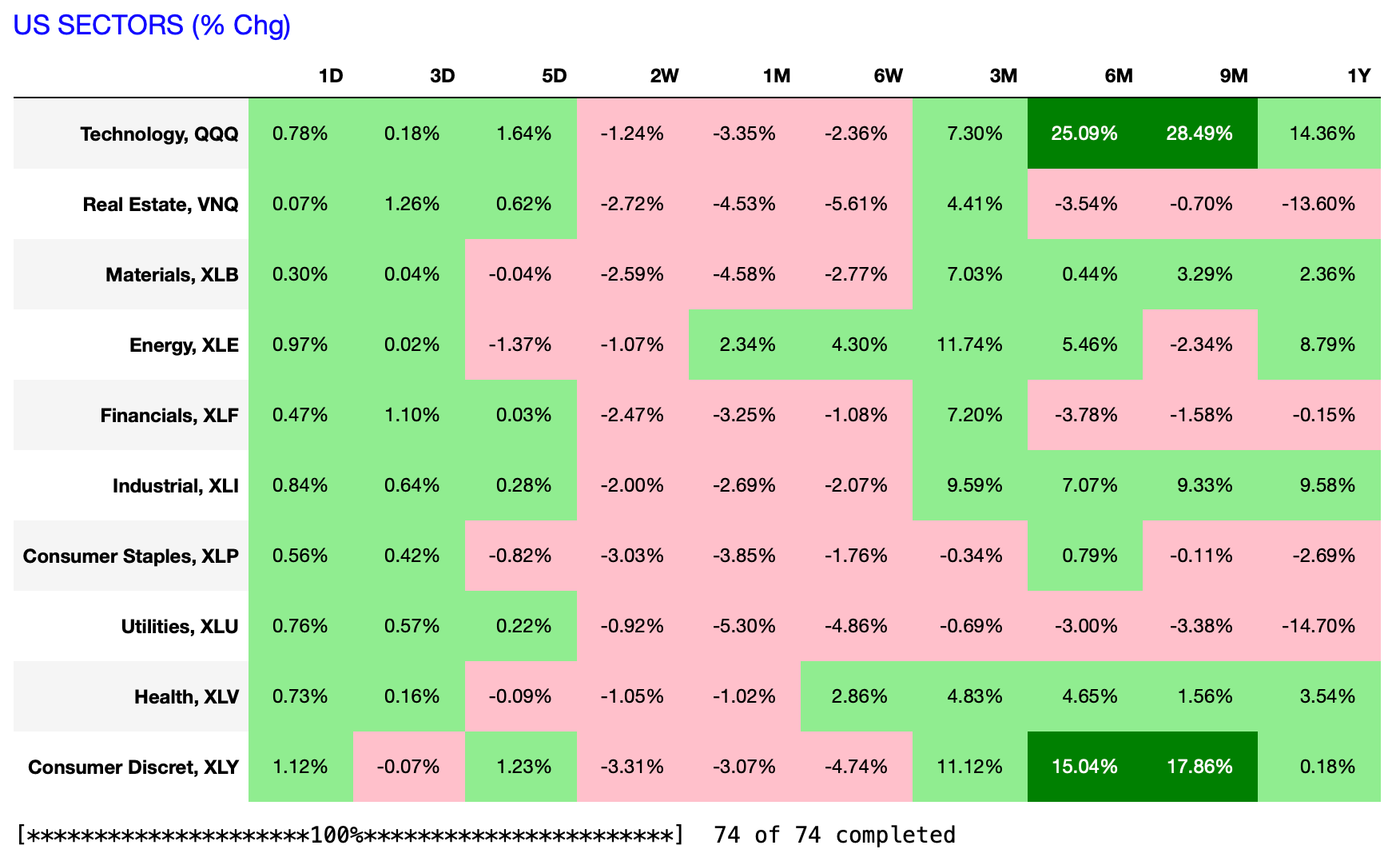

2) Sector Performance

Friday produced green shoots across board with the Dow Jones and Nikkei, etc. ending higher. Here is the sector breakdown:

Furthermore, we saw risk-on sectors such as Consumer Discretionary and Tech moving higher on the week, much of the gains coming after Powell spoke on Friday.

The heaviest action was in Semiconductors following Nvidia earnings. Currently, the oscillator reading the SMH 0.00%↑ sector etf are extended in the lower quadrant and possibly starting a trend of lower lows/highs.

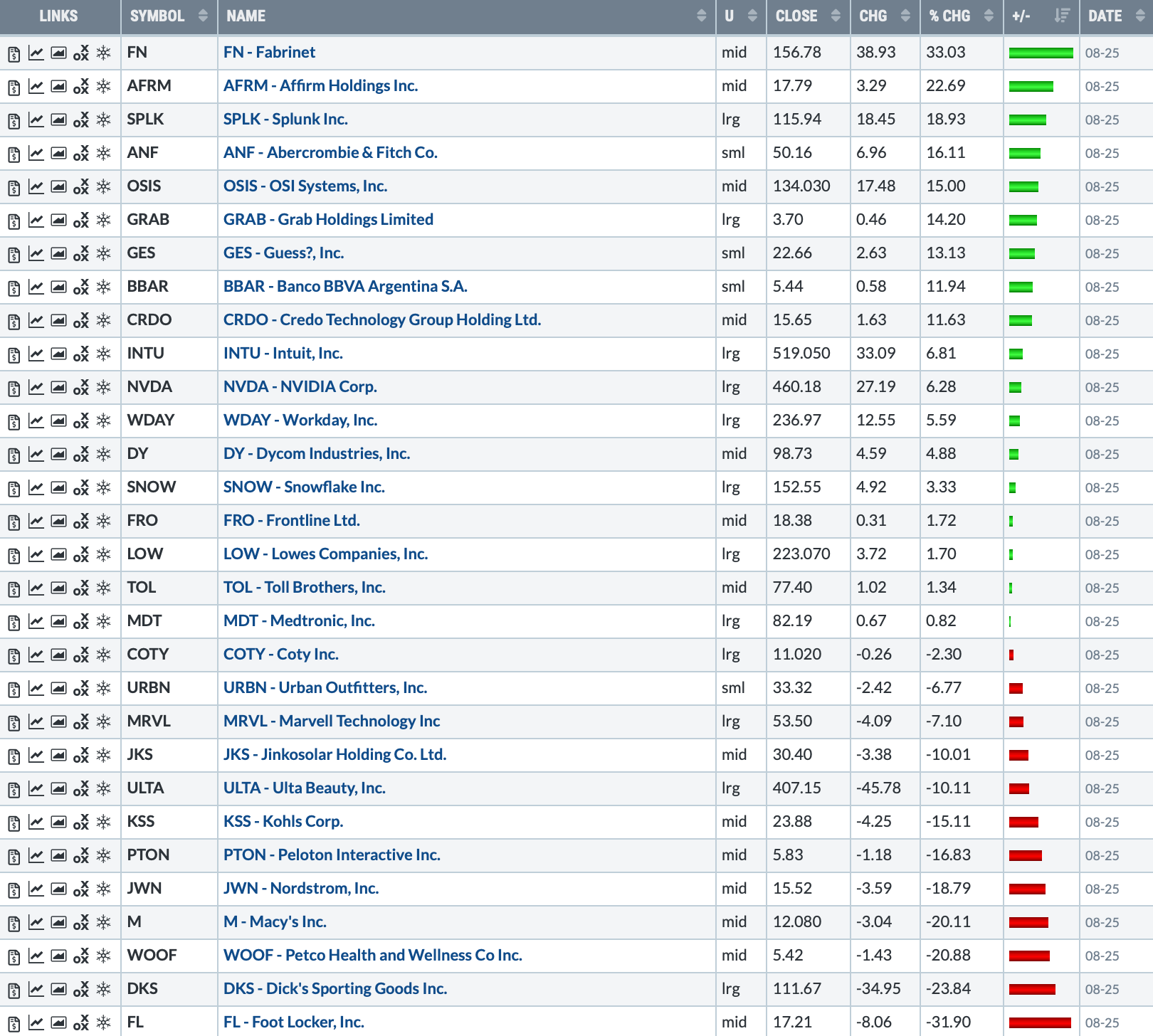

3) Earnings reports from the prior week:

Weekly results from some names of significant interest.

4) The week ahead

From Barrons:

The Calendar

New data on the U.S. labor market will be next week's highlights, as well as earnings reports from several retailers and the latest inflation data.

Best Buy, Hewlett Packard Enterprise, and HP will report on Tuesday, followed by Salesforce and Brown-Forman on Wednesday. On Thursday, Broadcom, Dollar General, and Campbell Soup release results.

The Bureau of Labor Statistics will publish the results of the July Job Openings and Labor Turnover Survey on Tuesday. Economists are forecasting job openings to hold about flat from a month earlier.

On Friday, the BLS is expected to report a gain of 175,000 nonfarm payrolls for August, which would be another slim deceleration from the prior month. The unemployment rate is forecast to hold steady at 3.5%. Average hourly earnings are seen rising 0.4% month over month, matching July's pace.

Other economic data out next week will include the Conference Board's Consumer Confidence Survey for August on Tuesday and the Bureau of Economic Analysis'personal income and expenditures data for July on Thursday.

Economists are expecting to see a 0.3% rise in income and a 0.7% increase in spending in the month. The Federal Reserve’s preferred inflation measure, the core personal-consumption expenditures price index, is forecast to be up 4.2% from a year earlier.

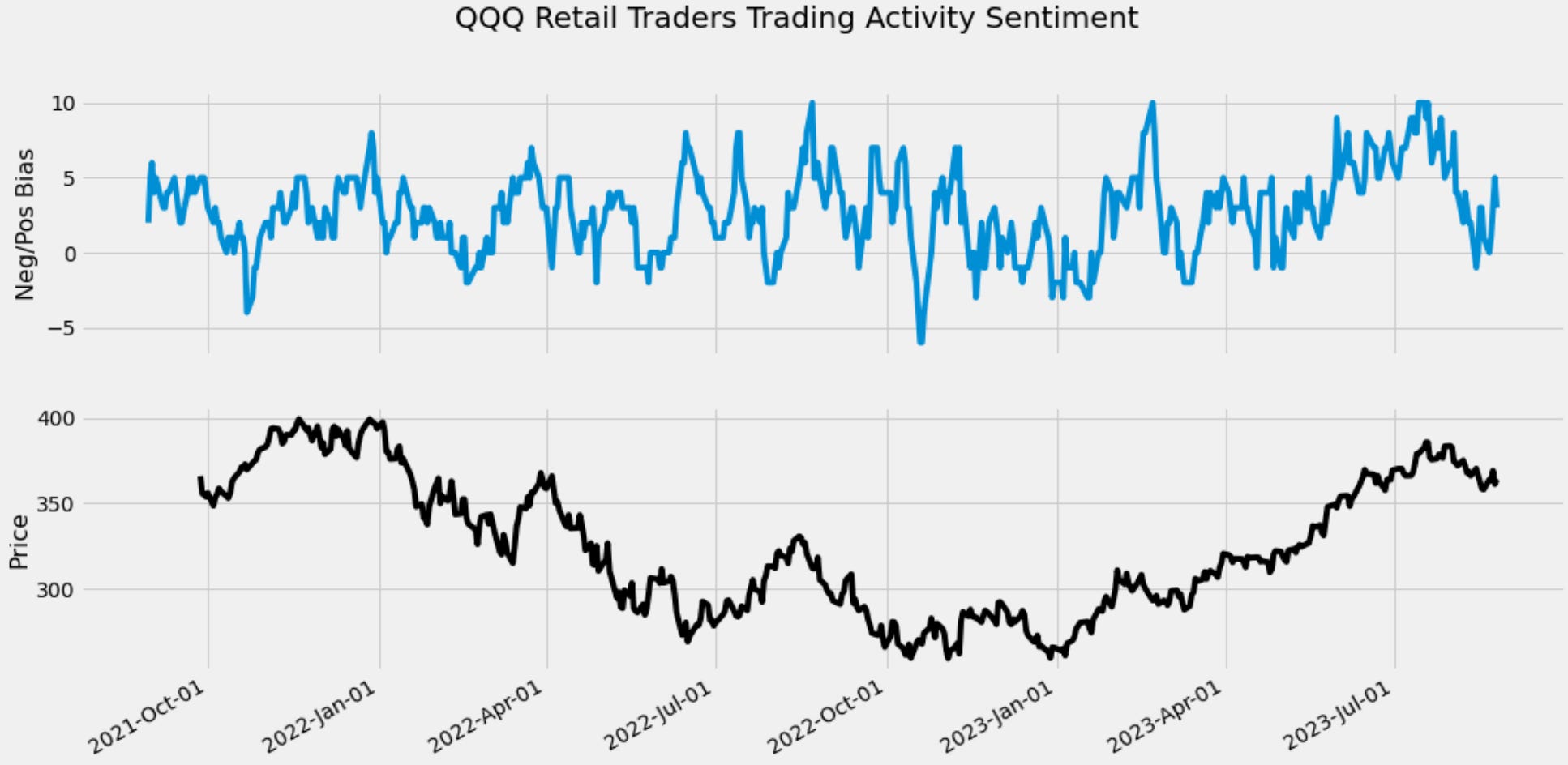

5) Wisdom of Crowds

6) Macro conditions

Weekly risk signals are based on intermediate and long-term market trends, as well as the flow of money into or away from asset classes. Not included are potential fundamental or gamma implied volatility tail risks.

Note: top traders themselves have a hit rate approaching the 50% lower bound. Controlling risk on losing positions and letting winners prosper is for many the difference in creating a successful track record over time.

Still in the spotlight this week will be bonds. According to Saxo Bank, the 20-year US Treasury bond is a special issue, and that may have cause the recent spike in August of the MOVE index (the volatility gauge of bonds) and therefore yield spreads and the $USD.

With this news event out of the way, this might make way for a cool-off rally without the pressure from the dollar and the inverse lift to stocks. Notice the hot indicators readings and over extendedness of UUP 0.00%↑ having nearly filling the entire gap from November.

Currently investors are leaning more positive following last weeks foundation being formed.

6) Opportunities/Movements Internationally

With high valuations in the US and a dollar off it’s rockers, we think there are multiple areas to proffer.

This week Morgan Stanley gave an insightful analysis for Cnbc viewers of what’s happening around the Peloponnese peninsula. Link provided here: https://www.cnbc.com/video/2023/08/15/morgan-stanley-says-greece-is-its-top-holding-in-its-em-fund.html

In addition, the interest rate situation may bring about a great opportunity to invest in the United Kingdom currently snoozing like an (under)value trap.

One admirable corporation there is Halma.

😎 Cheers! 😎

Disclaimer: Please note that the information provided in this article is for general informational purposes only and does not constitute financial, legal, or professional advice. The information provided should not be relied upon as a substitute for financial, legal, or professional advice. Before making any decision, it is important to consider all relevant information and consult with a professional who can provide personalized advice based on your specific circumstances. The author and publisher of this article cannot be held liable for any actions taken based on the information provided. This is not a recommendation to buy or sell any specific securities or financial instruments.